March 2026.

Mike Tyson famously remarked that a plan was all very useful until you were smacked in the mouth. The SA economy has taken a snot-klap in the form of an oil price shock accompanied by a further shock in the form of a weaker ZAR. An unexpectedly disappointing development but by no means unprecedented. Oil price and currency shocks have been a regular feature of recent global and economic history. Any helpfully realistic plan for the SA economy should include a credible plan to deal with an oil price or currency shock. Do we have one?

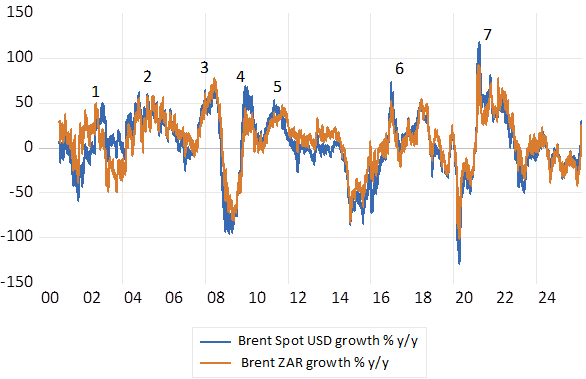

We have often been here before as the oil price cycle in ZAR and USD reveals- though it also reveals that the oil price cycle when measured in USD or ZAR looks very much the same. One can identify at least seven such shocks – in both directions – since 2000. And the stock market reacts in the same direction- share price volatility rises and falls with the oil price. An oil price shock is bad news for SA facing businesses -understandably so – and for their shareholders in pension and retirement funds – because of its negative implications for generating sales and earnings.

Recognising the Oil Price Cycle. USD and ZAR. Daily Data to March 2026

Source; Bloomberg Investec Wealth & Investment

What is our economic plan and how has it been disrupted? The plan is to realise consistently lower inflation ( for all the benefits lower inflation delivers for the long-term growth outlook- easily exaggerated I would add) Yet To achieve lower inflation a helpfully stronger ZAR and stable oil price is essential to the purpose. But both are not at all influenced by SA interest rate settings. The supply side of our economy (the cost of imports) as we painfully observe, is not under our control. Yet the demand side of the economy and its impact on prices can be managed to a degree with interest rate settings.

Policy determined interest rates and the cost of credit for an extended period have therefore been set high enough for an extended period to effectively restrain the strength of the demand side of the economy (to a fault –I would argue). A mixture of demand repression and very welcome supply side support- stable oil prices and a stronger rand with support from much higher precious metal prices and a weaker USD – has helped bring down inflation in 2025. And led us to an inflation target of 3% p.a.

Though despite the severe monetary policy setting there were some encouraging preliminary signs of a cyclical pick up in credit and money supplies and in household consumption spending. By year end 2025 household spending was ticking higher – by about 1.2% more than the quarter before as were the growth rates in money and credit supplies. And perhaps even more important for a sustained upswing, precious metal prices provided good support for the ZAR, the Treasury and the value of pension and retirement funds of the working and retired South Africans in 2025

The chance of a cyclical recovery have now receded sharply- on the assumption that inflation will rise and the Reserve Bank will increase rather than cut interest rates over the next twelve months- as was the market expectation until two weeks ago. The money market is now pricing in about 50 bp higher short-term rates in twelve months. The broader bond market view is also anything but sanguine with interest rates rising similarly- though still below levels of a year ago.

Perhaps realistic expectations but, if they are imposed on a stagnant economy, would surely mean a serious and avoidable policy error. The ZAR, while helpfully little changed over a twelve-month period, has unhelpfully also weakened marginally against the major currencies and other emerging markets.

