JSE dividends (All Share Index dividends per share) have increased significantly faster than earnings over recent years. The payout ratio (dividends/earnings) that averaged about a steady 40% between 1995 and 2016 has increased to about 60% of earnings. If we leave Naspers, now about 18% of the All Share Index, out of the calculation, the payout ratio is now close to 70% of reported headline earnings. This ratio is unusually high by international and emerging market comparisons.

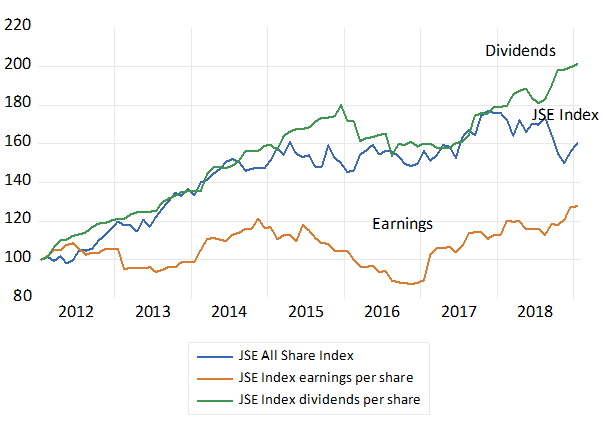

Since 2012 JSE dividends per share in rands have doubled while reported earnings are only 20% higher than they were in 2012. Share prices are about 100% up on 2012 levels and have tracked dividends more closely than depressed earnings. A value gap between dividend flows and the price paid for these dividends has opened up. Our model of the JSE indicates that the JSE may be about 15% below its ‘fair value” as predicted by reported dividends and interest rates (see figure below)

Fig.1 JSE All Share Index, earnings and dividends per share (2012=100)

Source; Ires and Investec Wealth and Investment

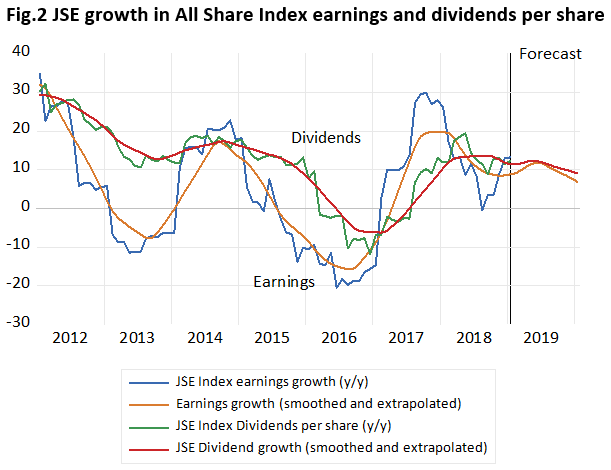

JSE dividends and earnings are currently growing at about the same rate of about 13% p.a. and are forecast to sustain growth rates of about 10% p.a over the next twelve months. (see chart below)

Fig.2 JSE growth in All Share Index earnings and dividends per share

Source; Ires and Investec Wealth and Investment

Should shareholders welcome or disdain this higher payout ratio? If a company has prospective returns from its investment programme that exceed its cost of capital, it should retain all the cash it is generating and invest it back into the company on behalf of its shareholders. Shareholders can only hope to achieve lower market related, risk adjusted returns with the cash distributed to them. If the company can beat this opportunity cost of capital, it should not pay dividends or buy back its shares. Indeed in such circumstances free cash flow ( cash retained after capital expenditure) will ideally be negative rather than positive. A true growth company would be well justified in raising fresh equity or debt capital to fund its expansion and be revalued accordingly with sustainably faster growth in mind.

That SA companies are paying out more of their earnings is both good news and bad news for shareholders and the economy at large. The good news is that paying out more is better than undertaking capital expenditure, including mergers and acquisitions, that cannot be expected to beat their cost of capital and add value for shareholders .

The attempts SA companies have made seeking growth offshore have often proved value destroying rather than value adding. Such attempts typically add unwanted complexity to SA businesses and reduce their value. While they may diversify away some SA specific risks, shareholders are fully able to undertake their own diversification investing directly in offshore companies. They do not need SA managers to do it for them and venture outside their area of competence.

The bad news implication of higher SA payouts is that it reflects an understandable reluctance to invest more in what has become very slow growth South Africa. Such a reluctance to invest more in capital or people (also called working capital) while good for shareholders, inevitably reinforces the slow economic growth under way.

The solution to the problem of high pay outs in South Africa is to get growth going again. Companies will then invest more in growing markets for their goods and services and retain more cash to the purpose. They would be doing more good for shareholders, their customers, their employees and the wider economy.

It is unrealistic to expect SA firms to invest more unless the markets for what they produce can also be expected to grow. It is the spending of SA households that determines the path of the SA economy. It is the consumption egg that leads the investment chicken.

Without the stimulus of lower interest rates household spending will remain subdued. We can only hope a stronger rand and consequently less inflation will allow the Reserve Bank to help the economy along – rather than stand in its way.