The Fed will have a new chairman of its Board of Governors. He will have to contend with the outgoing chairman of the Board, Mr. Jerome Powell, continuing to participate in the 12 member meetings of the Open Market Committee (OMC) that sets short term interest rates. Warsh remarked in his Senate hearings that he would prefer more debate and dissonance on the Committee which has been remarkably absent in recent years- “messier meetings without pre-rehearsed scripts”. No doubt he will get more of it if he is prepared to listen.

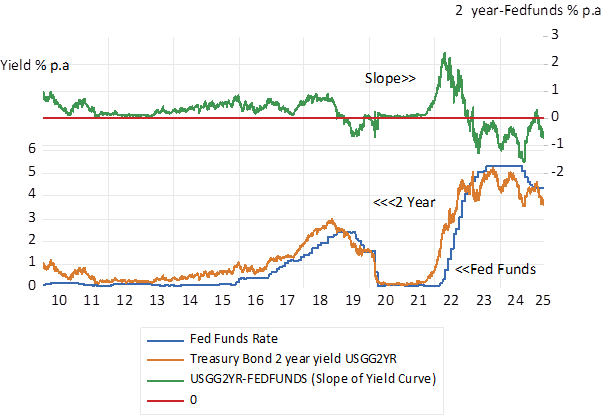

There is enormous attention paid and constant pressure from the politicians for lower rates in the US Borrowers clearly have more political heft than lenders apparently. Yet why short-term interest rates as set by the Fed matter as much as they do in the US is something of a mystery. Given that much borrowing and lending, including mortgage lending, is undertaken over extended periods of time at pre-determined fixed rates. And rates for longer term lending and borrowing can be lower than short term rates. As they have been consistently so in recent years. Because the market always looks ahead and has been acting on the expectation that the Fed will be lowering the short-term rates in the future. (Note below how longer-term rates lead the fed Funds rate)

Fig 1; US Short (Fed Funds Rate and Longer-term rates – US Treasury Bond 2 year yields) Daily Data (2010- 2026)

Source; Federal Reserve Bank of St.Louis and Investec Wealth & Investment

Walsh also indicated that he did not approve of the Open Committee members sharing their views about the future direction of the interest rates over which the OMC exercise control. The argument for doing so is presumably to better inform the market about direction of interest rates so that the Fed would be less likely to disturb the forward-looking actions taken by the market makers. Surely monetary policy should act in a predictable way so as not to surprise the market that will always be doing as well as it knows how to anticipate Fed action? And if its expectations are well informed this will allow for better planning, better debt management and less risk.

Less uncertainty about interest rates, less risk priced into the marketplace, is surely one of the objectives of monetary policy. Economic policy can logically only help fine tune the economy, moderate the business cycle, by acting in advance of the market based on a presumed superior ability to forecast the state of the economy. The economic forecasts of market participants are as likely to be as good as those of the central bankers whose actions will be anticipated and reflected in forward looking forecasts of interest rates and financial markets generally. A market waiting for the Fed to act does not describe reality. A market that anticipates Fed action to avoid losses or make profits describes the forces at work.

Ordinarily data dependence for the Fed and its watchers, as opposed to forecast dependence, will serve the economy well enough. If spending is running observably too hot – driving up prices – the case for raising short-term interest rates – to cool down the economy -is obvious enough and predictable. And vice versa, should the data indicate that the economy could grow faster and more spending, encouraged by lower borrowing costs is called for and will also be easily predicted. The problems arise when prices are rising for supply side reasons. When prices generally are rising because less is being supplied –for example when energy prices or food prices are shocked higher -leading to higher prices generally. Such temporary shocks do not call for higher interest rates. Higher prices act to restrain spending and shocks will reverse. And the best the central bank can do is to do very little – and be expected to do so. This should be the expected policy reactions to supply side shocks.

But the central bank may believe as the European Central Bank and the SARB currently asserts, that a temporary shock to prices may lead to more inflation expected over the long term and hence permanently higher inflation -regardless of the state of demand. My view is that prices do not do simply what they may be expected to do – they depend also on what the market will bear. And a stagnant economy – too little demand – must restrain the prices set regardless of extrapolated expectations. But the playbook for dealing with supply side shocks is by no means agreed either by central banks or their watchers. Which adds to the difficulty of predicting policy reactions adding to market risk.

