The financial markets have been roiled by the prospect of recession in the US. The market makers fear that the Fed, having allowed prices to explode in the US will now reverse course abruptly enough to bust the economy. They are right to worry.

Managing the level of demand in an economy well enough to exercise the full potential of an economy – and to avoid continuous increases in the price level, inflation, or its opposite deflation, is a central bank ideal. The more stable the environment, the more accurate become the plans of business, the more predictable their earnings and their values- and vice -versa.

The reality is often very different. The proclivity of central banks to exaggerate the swings of the business cycle is a constant danger to businesses and investors. In some senses the fear of recession may be more disturbing than recession itself. Were a recession to seriously threaten the US economy any time soon, policy determined interest rates in the US would not rise as much and soon go into sharp reverse and equity and bond valuations would rerate on improving prospects. Sell the rumour (of recession) – buy the facts (a recession itself) might well be an appropriate strategy for turbulent times.

The intention of central bank policy interventions should be to smooth the business cycle, avoiding booms and busts – while containing inflation. Central banks can hope to do this by anticipating and then influencing aggregate spending- over which they claim influence. And to ignore temporary supply side shocks (exchange rate or food or energy price shocks for example) that may also cause prices to rise and fall.

Policy settings should not add higher interest rates to the downward, recessionary pressures on demand when prices have risen temporarily. Or vice versa when the supply side of the economy (lower prices) are stimulating demand to lower the cost of credit to push spending still higher. Navigating successfully between supply side shocks- with a temporary impact on the price level – to be ignored – and actions that could cause continuous rises in prices, permanently excess spending- to be actively countered is the true art of central banking. Highly relevant also for the SA Reserve Bank that wrongly believes temporary price increases lead to permanently higher inflation.

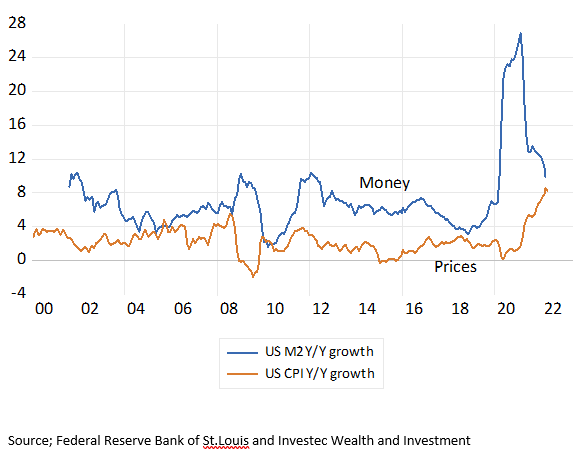

The impact of an extraordinary surge in demand to counter Covid on prices, led by an even more extraordinary increase in the money supply, should not have been anything like the surprise it was inside and outside the FED. The growth in the money supply (M2) peaked at an mind blowing 27% in early 2020. Any sense of monetary history would have regarded much more inflation as inevitable.

The Fed and market watchers had been lulled into ignoring the growth in the money supply and bank lending by years of modest and declining growth in the money supply since 2010 – with declining rates of inflation. Though this record is not without serious blemishes. The run up in money and bank credit growth prior to the GFC should surely have been avoided- as should the abrupt decline in money growth that exaggerated the post GFC recession.

US Money Supply (M2) growth and inflation 2000-2022

Source; Federal Reserve Bank of St.Louis and Investec Wealth and Investment

The Fed should be paying the closest possible attention to the current trends in money supply and bank credit growth and set its interest rates accordingly. It should be aiming to stabilize money supply growth at about 6% a year- consistent with average inflation of 2% a year as was the case to 2019. And to reach that goal – from the current 10 to 6 per cent p.a. growth – as gradually as possible. It should communicate clearly that both money supply and prices are heading in that direction. And that higher prices have already restrained the demand for goods and services.

The marketplace should be paying the same close attention to the growth in the money supply and in bank lending as a leading indicator of the state of the economy. Readings sharply below 6% p.a. growth in the money supply will give ample warning of trouble to come.

