My colleague, a formidable stock picker with an impressive market beating record of performance over the past five years and more, (providing average annual returns on his substantial portfolio of SA shares of 20.7% p.a. since 2020) asked an intriguing question about AVI. A listed company that is a mixture of branded food and consumer goods manufacturer, deep sea fisher and fashion retailer. AVI has realised an exceptionally impressive return on the capital it employs. Its internal rate of return (IRR) was as high as 30% in 2024. It has averaged over 25% p.a. since 2015.

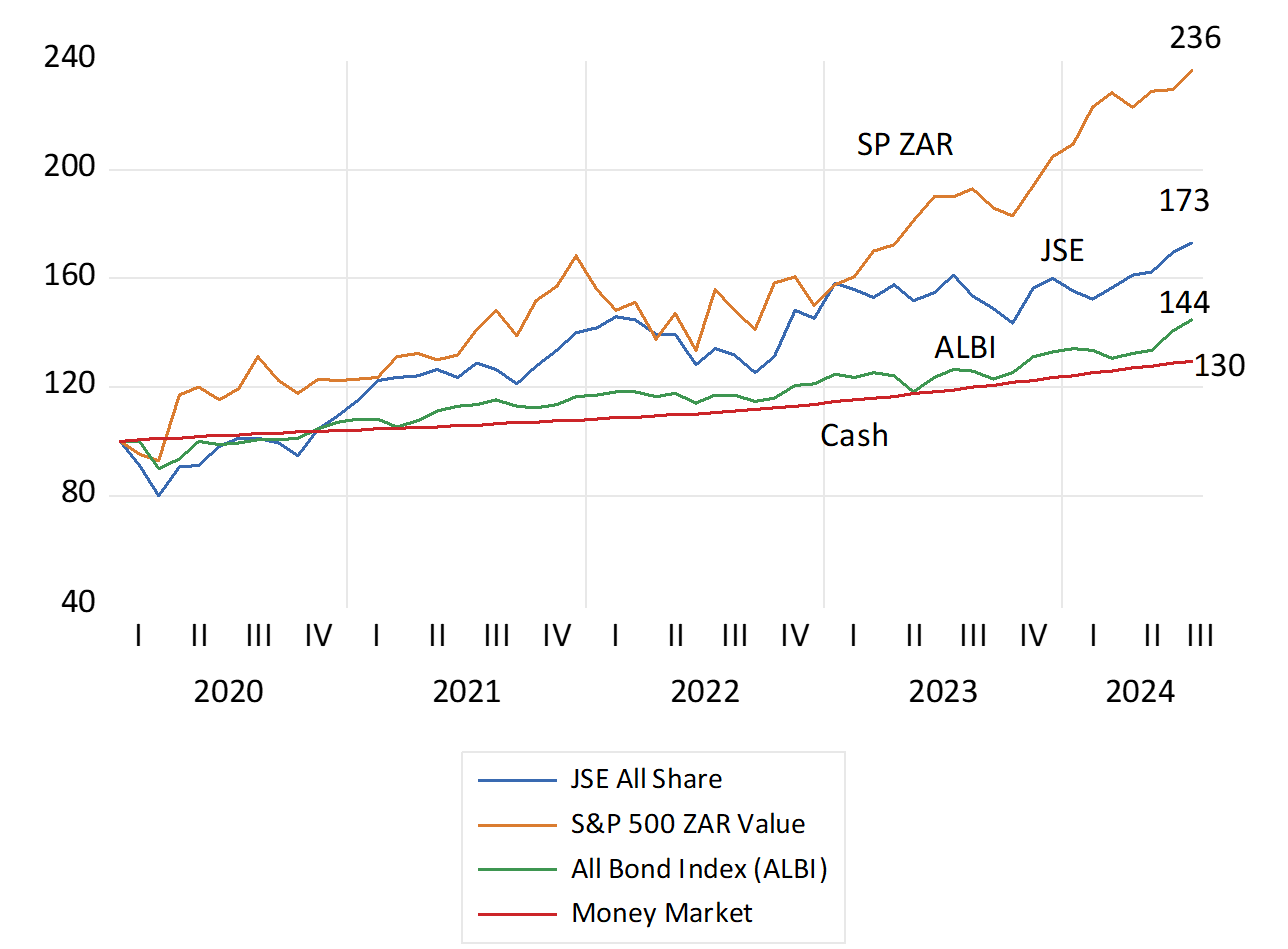

Yet after 2020 the total return to AVI shareholder, dividend yield plus capital gains, has averaged but 9.8% p.a. of which dividend payments, provided an average 7.54% p.a. The share price therefore advanced by only an average 2.2% p.a. over the five years not keeping up the JSE All Share Index that delivered an average 11.2% p.a. return over the same period. Why then, it was asked has AVI performed so poorly for its shareholders despite its very high returns on capital?

