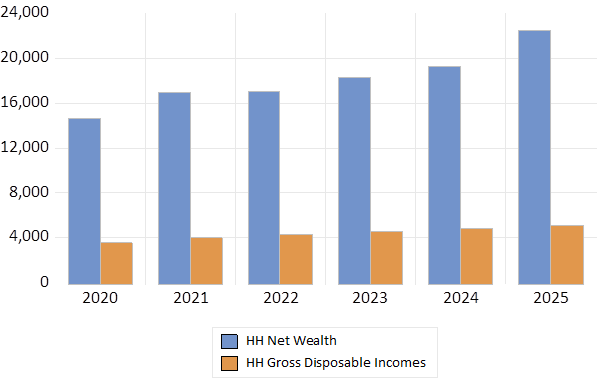

South Africans grew their wealth at a much faster rate than their incomes in 2025. Household assets, less household debt, was 15% larger than the year before. Up by a very tidy R3,200b. The disposable incomes of households grew at a much more pedestrian rate of 4.7% or by R230 billion in 2025. Household spending on consumption goods was 5.7% up on a year before. A respectable real increase given consumer goods inflation of only 2.2% in 2025, so helping the economy along. Nominal GDP grew by 3.9% in 2025 that lost only 2.8% of its purchasing power delivering real growth of only 1% in 2025

Household Net Wealth and Disposable Incomes (R billion)

Source; SA Reserve Bank. Quarterly Bulletin and Tables December 2025. Investec Wealth and Investment

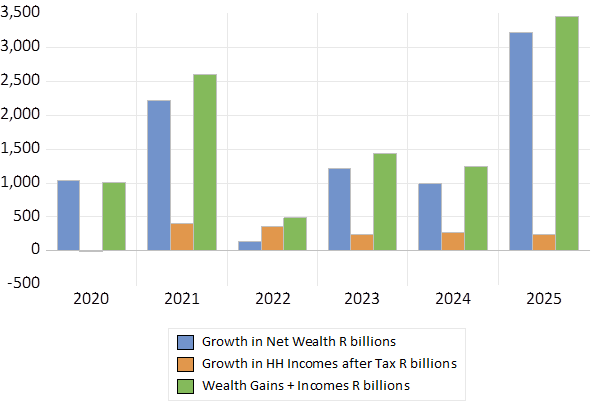

If we regarded the increase in net wealth as income and added it to the disposable incomes of households, the increase in household income, including unrealised capital gains, was close to an imposing 3.5 trillion rand and more than 10 times the increase in disposable incomes last year. The household wealth to disposable income ratio in 2025 was nearly five times- close to the long term ratio.

Growth in SA Household Incomes- including capital gains

Source; SA Reserve Bank. Quarterly Bulletin and Tables December 2025. Investec Wealth and Investment

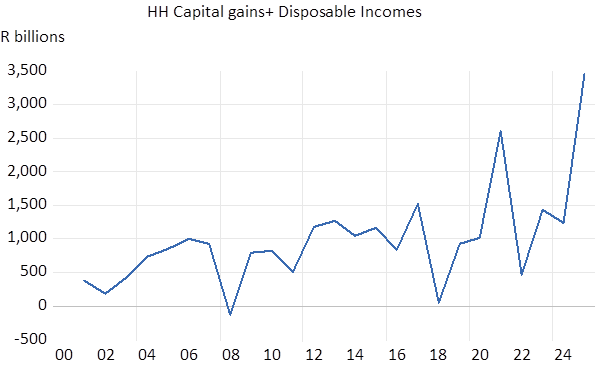

Source; SA Reserve Bank. Quarterly Bulletin and Tables December 2025. Investec Wealth and Investment

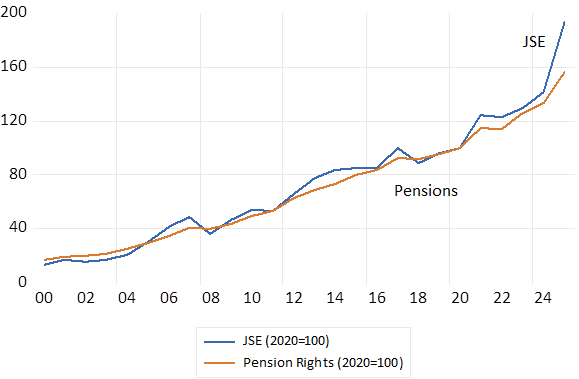

The largest contribution to this impressive increase in the wealth of SA households was the increase in the value of the assets held for retirement. The claims of Households on the pension and retirement funds managed for them amounted to over 9 trillion rand in 2025, having added as much as 1.36 trillion rand to net HH wealth in 2025. Pension fund rights account for about 40% of the net wealth of SA of households and homes about 35% worth about 7.7 trillion in 2025. The value of pension rights closely follows the JSE All Share Index and 2025 was a banner year for the JSE, buoyed as it was by dramatic increases in the prices of precious metals that play a significant role in SA exports and income tax. The JSE returned about 30% in 2025.

Pension and Retirement Fund Assets of Households compared to the JSE (2020=100)

Source; SA Reserve Bank. Quarterly Bulletin and Tables December 2025. Investec Wealth and Investment

The formally employed in SA are mostly required to contribute a proportion of their incomes to retirement and medical aid funds to which their employers often add a contribution which should be understood as a salary sacrifice, not as charity. The share market has served the many employees, who are the owners of SA companies, very well over many years. The shareholders of SA companies, through their pension rights are many and a highly diverse, representative of the work force. They incorrectly do not register as BEE qualifying.

Clearly changes in household incomes that include capital gains are not only much larger than disposable incomes. They are also much more variable, given exposure to financial market forces. Retirement funds moreover are less immediately accessible than income from work or from dividends or interest income that compounds most usefully when reinvested in retirement funds, rather than when paid out and consumed. Banks will lend when secured by incomes. They are apparently much more reluctant to regard pension fund assets as security for their credit. Is this appropriate, to encourage saving up rather than down? By households many of whom live from paycheck to paycheck and incur expensive debt doing so. Cheaper credit would be very valuable to them.

Though households are drawing increasingly, in as far as they are allowed to by the two-pot system, to cash in their pension fund gains. The number of such drawdowns, repeated drawdowns, have been increasing. Though the amounts drawn down to fund current expenditure given the growth in the market value of pension fund assets has not had a significant negative influence on the funds managed. Favourable wealth effects will have helped to stimulate household spending in SA in 2025 and compensated for a general reluctance or inability to commit funds to capex. For want of business confidence to do so and for want of capacity of SOE’s to do so.

Despite the ubiquity of pension funds for the formally employed the distribution of SA’s wealth has surely been less equal than the distribution of incomes. Especially given that so many South Africans, earn or report no incomes at all and rely on the taxpayers to fund their consumption of private and public goods. So reducing significantly differences in actual consumption if not in earned incomes.

But an inevitably unequal distribution of wealth and of the savings of net income, including capital gains, undertaken mostly by the better off has a major upside. It means more capital for the economy to fund productive real capital, plant equipment, infrastructure and also R&D. The higher the ratio of capital- that is wealth to the labour force – the higher will be incomes from work. The rich make their contribution not only by producing and earning more (when earned in the old-fashioned honest way not corruptly) But also by saving more to help fund capex.

Expenditure on consuming goods and services by rich and poor has an opportunity cost. It means fewer goods and services left over to be consumed by others, in the wider community. But saving, accumulating wealth and not spending it all, postponing spending, provides a public benefit. It enables and funds the growth in the real stock of capital. It should be encouraged. As should the incentives to allocate capital domestically rather than abroad.