https://podcasts.apple.com/za/podcast/the-monocle-banking-podcast/id1714449953

Month: December 2023

Busting the compound returns myth

Looking closely at the Foreign Exchange and Cash Reserves of SA. There are no free lunches.

The RSA can hope to raise tax revenues at a faster rate and reduce the pace at which government spending is growing to escape the debt trap. Reversing the direction of government spending and revenues is made very difficult by a stagnant economy. But there is also another way. That is to sell assets owned by the government. Not only could asset sales or leases be a source of extra income for government to replace extra borrowing and interest paid, but it could also be a most valuable exercise in the broad public interest. Regardless of how much the asset sales would fetch which after much neglect might need much maintenance and repair.

The assets would be made to work much better in private hands and with private business interests managing the outcomes for a bottom line- as private owners are empowered to do. The assets would come to be worth more and their owners and service providers, including employees, would increase their output. Incomes and taxes. Sadly the status quo, the well rewarded private interests of the managers, workers and especially those of the suppliers of services and goods to the state owned enterprises on highly favourable corrupted terms stand in the way of the pursuit of a broad public interest.

But there is another way. That is to sell assets owned by the government. Asset sales or leases could be a source of extra income for the government to replace extra borrowing and interest paid. Regardless of how much the asset sales would fetch, they would be made to work much better in private hands. The assets would come to be worth more and their owners and service providers, including employees would increase their output. Incomes and taxes paid.

Do the foreign exchange reserves managed by the Reserve Bank on behalf of the government fall into this category of assets that could usefully be sold down? It is possible to hold too much as well as too little gold and foreign currencies on the national balance sheet. They are held as a useful reserve against unforeseeable contingencies. That is a possible collapse of exports or capital inflows, or a flight of capital that would make essential imports unobtainable or foreign debts and interest unpayable.

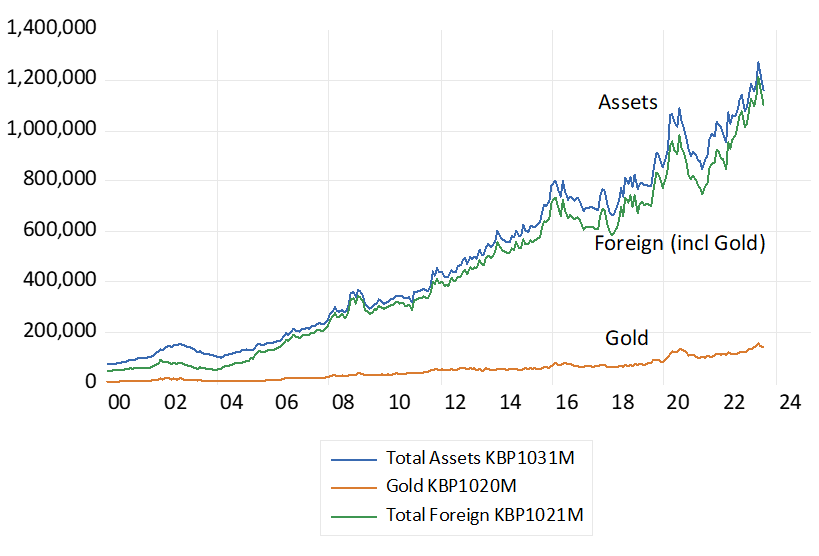

South Africa’s foreign assets have grown strongly over recent years, in current rand value. Since 2010 these reserves have grown from R299 billion to the current levels of approximately R1200b. But when these reserves when measured in foreign purchasing power, in US dollars, while they have doubled since 2010, they still only amount to 62b dollars. There are not many battleships or jet fighters you can buy with that loose change.

Much of the growth in the stock of reserves is the result of a weaker rand. Which is accounted for in the SARB books by mark to market value adjustments of their higher rand values. Which currently have an accumulated value of over R400b. They are described as the Gold and Foreign Asset Contingency Reserve and is recorded as a liability to the Government on the SARB balance sheet. On any consolidated Treasury and SARB balance sheets these assets and liabilities cancel out leaving only the market value of the forex reserves as a net government asset. As SARB Governor has pointed out, these reserves would have to be sold to realize any value.

