The short fall in government revenues of R56.8 billion reported in the Budget Review of 2023 came as no surprise to observers of the monthly tax returns. It represented a moderate miss in volatile circumstances – equivalent to 3.1% of the revenues expected in the February 2023 Budget of R1787.5 billion. A very large number and equivalent to 25% of GDP. This real tax burden (Taxes/GDP) is not expected to change over the next few years. Underestimated company tax, lower by R35.8b and net revenues from VAT down by R25.6b, accounted for much of the revenue shortfall. Weaker metal prices and massive investments in alternatives to Eskom power were largely responsible for both declines. Personal Income Tax grew as expected by 7% in line with some growth in real wages and salaries for those employed in the formal sector. The shortfall will be fully covered by raising additional loans of about R54b.

The higher ratio of national government expenditure to GDP, currently 29.1%, is estimated to decline to about 28% of GDP over the next three years. Still leaving scope for a positive Primary Balance of 0.3% of GDP this year and 1% next year. Raising revenues to exceed expenditures, net of borrowing expenses, is the first and necessary step to reducing the burden of National Debt to GDP-now about 74%, though predicted to decline to about 71% of GDP in three years. National government expenditure, is estimated to increase by an average 4.6% p.a. over the next three years, including servicing our debts, currently over 20% of all revenue that will cost the taxpayers about R400 billion this year. That would represent a decline after inflation.

The SA government is still practicing fiscal conservatism despite persistently slow growth that weighs so heavily on revenue. And inhibits expenditure. And raises persistent doubts about fiscal sustainability. That is the willingness of the government to avoid money creation, that is a heavy reliance on its central and private banks to fund its expenditure over the long run. Which raises the risks of more inflation and is already well reflected in high borrowing costs. Risks incidentally that have not trended higher in the run up to the Budget Review. Encouragingly the debt and currency markets reacted positively to the statement itself. The rand strengthened to improve the outlook for inflation and long bond yields declined by about 15 b.p.to help reduce debt service costs.

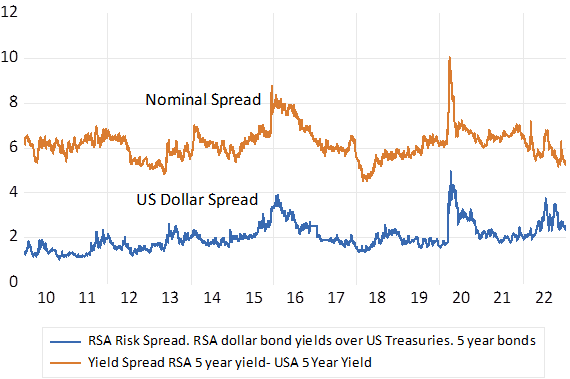

Source; Bloomberg

South Africa; Risk Spreads- Differences in borrowing costs. RSA-USA

Source; Bloomberg, Investec Wealth and Investment

In reading the Budget Review and listening to the Minister one is struck by how deeply dissatisfied the government is with its own performance. The statement is a catalogue of government failure.

To quote the statement

The case for reconfiguring government, as it is put, is vigorously argued by the government itself. It will however need its own genuine champions informed by events rather than a stale ideology. It will have quite simply to put the private sector and private sector incentives in control of much of the activities so badly performed by the SOE’s and government departments generally, that could be outsourced. It can be called private public partnerships rather than privatization, but the essential reforms required will be to incentivize operating managers on the bottom line and return on capital- as the private sector does – to thrive and survive. The upside is incalculable.

And as far as funding a reformed public sector, the place to start would be to dispose of key underperforming assets on the best possible terms. Selling assets or leasing them over the long term would be equivalent methods for raising capital and reducing government debt. The leases can be sold to funders (foreign and local) who would be very keen to provide finance on favourable terms, given credible operators. The Transnet iron-ore line from Sishen to Saldanha would be an obvious candidate for sale or lease. There will be many other such projects made much more valuable under different operating control. For the mines to lease and operate their essential gateways to the market would add many billions to their values and taxable incomes.