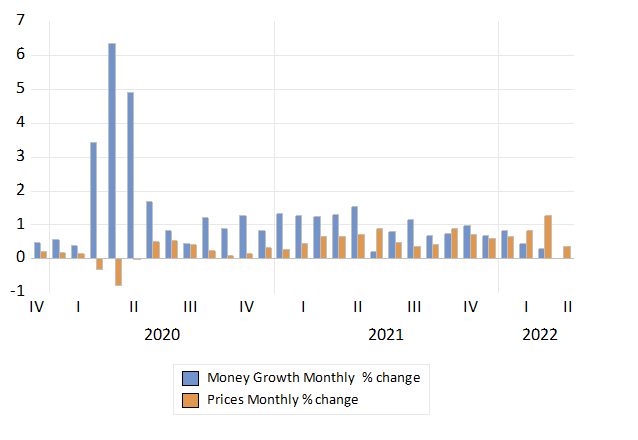

Monthly % Growth in US Money Supply (M2) and Consumer Prices

Global stock markets have done well for investors over the years. We look at what will be required for them to continue to do so.

The compounding growth of the West is powered by business enterprises and savers share in the wealth created.

The economic history of Western economies is an admirable one. Their standard of living has been transformed over the past 200 years by consistently positive year-by-year growth in output and in incomes per head, despite the rapid growth in population over the same period. And all of this was achieved despite the destruction of life and capital, buildings and valuable infrastructure by periodic wars. The Russian war in Ukraine is an awful reminder of how destructive war is. It will take many years of sacrificing consumption – of saving and productive investment in capital equipment and infrastructure – to make up for these losses.

Privately owned businesses are responsible for much of the growth in incomes earned, and in the extra goods and services supplied to the western economies over time. Their most decisive stakeholder is the consumer of this growing cornucopia of goods and services that they produce. Their owners earn a surplus after all contracted-for costs of production have been met and revenues have been collected. There is the risk of a loss, though a growing economy makes losses less likely. More efficient businesses will also compete on the prices for and quality of goods and services they provide their customers, at the possible expense of the revenue line. Improvements in the productivity of capital will be widely shared.

A stock exchange enables the ownership rights in larger businesses to be widely and conveniently shared and traded. It provides the average saver the opportunity to plug into these surpluses and the wealth-creating machine of immense force that is business enterprise, mostly via their pension and mutual funds. These widely dispersed owners have realised much more wealth creation than they would have done by investing their savings in the money market, bank deposits or in the bonds and bills issued by governments. And they would have done even better had they further postponed consumption and reinvested the dividend income they received, as well as conserving their capital gains by staying in the stock market.

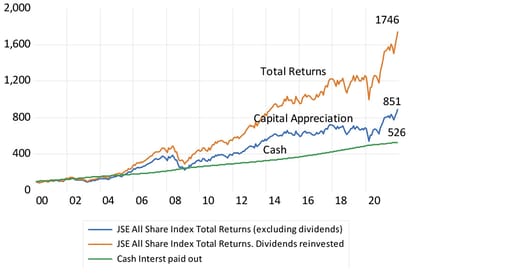

The JSE, very much part of a global capital market, has provided comparably excellent returns over the many years of its existence and has repeated the performance this century. As illustrated below, the average annual total returns with dividends reinvested from the JSE since 2000 have been nearly twice as high as the interest earned on cash and paid out: 13.5% annually vs 7.6% annually. The compounding effect has been so powerful because the returns on extra capital invested by privately owned businesses have been so positive. Economists therefore go further, given past performance. They regard these high expected returns over the long run, as part of the cost of capital employed. They add these higher expected returns to the returns that should be required of any company contemplating an investment decision. It is called the (expected) equity risk premium. If the proposed project cannot promise to leap over this higher hurdle of required returns on capital, the advice is not to go ahead.