The other R800 of foreign assets on the SARB balance sheet originally come from the positive flows on the balance of payments when the Reserve Bank buys dollars in exchange for deposits in rands at the Reserve Bank. The extra foreign asset held by the SARB is then held in the form of a dollar or other foreign exchange deposit in a foreign bank. The extra liability is a (cash) deposit at the SARB.

In recent years the source of extra dollars supplied to the SARB is very likely to have come from the Government Treasury rather than the private banks and their customers. A flexible exchange rate will have balanced the supply of and demand for foreign currency transactions that originate in the private economy. The extra dollars acquired by the Treasury will have been borrowed by the government offshore or have been the result of flows of foreign aid or concessionary finance provided SA. And then sold by the Treasury to the Reserve Bank for an additional credit on the Government Deposit Accounts with the SARB.

The Gold and Foreign Assets of the South African Reserve Bank. R million

Source; SA Reserve Bank and Investec Wealth and Investment

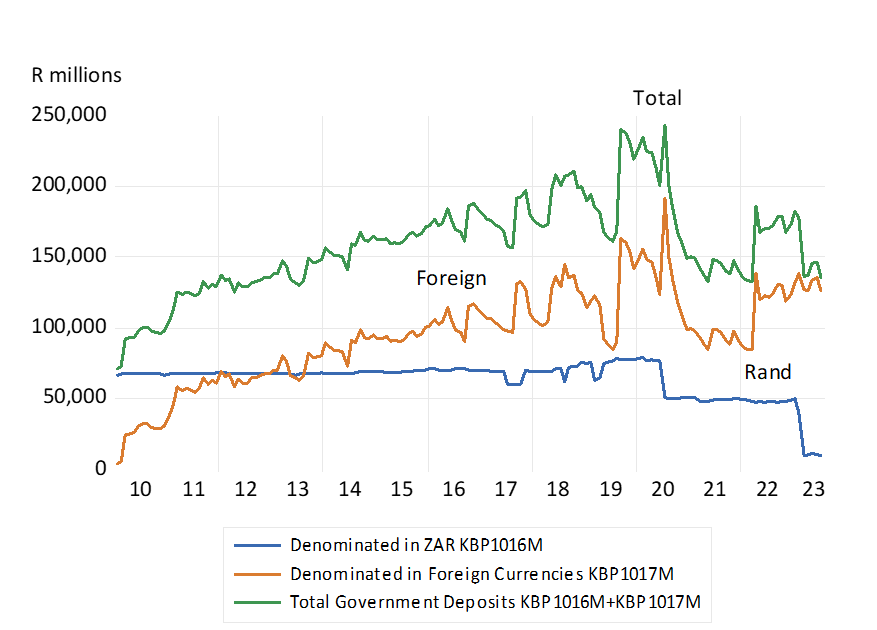

It is striking how rapidly the Government Deposits with the Reserve Bank, deposits denominated in foreign currencies and rands grew since 2010. Though these cash reserves peaked in 2020 at close to R250b and have been drawn down sharply in recent years. It may be asked why these cash reserves need to be as large as they are? Why expensive debt must be raised by the government to hold cash.

Yet running down the Treasury deposits to spend in SA increases the cash reserves of the banking system. The SA banks now hold large amounts of excess cash reserves- upon which they earn now high market related interest rates. Should however the banks turn the extra cash into extra bank lending the supply of bank deposits, the money supply, will grow rapidly and encourage inflation. It is a possibility that will bare close attention.

SA Government Deposits with the South African Reserve Bank

Source; SA Reserve Bank and Investec Wealth and Investment

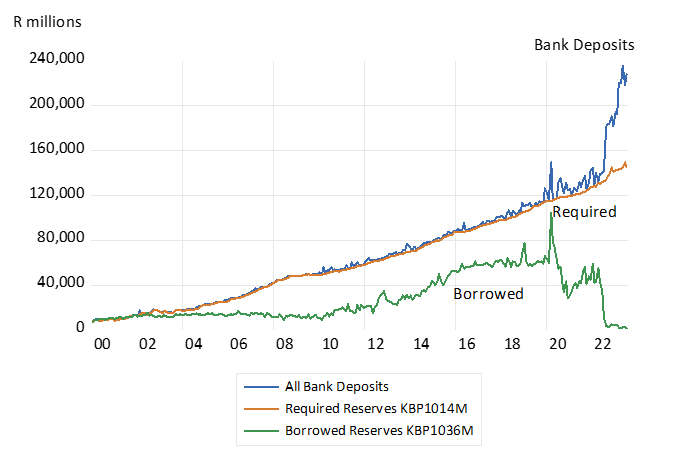

SA Private Banks; Required and Actual Deposits with the Reserve Bank and Cash Reserves Borrowed (to August 2023)

Source; SA Reserve Bank and Investec Wealth and Investment

Who do we thank- the Federal Reserve Bank?

