The Ramaphosa ascension has been very well received by the capital and currency markets. The political risk premium attached to SA-domiciled assets has declined sharply. The yield spread between RSA bonds denominated in US dollars that carry risks of default and US Treasury bonds narrowed sharply after November when it became more likely that the Zuma list would not be voted in at the ANC Congress in December. This sovereign risk spread – the extra yield investors receive on five year RSA debt to compensate for extra risk – declined from over 2% in November to about 1.4%. SA debt now trades as (low) investment grade.

The rate at which the rand is expected to depreciate has also declined sharply as long-term interest rates in SA have declined and US rates increased. These differences in yields, expressed in different currencies, is known as the carry and is also the percentage difference between the spot and forward rates of exchange maintained through arbitrage exercises in the money and currency markets. The cost of securing a US dollar for delivery in the future therefore increases by the per annum interest rate spread. This spread for five year debt denominated in rands was 6.7% in mid-November and has declined to current levels of about 4.9% a decline of about 1.8% (See figures 1 and 2 below).

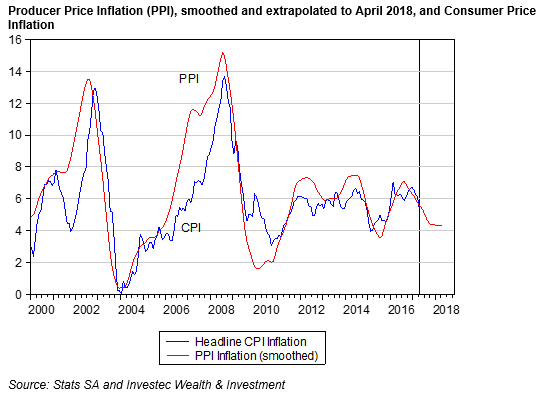

This decline in interest rates and less rand weakness expected portends lower SA inflation. Less inflation has also come to be expected by the capital market. These expectations are represented by the spread between the yields on vanilla bonds that carry the risk of inflation eroding the purchasing power of interest income, and the inflation linked variety that offer complete protection against higher inflation. As may be seen below, the bond market is pricing in about 60 basis points (0.6 percentage points) of less inflation to come in over the next five and 10 years.

These sovereign risks are also represented in the real yields on inflation-linked bonds issued in different currencies. The inflation link, especially on long-dated bonds, offers protection against the exchange rate weakness associated with more inflation. The real spread must therefore be attributed to factors other than the exchange rate risks the market is factoring in with nominal rates. Of interest is that this spread between long-dated RSA inflation-linked debt and US Treasury Inflation Protected Securities (TIPS) has narrowed sharply in recent months by more than 100 basis points (one percentage point). (See below)

It should also be recognised that real government bond rates in the US, while having increased marginally in recent months, remain well below normal. They indicate a continued global abundance of saving over capital expenditure and continued pressure on prospective real returns from all asset classes.

The better news about the future of SA has also been well reflected in the share market. Since December 2017, those listed companies with strong exposure to the SA economy have dramatically outperformed those companies that generate almost all of their revenues and earnings outside SA. The JSE All Share Index – with at least half the companies represented in the index highly dependent on offshore economies – has returned very little since 1 November. The total returns from Banks and Retailers since then by strong contrast have been over 30%. (See below)

The offshore businesses listed on the JSE are best described as SA political hedges rather than rand hedges. The rand/US dollar exchange rate reflects two forces: global and SA-specific forces drive the markets in the rand and rand denominated securities. Global economic forces can act to strengthen or weaken emerging market economies and their exchange rates against the US dollar. The rand is very much an emerging market currency and will move with emerging market exchange rates – with an import overlay of SA political risks. When the rand strengthens for SA reasons, as it has done recently , the SA hedges listed on the JSE (British American Tobacco, Richemont and Naspers, for example) are likely to lose value when expressed in rands. Their US dollar value may remain unchanged while their rand value falls with a stronger rand. The earnings of SA economy-exposed stocks benefit from a stronger rand whatever its provenance; hence their recent outperformance can be attributed to a stronger rand because of less SA risk priced into the markets and an improved outlook for the SA economy.

These SA economy plays could benefit further should the SA economy grow faster than expected. The additional confidence to spend that comes with a happier state of political affairs will help the economy along. The lower inflation rates that follow a stronger rand will also encourage the spending that SA-exposed companies can benefit from. Lower short-term interest rates would be an additional stimulus to the economy. Lower inflation and expectations of lower inflation should encourage the Reserve Bank to lower its key lending rates.

The money market however, while no longer expecting short-term interest rates to rise over the next 12 months, according to the forward rate agreements, does not (yet) expect short-term rates to decline. The case for lower interest rates is a very strong one, given the state of the domestic economy and lesser uncertainty attached to its political future. An austere 2018 Budget, with government revenues estimated to rise significantly faster than government expenditure, is a further reason to ease monetary policy. The SA economy plays might well continue to outperform the SA hedges were the Reserve Bank to focus on the risks to growth rather than the risks to the exchange rate and inflation. 5 March 2018