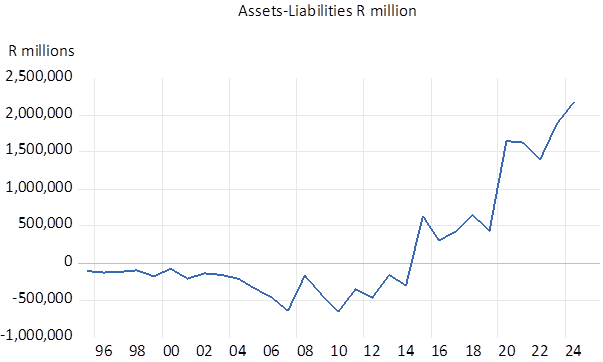

Since 2016 in ten years the annual growth in real GDP has averaged a miserable 0.69% p.a. and the growth in household disposable incomes has grown by an immiserating 0.46% p.a. average. By sharp contrast the increase in the wealth of South Africans has been very impressive. Net SA wealth held offshore was substantially negative before 2014, it amounted to over 2 trillion rand by 2024. The result of capital gains realised in portfolios rather than net inflows into AUM. Relieving forex controls has worked very well for SA balance sheets.

Fig 1; SA; Growth in Net Foreign Assets 96-2024. Annual Data

Source; SA Reserve Bank; Investec Wealth and Investment

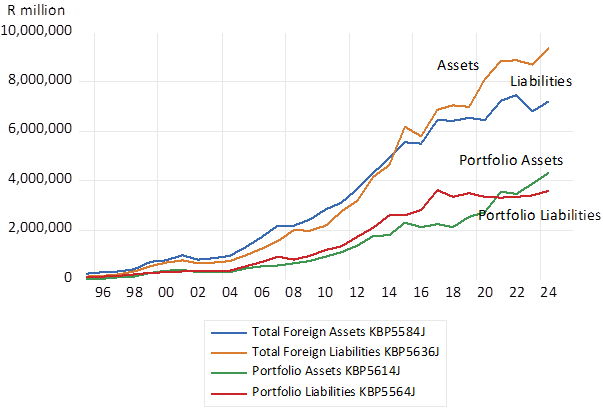

Fig 2; SA Foreign Assets and Liabilities. Market Value (R million) Annual Data.

Source; SA Reserve Bank; Investec Wealth and Investment

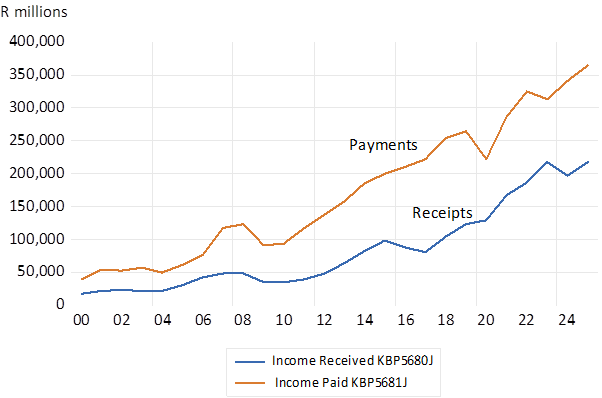

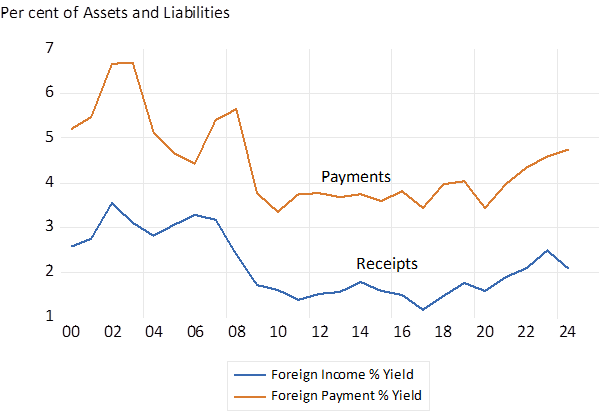

The income received from assets held abroad still lags well behind the payments of dividends and interest to offshore investors. An income gap that has remained a very wide one and a major contributor to the deficit on the current account of the balance of payments. South African issuers of debt or equity pay out at a much higher rate than we receive. Currently the yield on SA securities held abroad is over 5% p.a. compared to the 2% yield received.[1] Measured in rands that are expected to lose value over time.

Fig 3: Foreign receipts and income from SA assets and liabilities held offshore (R millions) