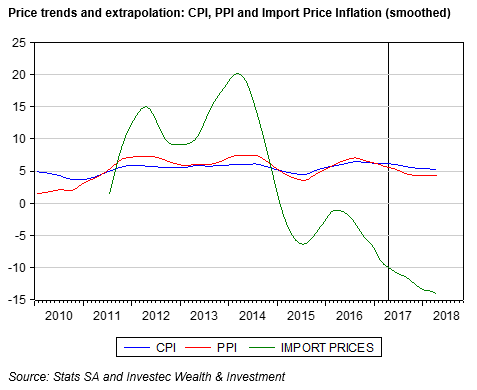

The SA economy has begun to offer a few glimmers of cyclical light. Of most importance is that industrial metal prices have continued to recover from their depressed levels of mid-2016, as we show below in figures 1 and 2. The London Metal Exchange Index, in US dollars, is up 20% on its levels of January 2017 – a helpful trend for SA exports and manufacturing and mining activity. Less helpful to the SA economy is that the oil price has also sustained a muted recovery, influenced no doubt by the same pick up in global growth.

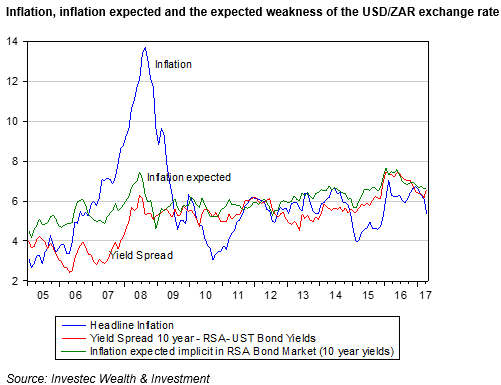

Further encouragement for the economy has come from a stronger rand: it has more or less maintained its US dollar value when compared to its emerging market (EM) peers. The US dollar exchange value of the rand has moreover remained consistently ahead of its values of a year ago, as is shown in figure 3.

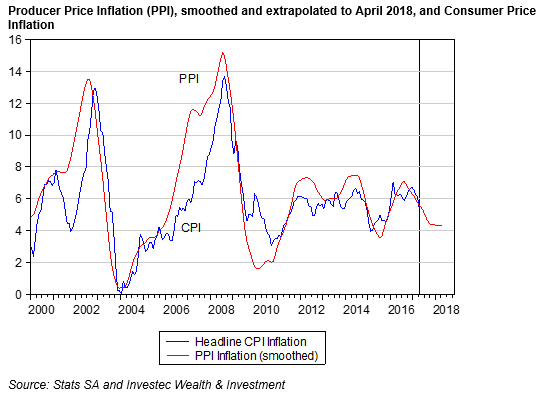

The stronger rand has helped to reverse the headline rate of inflation, which is now well down on its peak levels of mid-2016 and could easily fall further, as we show in figure 4, where currently favourable trends are extrapolated. Over the past quarter, the consumer price index has risen at less than a 3% annual rate.

The prospect of significantly lower short-term interest rates, which would be essential to any cyclical recovery, has therefore now greatly improved, given prospects of lower inflation. The demand for and supply of cash, a very useful coinciding business cycle indicator, has been growing ever more slowly in recent months and, when adjusted for inflation, has turned significantly negative. Somewhat encouraging therefore is that the cash cycle appears to have reached a cyclical trough (see figure 4). A reversal of the cash cycle is an essential requirement for any cyclical recovery.

Two other activity indicators, retail sales volumes and new vehicle sales, provide somewhat mixed signals about the state of the economy. Retail volumes, as can be seen in figure 5, have continued to increase, albeit at a slow rate, while new vehicles sold in SA have declined sharply since early 2016. However the latest vehicle sales trends as well as retail volumes suggest that the worst of these sales cycles may be behind the economy. The sales trend however remains very subdued and will need all the help it can get from lower interest rates over the next 12 months.

We combine two recent data releases, new vehicle sales and the cash in circulation in July 2017, to establish our Hard Number Index (HNI) of the immediate state of the SA economy. As we show in figure 7, the HNI of economic activity turned decidedly down in mid- 2016 but now appears to have levelled off. The HNI can be compared to the coinciding business cycle measured by the Reserve Bank as we do in Figure 7. Extrapolating this Reserve Bank business cycle indicator also indicates that the worst of the current business cycle may be behind us.

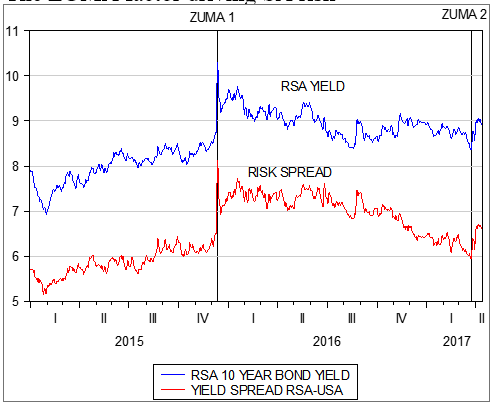

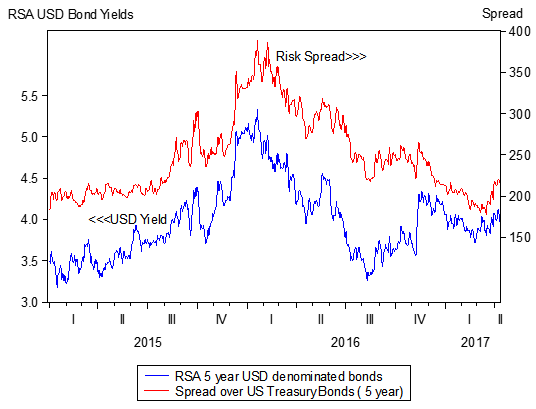

The economic news therefore is not all negative. However essential for an economic recovery is further rand stability and the lower inflation and interest rates that would accompany a stable rand. A combination of better global growth and so higher metal prices would help. So, presumably, would any confirmation of the end of the Zuma regime – a view seemingly already incorporated into the current strength of the rand as well as by the reduction in SA risk premiums. Both the strength of the rand, relative to other EM exchange rates, and the spread between RSA Yankee (US dollar) bond yields and US Treasuries indicate that the market expects the Zuma influence over economic policy to be over soon. For the sake of the rand, the economy and its prospects, one must hope the market is well informed. 25 August 2017