South Africans this week benefitted from a powerful demonstration of our integration into global capital markets. On Tuesday November 14th, the interest yield on the key ten-year US Treasury Bond fell by about 20 b.p. from 4.63% to 4.44% p.a. By the end of the day, the 10 year RSA bond yield had declined by the same 20 b.p. from 11.66% to 11.45% p.a. The yield on a RSA dollar denominated five year bond fell from 7.52 to 7.19 per cent p.a. leaving the yield spread with the US TB, an objective measure of SA sovereign risk, slightly compressed at 2.76% p.a. The dollar weakened across the board. And with higher bond values the share markets almost everywhere responded very agreeably for investors and pension plans. The JSE gained nearly two per cent on the Tuesday (5% in USD) and again by a further near 2% on the Wednesday.

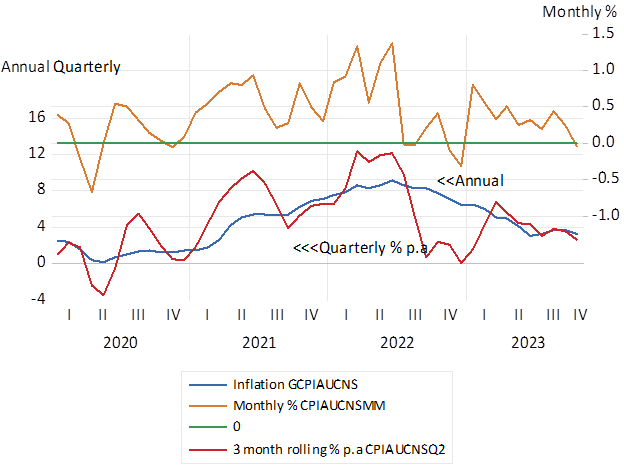

All this on the news that inflation in the US had fallen to by a little more than had been expected after the CPI remained unchanged in the month. The chances of further increases in short term interest rates therefore fell away as they have in SA. And long rates moved in sympathy. Should the US economy slow down sharply as slowing retail spending as strongly suggested in a print released on Thursday, declines in US short rates will follow in short order adding to dollar weakness and rand strength. Or at least as investors, if not yet the Fed, thinks.

US Inflation; Annual, Quarterly and Monthly

Source; Federal Reserve Bank of St.Louis and Investec Wealth and Investment

All it might be thought as much ado about relatively little- a mere blip on the CPI. If you could predict nominal US GDP and interest rates over the next ten years you would be able to predict share and bond values with a high degree of accuracy- if the past is anything to go by. Predictions that will not be much affected by the failure of the Fed to manage inflation during the Covid lockdowns. Or by what has been its near panic and confusing rhetoric in dialing back inflation. That so roiled the equity and bond markets in 2021- and 2022, a strong bull market in most of 2023 has yet to fully recover from.