JSE All Share Index, with or without reinvesting dividends, and money market returns (three-month Johannesburg Inter Bank Rate) (2000 = 100)

Source: Iress, Bloomberg and Investec Wealth & Investment, 9 May 2022

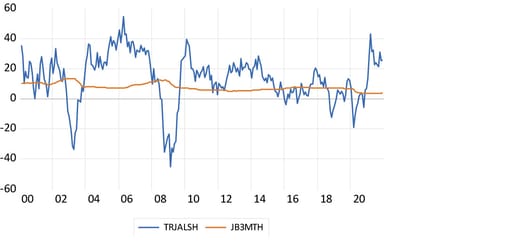

JSE All Share Index total returns vs cash (three-month Johannesburg Inter Bank Rate) 2000 to 2021

Source; Iress, Bloomberg and Investec Wealth & Investment, 9 May 2022

It is not only returns that matter – so does risk. Human nature says (expected) return and estimates of risk are positively related.

So, the obvious conclusion would seem to be to invest in the stock market, since, based on past experience it can be expected to perform well in the long-term, even if there are some short-term blips. It is these short-term blips however that discourage investment in the share market. Between 2000 and 2021 the annual total return on the JSE was 13.5% a year and that provided by the money market was a much less 7.6% a year return on average. However judged by the movement about this average return, the JSE was nearly seven times as risky, as measured by the standard deviation about these returns (see figure above) – the risk that your shares may be worth much less in a few days or months, when you might be forced by circumstances to liquidate your wealth. This can be a major deterrent to share ownership.

The greater the risk aversion, the less comfort wealth owners and potential share owners have in the outlook for assets, the less time they wish to spend in the stock market, the less valuable businesses become. And the greater will be the risk premium earned by those willing and able to stay in the stock market. Bearing extra risk will likely bring extra returns because the entry price to the share market is reduced by the risk aversion of other potential investors. It has been true of the share market over the long run and market volatility, or risk, is likely to continue to negatively influence the long-term value of shares, so improving realised rates of return for those with an extended time in the market.

Albert Einstein famously described the power of compounding interest or returns as the “eighth wonder of the world,” saying, “He who understands it, earns it; he who doesn’t, pays for it.” This powerful force of low-digit exponential growth, of growth compounding on growth, year on year, is well demonstrated by the long-term ability of the major stock exchanges to grow wealth for shareholders in a consistent way over the same long run.

It is the return on owners’ capital that is the source of all interest income

But where do these good compounding share market returns come from? From businesses who are entrusted with much of the accumulated savings or wealth, described as capital employed in any market-led economy. The owners and managers of businesses are incentivised to husband scarce capital, as best they know how. The rate of return they realise on the capital employed, the productivity of that capital, is the foundation upon which all rewards from saving and owning capital or wealth is built. Firms experiment continuously in improving the return on the capital they utilise. They aim to improve the relationship between the cash value of the resources they invest in, called operating costs and what comes out as revenues, and they apply their fixed and working capital to the purpose. The results of such efforts are measured, hopefully in a consistent and comparative way, as return on capital employed inside the firm. The rewards for savers who supply the firms with capital to invest, come not only in the form of dividends paid, but in offers of interest payments that firms are able and willing to make to attract capital, in competition with other firms for the same potentially productive capital.

The less risky interest income offered by all other borrowers, the banks and the government, is therefore strongly influenced by the same return on capital realised by the business enterprise that employs a large proportion of the capital available. The banks, the money market funds, or the government as a borrower, would not offer the interest they do, unless the firms were able to earn a positive rate of return on all the capital they utilise and have to compete for. This includes competing for the overdrafts and mortgage loans provided by banks and other financial intermediaries. The higher the expected real returns from all the capital employed in businesses, the more competition from firms for additional capital to invest, the larger will be the real rewards for all saving. Be it named interest or dividends or lease payments or capital gains depending on the financial arrangements agreed to between suppliers and raisers of capital.

The internal return on capital is what is converted into market value and market returns

It is the positive internal rates of return on capital realised by the business enterprise, not share market returns, that reveals the productivity of the capital it employs. The share market in turn translates expected internal returns on capital into current share market values. The market value of the firm should be understood as the present value of future operating or cash surpluses over operating costs, expected from the firm, discounted by the required returns expected from likely alternative investments. The most valuable firms in the market-place – measured as the ratio of its current market valuation to current earnings or better current cash flows – are those firms that are expected to consistently improve their internal returns on capital and to add more capital by doing so. In other words, they are expected to consistently improve the productivity of capital they utilise and are able and willing to attract more capital, both loan and equity capital, to realise the growth opportunity, and to successfully hold the competition at bay that always threatens prices and operating margins.

The two measures of performance (the internal and market returns) are likely to be highly correlated over the long run. But such present value calculations made by the buyers and sellers of shares in companies are subject to considerable uncertainty from day to day and week to week or quarter to quarter. There is uncertainty about flows of revenue, operating costs and returns from alternative investments that determine the discount rate. There are more than enough unknowns to make estimating the future value of a firm or a market of them, a risky business. Risky returns help to direct savings to the lower return, less risky alternatives, for example to cash or cash like assets.

Knowledge (technology) improves the productivity of capital. Will it continue to do so, and will shareholders receive as valuable a share of the surplus generated?

The force that has driven the extraordinary and consistently unpredicted improvements in income and wealth and in the supply of goods and services delivered, is the success of technology and its application by the business organisation in sustaining and improving the (internal) return on capital, year by year and decade by decade. From railroads to electricity to the motor car, computers and the internet, technology has provided the opportunity to improve returns on capital and increase incomes and wealth, of which a large part is held in the form of shares of companies. A further explanation for consistently good returns to capital over time is perhaps that technology has consistently delivered more than most investors thought technology would deliver over the last two centuries. Stock markets have done so well because the productivity improvements from innovative technology have been at least what the market hoped they might deliver, and consistently delivered at least the productivity enhancements that it is expected to deliver, and typically considerably more. We have had few technology disappointments and technology has overwhelmingly surprised on the upside.

Will technology continue to consistently surprise on the upside in future and benefit the owners of the representative business enterprise and its customers and employees (and government treasuries) in the same way it has done over the last 200 years? There are some caveats.

Productivity has been dramatically driven by improving and ever cheaper computer power. Moore’s law, which predicts that computer power per dollar invested in a chip will increase at an exponential rate, has been shown to be approximately true for around 50 years. But such increases in the power of computer chips must necessarily face physical limitations because of the finite nature of matter.

Similarly, can one assume that the efficiency of food production will continue to improve at the rates it has in the past? The finite resources of planet earth may put a brake on the pace of technological improvement (unless we extend ourselves by settling the planets and beyond, and investing in knowledge itself may defeat the law of diminishing returns). Moreover, will humanity attach as much importance to increasing further our command over goods and services through productive capital expenditure as much as we have in the past and tolerate the share of output going to owners of capital as we have in the past? Capital and its application may be given a lower priority and if so, growth rates will subside.

That the SA economy has performed quite as poorly as it has in recent years is not easily explained. The rate of growth of less than 2% a year represents a very poor outcome, with alas little prospect of any lift off, according to the economic forecasters in and outside government. Yet there are more corrupt economies with much less of an endowment of capital and skills that grow faster.

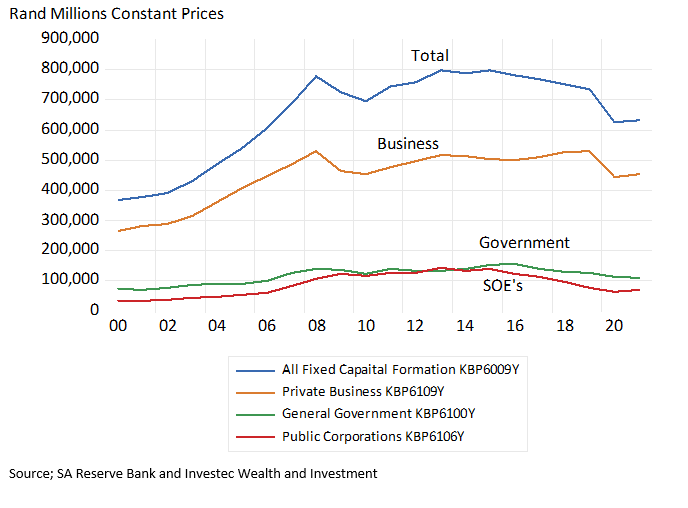

Fixed capital formation and employment offered by private businesses is at best in a holding pattern – capital formation being maintained at levels first reached in 2008. Capital formation by the public sector is in sharp decline- necessarily so – given past performance. The unwillingness of SA business to invest in future output and income generation and in their workforces – describes slow growth – but does not explain its causes. Such reluctance needs to be understood and addressed if the outlook for the economy is to improve.

Fixed Capital Formation Constant 2015 Prices

Source; SA Reserve Bank and Investec Wealth and Investment

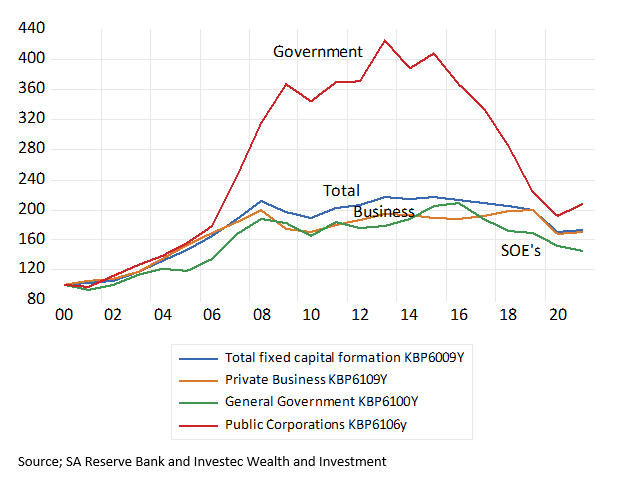

Total Real Fixed Capital Formation (2000=100)

Source; SA Reserve Bank and Investec Wealth and Investment

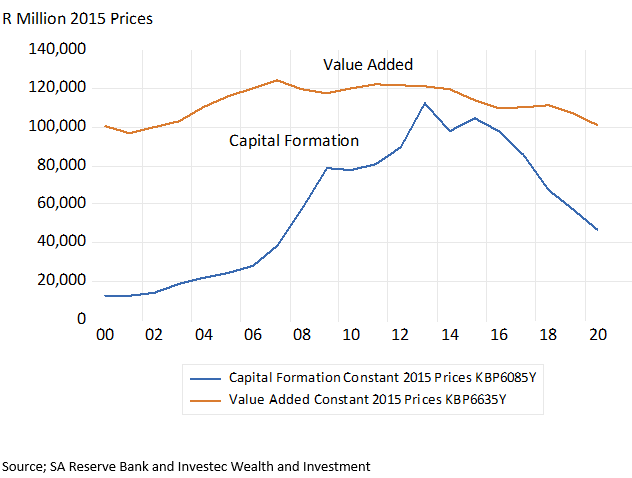

We need look no further for a large part of the explanation of unusually slow growth than to the disastrous failures of the SA public sector. South Africa relies heavily on the State as a producer of essential services, including electricity, water, transport, ports and education. More heavily than is wise or necessary. The inability of Eskom to meet depressed demands for electricity clearly sets limits to growth as do the failures of Transnet to run the railways and ports anything like competently.

These operational failures have meant very large amounts of wasted, taxpayer and consumer provided capital and opportunity. The relationship between what has been spent on the large new electricity generating stations Medupi and Kusile and what has come out as additional electricity is especially egregious and damaging. As much as 1.1 trillion rands was invested in electricity, water and gas between 2000 and 2021. Much of it in electricity generation. Shockingly, almost unbelievably, the real output of electricity etc. has declined by 20% since 2000.

Electricity, gas and water. Capital Formation; Constant (2015) and Current Prices

Source; SA Reserve Bank and Investec Wealth and Investment

Electricity, gas and water. Capital Formation and Valued Added 2000- 2020. Constant 2015 Prices

Source; SA Reserve Bank and Investec Wealth and Investment

The abject failures of other government agencies – of the provinces and in particular municipalities – to maintain the quality of the essential services they are tasked to provide, water, roads, sewage, building plans, education training and health care etc. has become ever more destructive of the opportunities open to business and households. Such failures are also reflected in the declining real value of the homes South Africans own –a large percentage of the wealth of the average household – which has made them less able and willing to demand additional goods and services from SA business.

