The PSG holding in Capitec had accounted for a very important 70% of the net asset value (NAV) or the sum of parts of PSG. Before the unbundling cautionary was issued in April 2020, the difference between the NAV and market value of PSG, the discount to NAV, had risen to well over 30%. The difference in NAV and market value of PSG was then approximately R20bn in absolute terms. The discount to NAV then narrowed to about 18% when the decision to proceed with the unbundling was confirmed.

Now with the unbundling complete, PSG again trades at a much wider discount of 40% or so to its much-reduced NAV.

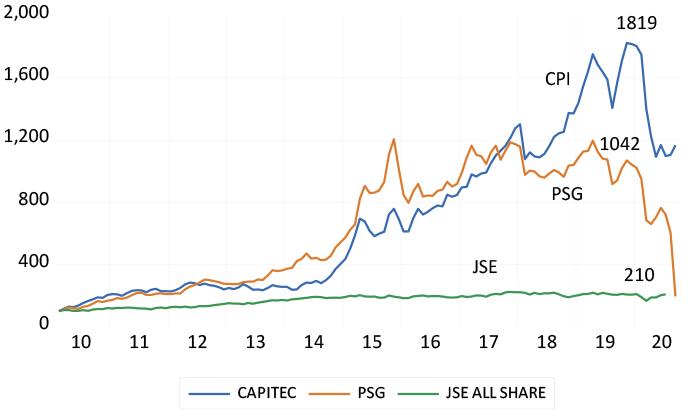

Capitec and PSG delivered well above market returns after 2010. By the end of 2019, the Capitec share price was up over 18 times compared to its 2010 value. By comparison, the PSG share price was then 10 times its 2010 value, and the JSE 2.1 times. The Capitec share price strongly outpaced that of PSG only after 2017.

The better the established assets of a holding company perform, as in the case of a Capitec held by PSG or a Tencent held by Naspers, the more valuable will be the holding company. Its NAV and market value will rise together but the gap between them may remain wide. Investors will do more than count the value of the listed and unlisted assets reported by the holding company. They will estimate the future cost of running the head office, including the cost of share options and other benefits provided to managers of the holding company. They will deduct any negative estimate of the present value of head office from its market value. They may attach a lower value to unlisted assets than that reported by the company and included in its NAV.

Investors will also attempt to value the potential pipeline of investments the holding company is expected to undertake. These investments may well be expected to earn less than their cost of capital, in other words, deliver lower returns than shareholders could expect from the wider market. These investments would therefore be expected to diminish the value of the company rather than add to it. They are thus expected to be worth less than the cash allocated to them.

To illustrate this point, assume a company is expected to invest R100 of its cash in a new venture (it may even borrow the cash to be invested or sell shares in its holdings to do so). But the prospects for the investments or acquisitions are not regarded as promising at all. Assume further that the investment programme is expected to realise a rate of return only half of that expected from the market place for similarly risky companies. In that case, an investment that costs R100 can only be worth half as much to its shareholders. Hence half of the cash allocated to the investment programme or R50 would have to be deducted from its current market value.

All that value that is expected to be lost in holding company activity will then be offset by a lower share price and market value for the holding company – low enough to provide competitive returns with the market. This leads to a market value for the company that is less than its NAV. This value loss, the difference between what the holding company is worth to its shareholders and what it would be worth if the company would be unwound, calls for action from the holding company of the sort taken by PSG. It calls for more disciplined allocations of shareholder capital and a much less ambitious investment programme. The company should rather shrink, through share buy backs and dividends, and unbundling its listed assets, rather than attempt to grow. It calls for unbundling and a lean head office and incentives for managers linked directly to adding value for shareholders by narrowing the absolute difference between NAV and market value. Management incentives, for that matter, should not be related to the performance of the shares in successful companies owned by the holding company, to which little or no management contribution is made.

On that score, a final point directed towards Naspers and its management: the gap between your NAV and market value runs into not billions, but trillions of rands. This gap represents an extremely negative judgment by investors. It reflects the likelihood of value-destroying capital allocations that are expected to continue on a gargantuan scale. It also reflects the cost of what is expected to remain an indulgent and expensive head office.