A path to faster growth in SA could be export led. There is no lack of global demands for valuable goods and services that could be delivered from SA with the right incentives to do so. The most obvious incentive would be a consistently favourable relationship between the revenues, realised producing goods and services at home for foreign customers and their costs of production. From an exporters perspective and from the perspective of a local producer competing with imports, the wider the gap between exchange rate movements and inflation rates, the better for growth in output and incomes with more exported less imported.

To encourage the demand for exports and discourage the supply of exports the exchange rate should weaken predictably by more than the difference between inflation in SA and its trading partners. The weaker the exchange rate movements compared to the differences in inflation rates, the better for competitive local production. But ideally the exchange would weaken at a modest rate, but also one that consistently exceeds a hopefully still modest rate of inflation. Indeed, a slow rate of currency depreciation is an essential ingredient for sustaining low rates of inflation. Yet still allowing enough of a predictable gap between exchange rate weakness and local inflation to make exports and replacing imports a consistent driver of faster growth.

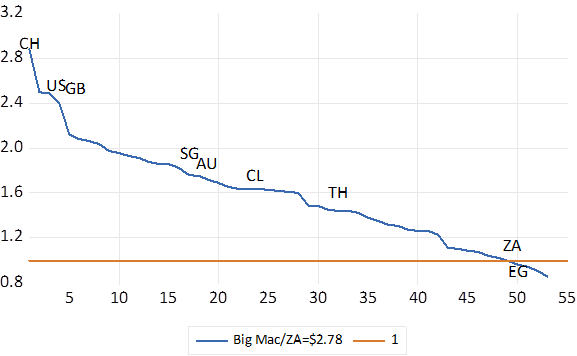

The South African rand ever since the economy opened to significant inflows and outflows of capital in 1995 has consistently had much more purchasing power at home than abroad. As any tourist local or foreign would attest. SA is among the very cheapest destinations. The 50th cheapest Big Mac cheeseburgers are to be found in SA. We pay about USD 2.78 for the privilege. Compared to an average $5.79 paid in the US (tip 20% – strongly recommended, excluded)

You would only pay marginally fewer dollars and cents for your Big Mac in Egypt, India Indonesia and Taiwan than in SA. Surely a boost to incoming tourism. The most expensive Big Macs are to be found in Switzerland, priced at over 2.8 times their USD cost in SA. Switzerland struggles to maintain the competitiveness of its jewellery and watch manufactures and Alpine holidays in the face of safety seeking capital flows that raise the cost of a Swiss franc and everything else in Switzerland. Perhaps a high-level problem to have when you can convince the wealthy of the world that their money is safe with you. According to the WSJ the average price of a margin enhancing and buzz inducing cocktail in the US is now $13.61. Equivalent to R225 rand. Which with luck and judgment your local speakeasy will charge you half as much- maybe R110.

Fig.1; The Price of a Big Mac around the world. A multiple of its dollar price (2.78) in South Africa

Source; Google and Investec Wealth and Investment

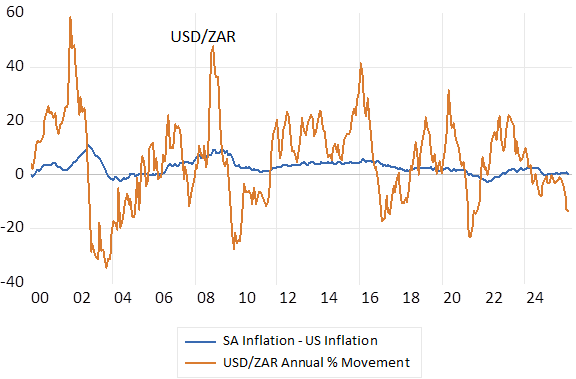

But this ratio between the foreign exchange value of a rand and its purchasing power equivalent has been a highly variable one. Since 2000 the rate of inflation in SA has averaged about 2.4% a year faster than in the US, with minimal volatility. The USD/ZAR exchange rate has weakened by an average 5.8% p.a. providing for a generally competitive exchange rate with the USD but a margin with very high volatility. Making the budget calculations of exporters and importers highly uncertain A highly variable real exchange rate is not good for sustainable business. We should hope for less volatility.