Hopefully the economy will not stay on these destructive paths. Restructuring the ownership and incentive structures facing the public sector is an obvious and urgent requirement for faster growth- for more capital formation of the human and physical kind. As is reducing the reliance on the public sector to deliver the essentials.

But we need a meta explanation and understanding of why the public sector has failed South Africans so particularly badly to move forward. The key political objective on which the public sector leaders were evaluated was clearly not the efficient use of resources, with quality of delivery related rewards, within sensibly constrained budgets. The Scandinavian model, if you like, did not apply. The primary objective set the new leaders of the public sector – and for which they were presumably judged and rewarded – was the transformation of the racial character of the public sector workforce.

It is an economic truism that you get from people (managers and workers) what you pay them for. This key performance indicator, transformation, has been achieved with huge waste, financial and in foregone opportunities. Losses that were exaggerated by the opportunities the lack of attention to the costs of operations, and their value to consumers, offered for theft, fraud and the patronage of the incompetent.

The continued enthusiasm for demanding that the private sector to transform further and faster seems uninhibited by any comparison of the cost and benefits of forcing transformation. There is perhaps one consolation in all this- the private sector cannot ignore the bottom line in the way the public sector was able to do for so long.

A growing number of employers have insisted that their employees must come back to their work- places. Elon Musk, has demanded that Tesla or Space Ex staff spend at least 40 hours in their offices and that those who do not want to do so “…. Should pretend to work somewhere else…” He also wrote “Tesla has and will create and actually manufacture the most exciting and meaningful products of any company on Earth, this will not happen by phoning it in.” Many other firms, feel the same disillusionment.

WFH is an option – not a compulsion. But an option modern technology has now made possible in ways that were not possible before. Homework was hardly unknown before. Writers, composers and artists as well as weavers and sewers, home bakers, worked from home long before the gig-workers who congregate at the internet café. You may you noticed how the coffee mavens all look up from their laptops to appraise the new arrivals? Seeking company no doubt that they could find at the water cooler.

Being able to measure accurately the relationship between how they reward their employees and how much they contribute to the output and profits of the firm is an essential responsibility of any business. It could not hope to survive without accurate calculations of the costs and benefits of alternative working arrangements. And the firms faced with WFH preferences have been learning by doing as they always do.

It can be assumed with great confidence that the great majority of employees will be paid no more or less than the value they will be expected to add for their employer – be it from the office or home. Furthermore, as clearly, nobody will be rewarded for the time they spend commuting. It is paid for in income or leisure sacrificed by the commuter. Recent evidence that the revealed willingness to go back to the office in the US is inversely related to the time spent commuting is no surprise. The lucky winners from the enforced lockdowns have been those who to live far from the office – that they chose to do for – their own good reasons – pre the lockdowns.

Employers are not the only party with the right to choose where best to work. Workers will make their own choices. The ratio of job openings to work seekers in the US has never been higher and the opportunity to work from home has not been greater this century.

The Tesla office worker who has remained in California, even though the Tesla office is now in Texas, may well tell Elon what to do with his job. They may even accept a lower salary to WFH – the cost of the commute is their bargaining chip. As is the saved rental and all other not at all insignificant costs of supplying an office desk that may improve their case to WFH. They may even be able to do two jobs from home- as many do- given the time freed up and the absence of supervision or whistle blowers. Elon and other collaboration mindful employers may have to offer a premium to get the preferred workers to the office- if they are more productive there.

The individual households who choose where and how they live will help determine how the world of work will look in ten years or more. The developers of offices and homes and retail space will respond rationally to the choices and ongoing experiments of all those who hire and supply labour of all kinds- billions of decisions will prove decisive. The world of work and production evolves continuously, usually in an imperceptible way, to the signals provided from the market for labour. There is no design – just efficient outcomes. Employers no longer requiring office workers to attend on Saturdays, or offering extended annual holidays, are not providing charity but are making a considered response to market forces- necessary to attract workers of the right kind and at the right price. They will continue to respond accordingly.

The responses to the opportunity to work from home that technology has made possible- and made the lockdowns possible – will evolve sensibly and rationally. Provided freedom to choose is respected as the essential ingredient for a successful, highly adaptive economy.