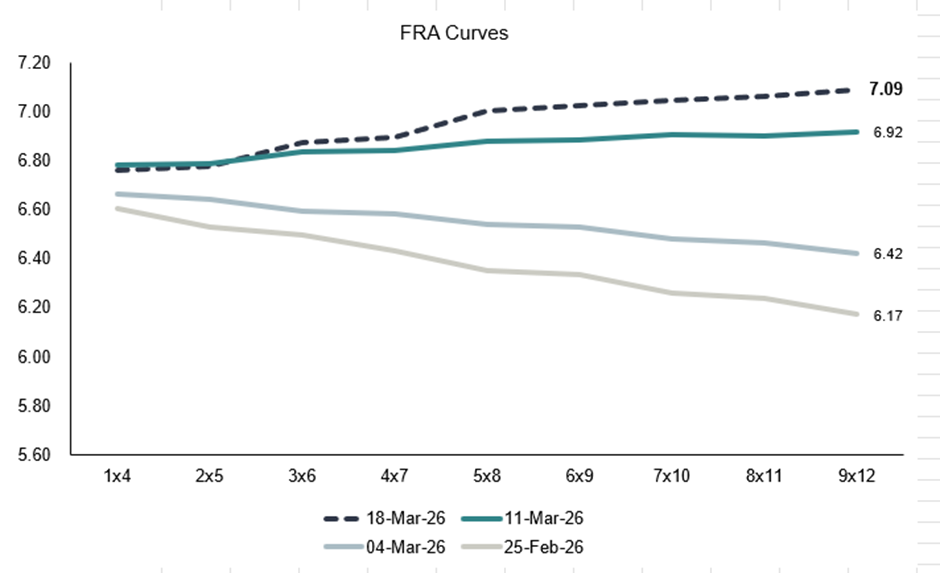

Forward Rate Agreements in the Money Market

Source; Bloomberg Investec Wealth & Investment

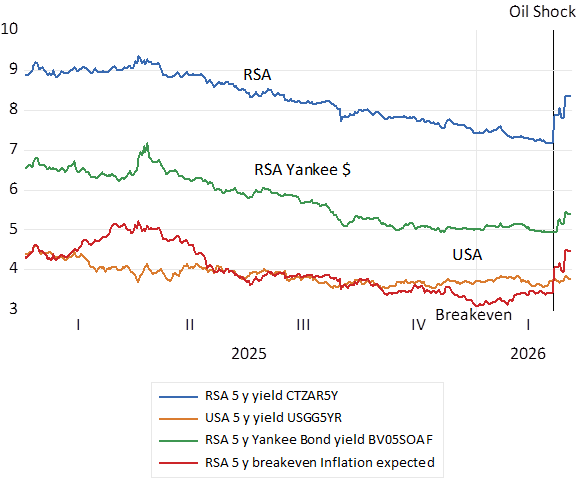

Long dated bonds – five-year RSA and USA Bond Yields and Inflation Expected; Daily Data 2025-March 17th, 2026

Source; Bloomberg Investec Wealth & Investment

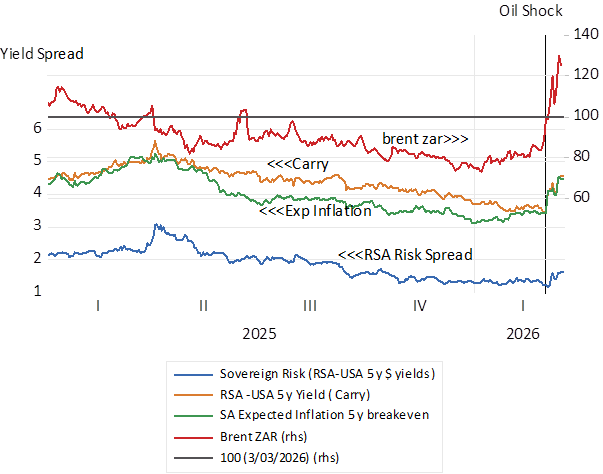

Interest rate trends and the rand oil price (March 2026=100) daily data

Source; Bloomberg Investec Wealth & Investment

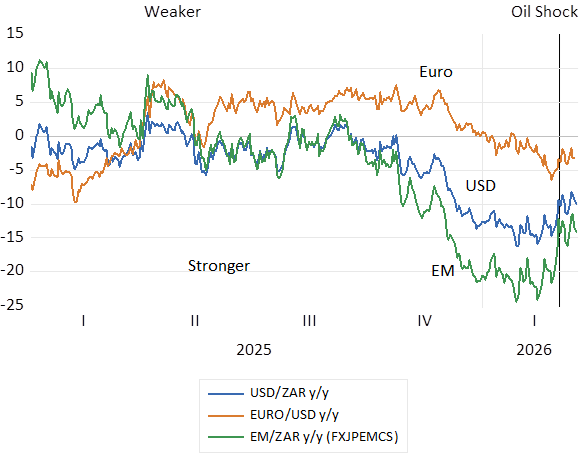

The Exchange Rate Cycle. The annual per cent movement in the ZAR vs the USD, the Euro and the EM basket. Daily Data to March 17th, 2026.

Source; Bloomberg Investec Wealth & Investment

It is not good sense to raise interest rates when a price shock is already damaging disposable incomes and undermining the willingness and ability of households or firms to spend. Adding higher interest rates to the debilitating impact of higher prices- an oil price tax- on spending – adds to the misery. And can have no impact on inflation expected. Inflation and inflation expected will take its cue from the oil price and the ZAR. And judged by past performance- neither the oil price nor the ZAR can be expected to continue in the same direction into an indefinite future. The rational expectation is that these trends must reverse and inflation trends will reverse in the same direction. Wisdom is for monetary policy to stand aside and let it all work out. The broader plan should include a plan to deal with a supply side shock to prices. A plan that ignores supply side shocks to help the economy ride through impact of a temporary increase in prices. By not raising interest rates and expected to do so.

There is some consolation for dependents on the SA economy in current circumstances. We are not dependent on imported oil or gas to generate electricity, as is Europe for example. Domestic coal is the feed stuff for our energy that also provides a domestic source of chemicals and refined petroleum. And renewables will play a more important role in the future. As will electric vehicles. We should have planned for a reserve of refining capacity but appear not to have done so. Should we now optimistically plan for a more stable oil market, one much less disrupted by choke points in the Middle East?