Fig.2; SA Vs US Inflation Differences, and USD/ZAR Exchange Rate Movements % p.a. Calculated monthly.

Source; Bloomberg, Fred, Investec wealth and Investment

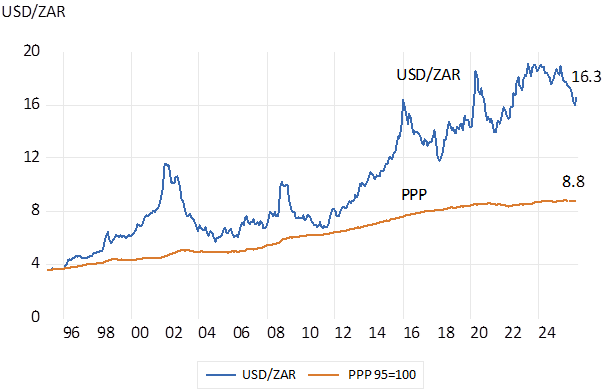

A purchasing power equivalent (PPP) exchange rate would fully compensate for differences in inflation rates between SA and the US. If the exchange rate (R3.6 in 1995) had simply compensated for difference in SA and US inflation since then, the USD would now trade for less than 9 rand – about 54% of its current market. Roughly equivalent to the double we pay in rands for the goods and services we consume abroad

Fig.3; The market and PPP equivalent USD/ZAR exchange rates

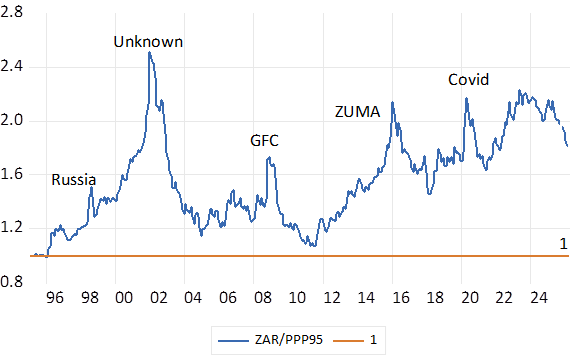

This ratio of the market value of the USD/ZAR to its PPP equivalent has however varied from a peak of 2.4 times in 2002, to a brief one-to-one relationship in 2010. A very good time to have travelled Whereafter under Zuma inspired threats to capital took the ration back over 2 in early 2016, a ratio that has remained similarly elevated and internationally competitive since.

Fig 4; The Real USD/ZAR exchange rate Market/PPP Ratios. (1995=1) Higher numbers indicate improved foreign competitiveness.

Source; Bloomberg, SA Reserve Bank and Investec Wealth & Investment

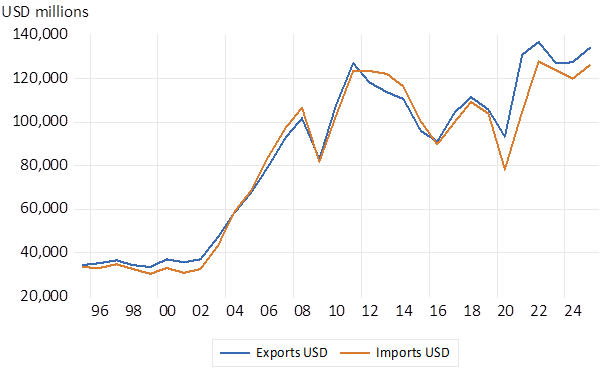

Yet despite the stimulus of a competitive exchange rate, export volumes and revenues in USD and have been largely stagnant since 2010. There was very strong growth in the years before. And imports have kept pace with exports. Clearly other well recognised forces have restrained economic growth generally as well as limiting the capacity to export and compete with imports.

Fig 5; Exports and Imports; USD values.

Source; SA Reserve Bank and Investec Wealth & Investment

But the case for export led growth remains compelling. It needs the right supply side encouragement. A more predictable exchange rate – both nominal and a competitive real exchange rate would be very helpful to the purpose. But very recent global events and its impact on the ZAR- a high beta emerging market exchange rate – have reminded us how unlikely is this prospect. And low inflation itself can be a mixed blessing for exporters if it means a stronger real exchange rate. South Africa should seriously consider the actions that would convince investors to support the economy with capital. And to learn to manage exchange rate instability and inflation without destabilising the real economy.