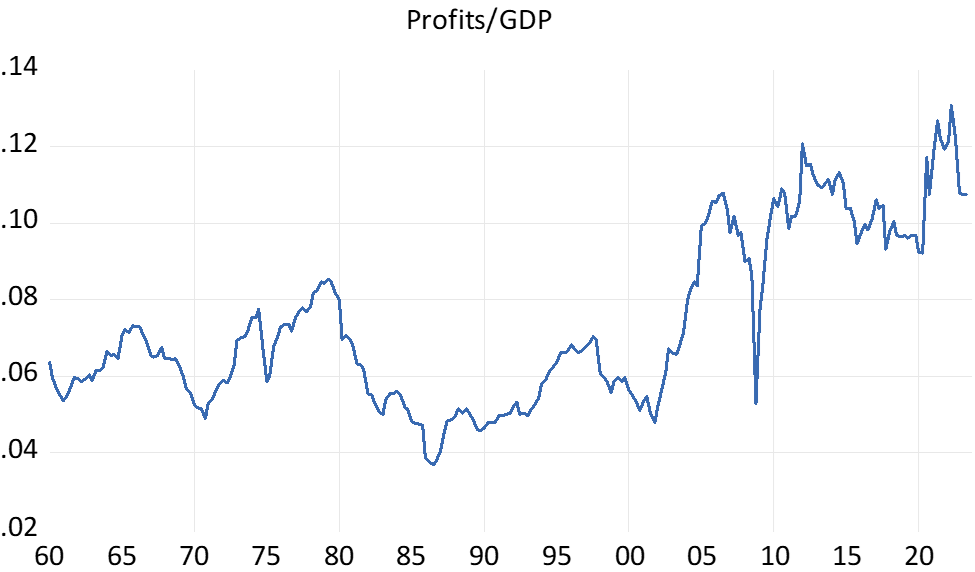

Perhaps the most intriguing feature of recent trends in the US GDP has been the growing share of Corporate Profits after taxes in GDP. The ratio of these profits to GDP- have nearly doubled since the early nineties. A profit ratio that investors must hope managers, with the aid of R&D, in which they invest so heavily, can defend to add to share values.

Another question about the long run value of US corporations and their rivals elsewhere will be about the cost of capital by which their expected profits will be discounted. A puzzle is why have long term interest rates in the US have increased as much as they have this year? It is not more inflation expected that have driven up yields. They have remained well contained below 3% p.a. despite higher rates of inflation. Quantitative tightening – the sale by the Fed and other central banks of vast amounts of government bonds bought after the GFC and during Covid, is surely part of the explanation.

But it is not only vanilla bond yields that have risen this year. Real yields- the inflation protected bond yields – have risen dramatically this year. From near zero earlier in 2023 to their current over 2% p.a. Clearly capital has become not only more productive of profits in the US – it has also become more expensive in a real sense, to counter productivity and profit gains when valuing companies. Will it remain so? That is the trillion-dollar question.

US Share of after tax corporate profits in GDP.

Source; Federal Reserve Bank of St.Louis, Investec Wealth and Investment

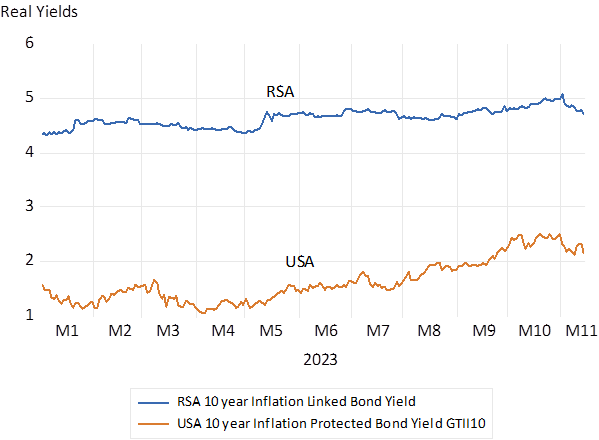

The gap between real interest rates in SA where a very low risk ten-year inflation linker offers over 4% p.a. – making for very expensive capital for SA corporations, and the US – has narrowed sharply. Surprisingly perhaps, real interest rates in SA have not followed global trends. Making for at lease relatively lower costs of capital for SA based corporations, good news, which we can hope will lead to more investment.

Inflation Protected Real Bond Yields RSA and USA – 10 year bonds

Source; Bloomberg and Investec Wealth and Investment

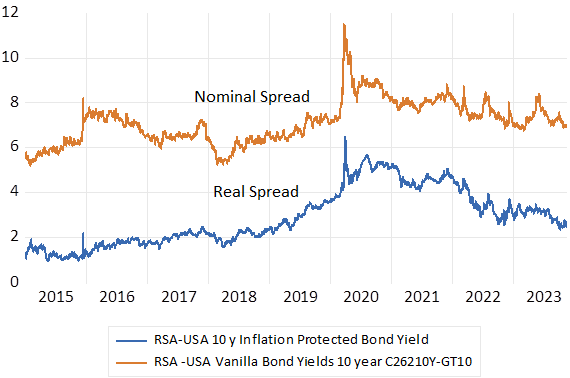

Risk Spreads – RSA-USA 10 year Bond Yields

Source; Bloomberg and Investec Wealth and Investment