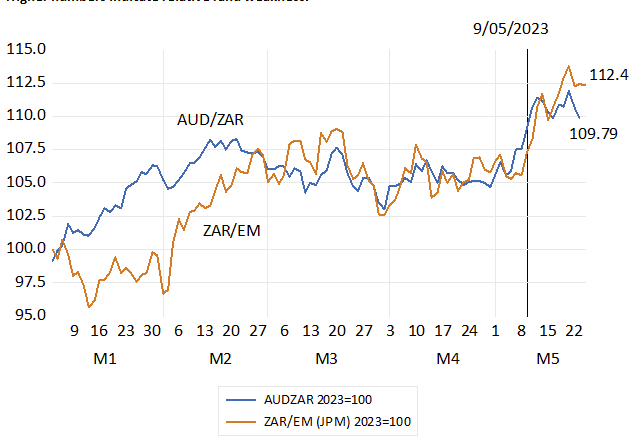

The latest shock to the SA currency and bond markets is of a large scale, similar to those of 2001, and of 2008-9, that was linked to the Global Financial Crisis, also to the Zuma-Nenegate shock of 2015-16, and the Covid shock of 2020. This shock is entirely of our own making. It is the punishing result of a failure to keep the lights on and choose our friends more carefully. We can assert this not only by reference to the abruptly higher rand costs of a USD or Euro, but by the poor performance of the ZAR against other emerging market (EM) and commodity currencies. A weakness that was pronounced earlier in the year as load shedding increasingly hurt the growth prospects of the economy and that was accentuated on the news of our arms business with Russia. The ZAR this year to the 24th of May, after a further burst of weakness on the 10th May, is about 10% weaker Vs the Aussie dollar and 12% weaker Vs the JPMorgan Index of EM exchange rates.

Fig.1 Relative performance in 2023 ; ZAR VS AUD and EM Index; Daily 2023 to 24th May 2023. (2023=100) Higher numbers indicate relative rand weakness.

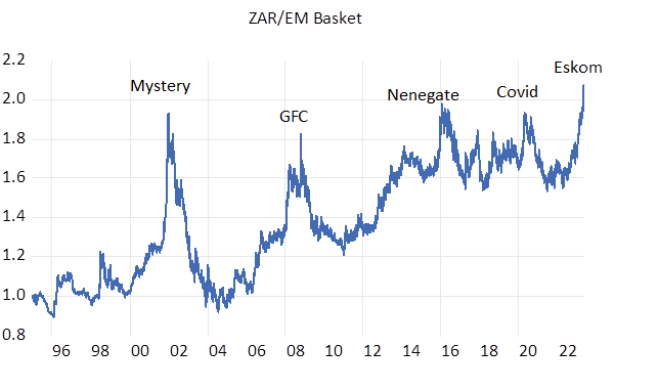

The ZAR compared to a basket of seven EM currencies – the ZAR/EM ratio – has never been weaker than it is now. The ratio very easily identifies the periodic shocks to flows of capital to and from SA since 1995. One can only hope that this time will not be different and that the ZAR bounces back- at least relative to our peers.

Fig.2. Identifying SA specific risks- comparing the behaviour of the USD/ZAR exchange rate to that of a basket of EM currencies. Daily Data 2000=1 to 15th May 2023

Higher ratios indicate relative rand weakness

Source; Bloomberg and Investec Wealth and Investment.

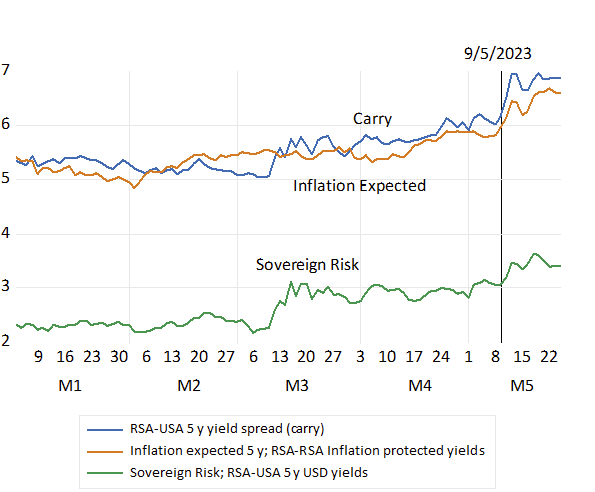

The RSA bond market could not escape similar punishment. Yields on long dated RSA Rand and USD denominated debt rose by about 60 b.p. between the 9th and 15th of May having all tracked higher through much of 2023. The case for investing more in SA plant and equipment has become that much harder to make. And the rand -judged by the wider carry- the difference between interest rates in SA and the USA- is now expected to weaken at an even faster rate- despite recent rand weakness. All bad news for our economy

Fig.3 Interest rate movements in 2023. Daily Data to 24th May

Source; Bloomberg and Investec Wealth and Investment.

The weaker rand is not an unmitigated disaster. Exporters and firms competing with more expensive imports will benefit from higher rand prices. Their extra rand costs of production will lag higher rand revenues and until local inflation catches up with the higher rand prices they will be able to charge on

foreign and domestic markets. The window of extra profitability will be supportive of extra output, incomes and employment. And of the rand values of the exporters and global plays (e.g. Richemont or Naspers or the International Mining Houses) listed on the JSE and who account for more than half its market value. The JSE is not in shock- it is well hedged against SA specific shocks.

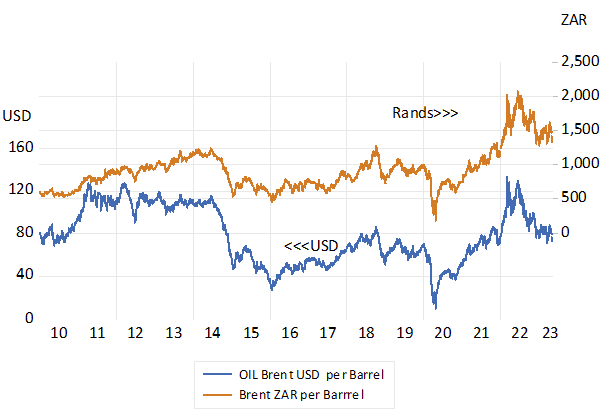

How quickly inflation rises in the months to come will depend on the rand price of imported oil. A saving grace for the inflation outlook is that the dollar price of oil has fallen by more than the rand- hence a lower rand price of a barrel of oil.

Fig.4; Brent Oil price – per barrel in USD and ZAR

Source; Bloomberg and Investec Wealth and Investment

The interest rates set by the Reserve Bank will make no difference to the rand or the inflation rate. Hopefully they will react to an exchange rate shock by not reacting to one. And do what little they can not to slow down growth any further.

The Treasury could help –by keeping the peak loading generators on for longer. And pay for the extra diesel or LPG. Every hour of load shedding not only means less income and output generally – it means lower tax collections. Every rand spent on diesel by the public or on replacing Eskom means less tax revenue in proportion to the company and personal income tax rates and the conversion to solar

allowances. Spending taxpayers rands on diesel will pay for itself. And possibly produce the growth surprise that could turn, only can turn around the rand.