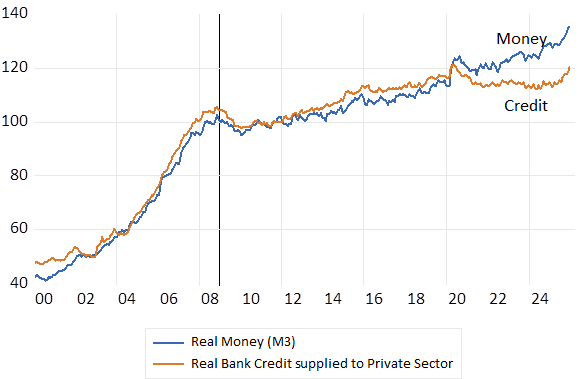

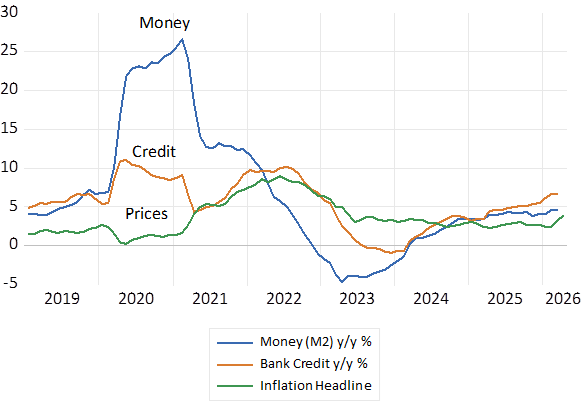

Warsh in its testimony was very critical of the Fed’s reactions to Covid when it believed (quite wrongly) that the shock to prices in 2020 was temporary and did not raise interest rates accordingly “The Fed missed its mark,” he said. “The fatal policy error” of 2021 and 2022 “is still a legacy that we’re dealing with.” What he said is needed now is “a regime change in the conduct of policy,” which “ includes a new inflation framework, new tools and a new approach to communicating its messages” The Fed missed because it allowed a short-term supply side (Covid) shock to supply to be accompanied by an extraordinary increase in the money supply. Caused by large direct transfers from the Federal Government to the bank deposits of households and firms stimulating demand and raising inflation. Central Bankers should know better than to ignore money supply and financial conditions generally when assessing the state of an economy.

Fig. 2; Growth in US Money Supply, Bank Credit and Consumer Prices; Monthly Data (2019-2026)

Source; Federal Reserve Bank of St.Louis and Investec Wealth & Investment

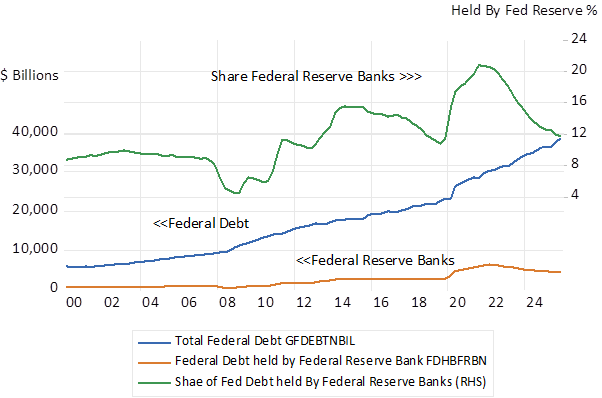

Walsh has more uncomfortable legacies to deal with than a failure to model inflation. He has a balance sheet to manage with a huge load of Federal Debt (some 12 per cent of all Federal Debt) and a US Treasury now spending at close to Covid levels while adding to Federal Debt (now about 120% of GDP) at about a 2 trillion annual rate. Keeping the Fed within a narrow monetary policy lane, as he intends, will test all the acumen and political savvy of the new Chairman.

Fig 3; US Federal Debt and Federal Debt held by Federal Reserve Banks

Source; Federal Reserve Bank of St.Louis and Investec Wealth & Investment

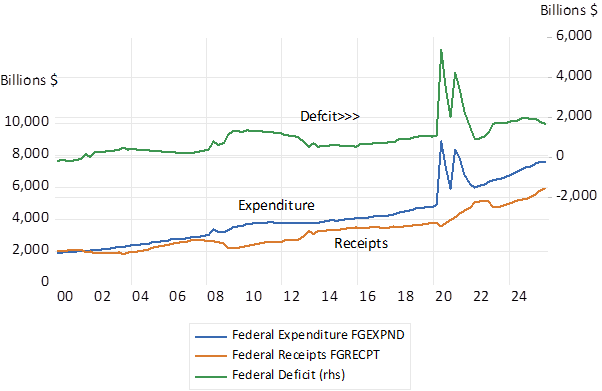

US Federal Government; Expenditure Revenue and Deficits

Source; Federal Reserve Bank of St.Louis and Investec Wealth & Investment