The market value of AVI is currently about R31b (it peaked at over R35b in 2018) and is now 14 times its reported earnings. About the same P/E rating as the JSE All Share Index. Between interim, final and a special dividend AVI paid out R8.70 of dividends in 2024 – equivalent to a 8.7% dividend yield in 2024. An initial yield – well above the current JSE average of 3.8%. Clearly while generous payouts may matter for shareholders – they may not do much for the share price.

The contrast with retailer Shoprite (SHP) is striking. Since 2020 the SHP internal return on capital has been much lower, less than 12% p.a. Yet SHP is valued at over 23 times its reported earnings. SHP has invested heavily in growing its business and provided much better returns for shareholders. An average 20.6% p.a. total return since 2020 with average share price appreciation of 17.3% over the five years.

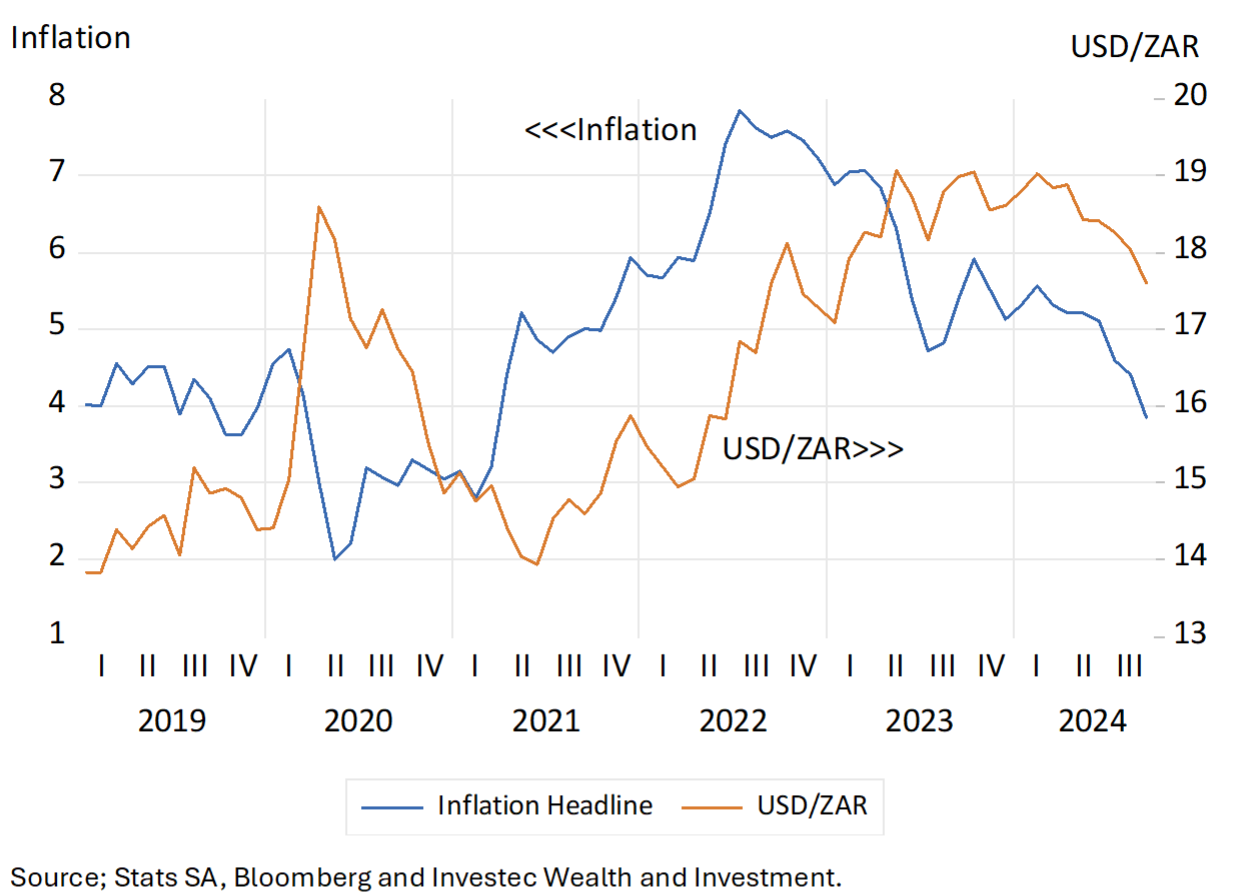

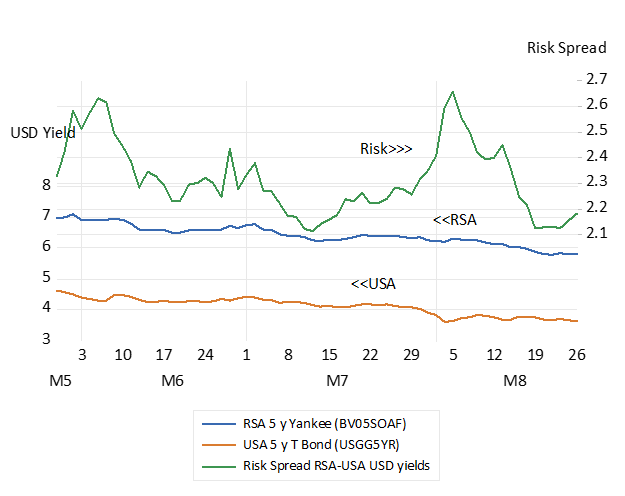

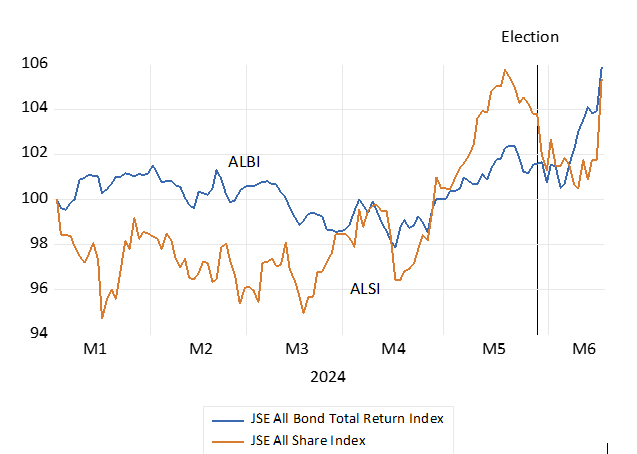

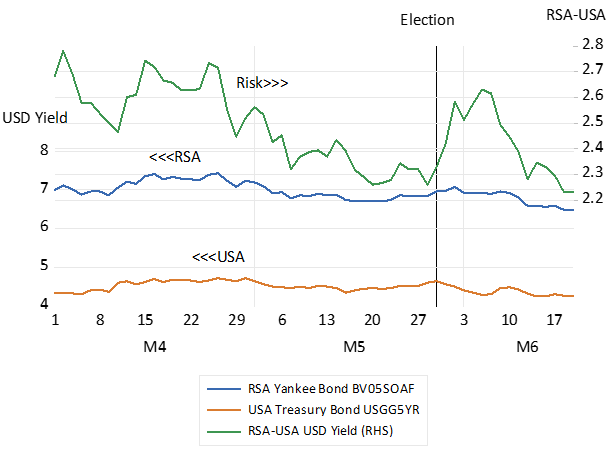

AVI by contrast has added very little capex in recent years. SHP invested about half of its cash flow from operations in 2023 and 2024, over R14,4b in total. AVI invested R959m in the two years. Equivalent to only a fifth of its operating cash flow and equal to a mere 1.4% of its market value. SHP invested the equivalent of 5% of its R155b. market value in 2024. Clearly SHP is valued for the growth in revenues and profits expected to follow its capex. The AVI offer is one of mainly dividends that are not expected to grow rapidly. The high initial dividend yield is therefore much more of an annuity. To be compared with the yield on a long-dated RSA bond, that offers a certain 10% p.a. (see charts below)

We however observe that senior managers in AVI, are granted shares, as a bonus, that vest and can be sold after three years, provided, among other requirements, that the average return on capital employed over the vesting period is ahead of the weighted average cost of capital (WACC) Estimated to be about 11% p.a. Rewarding managers to simply maintain the profit margin, the difference between the return on capital r and the cost of capital c (30-11 for AVI in 2024 ) does not make sense for shareholders. Shareholders benefit from additional flows of economic profits and not only from profit margins. Economic profits are Capex multiplied by the profit margin, which are likely to decline as less profitable, but still cost of capital beating projects are taken on that would raise profits.

These incentives must encourage caution by managers, that is for them to wish to protect profit margin in their own interest, rather than grow profits with additional capex. AVI shareholders should understand these implications and are advised to seek a remuneration policy that is much better designed to align their interests of with those of and managers in market value adding growth.