January 27, 2021

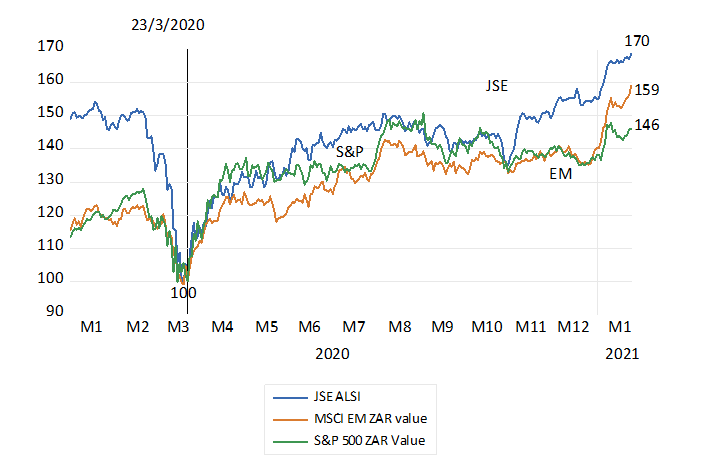

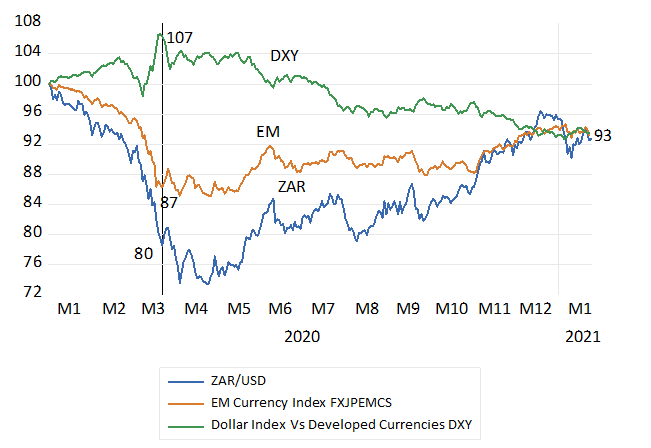

There is some very good news to cheer South Africans up. They are a lot wealthier than they were when the lockdowns were announced in March. And wealthier than they were on January 1st 2020. If their wealth has been diversified through the JSE, the average shareholder will be 70% better off than they were in March. And 13% up on their portfolios of the 1st January 2020. The All Bond Index has returned 31% since March and 9% since January 2020. Those with shares off-shore would also have done well, but not as well. They would be up 59% if they held an MSCI EM benchmark tracker or 46% if they had tracked the S&P 500 March. That foreign holiday plan sadly disrupted in March would now be about 16% cheaper in USD. Since the ZAR/USD bottom of April the mighty ZAR has also done a lot better than the average EM currency.

To what should South African wealth owners attribute their much improved financial condition? The usual global suspects can be interrogated. A weaker dollar in a more risk on environment and so buoyant EM stock markets, to which the JSE is umbilically attached, is a large part of the explanation. A rising S&P 500 is a tide that lifts all boats, though some higher than others, as we have seen of the JSE and the ZAR.

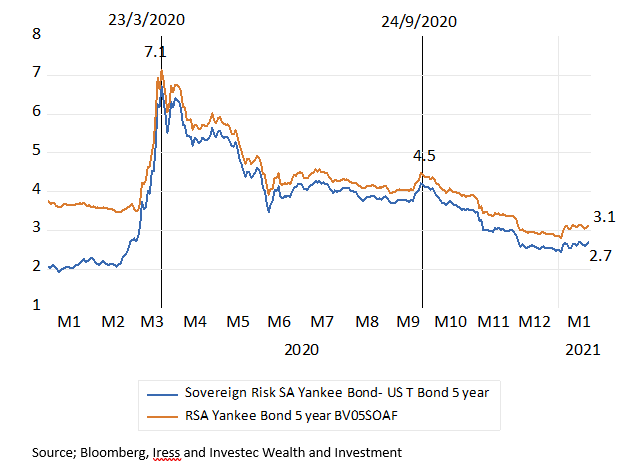

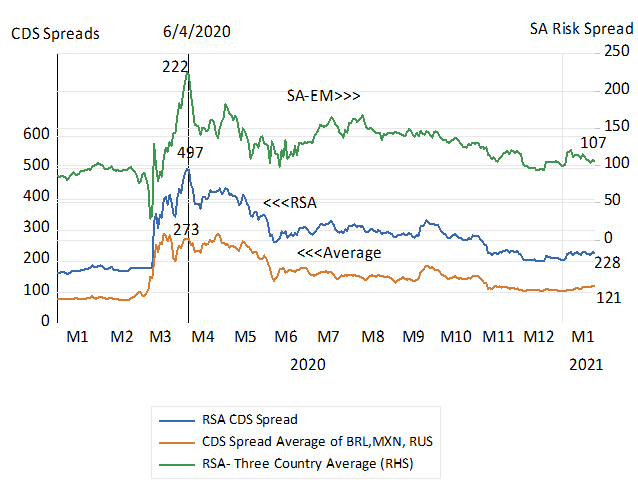

But there are more than global risk-on forces at work. SA specific risks, as measured in global bond markets, have declined, notably so since October. They have also have declined relatively, by more than the risks attached to Brazil, Mexico and Russia bonds of the same duration. In April, at the height of market turbulence, the yield on RSA USD denominated 5y bonds had risen to over 7% p.a. And the risk spread, the extra yield over US Treasuries, was about 6.5% p.a. These bonds now offer 3.1% p.a. and an extra 2.7% p.a. over US T Bonds, less than half their levels in March 2020 with much of the improvement also registered after October. Insuring RSA Yankee bonds against default now costs but 1.1% p.a. more than it would cost to insure the average of Brazilian, Mexican and Russian debt. This extra insurance premium to cover SA default SA was 1.5% in October.

The reasons for lower SA risks are not at all as obvious as the benefits. By reducing risk and helping to add to the wealth of South Africans they encourage more spending needed to encourage output and employment. Lower risks moreover reduce the returns required of business adding to their capital stock in SA, so much more of which is needed to permanently raise output employment and incomes. And tax revenues rise with income.

Such improved prospects will be completely reversed by an additional wealth tax. It will not be expected to be a once off event. It will mean more SA risk and demand higher returns on the cash firms invest, meaning still less capex. It will reduce the value of SA companies so that they can meet such higher required risk adjusted returns for investors and immediately reduce the rewards for saving and the value of pensions. It will encourage the export of the savings of tax paying wealth owners and the emigration of skilled taxpayers. Tighter controls on capital flows would inevitably have to follow that would undermine the depth of our capital markets. Have those who advise wealth tax increases estimated how much collateral damage will be done to tax revenues over the longer run?

The sensible way to fund an unavoidable increase in government spending is to call further on the R160b of Treasury cash held at the Reserve Bank. And to raise a temporary overdraft from the Reserve Bank to supplement this cash balance, should this become at all necessary. Adding more money to the wealth portfolios of South Africans, including to their deposits at the banks, created this way, would further stimulate spending, income growth and tax revenues. It would be growth enhancing and therefore risk reducing.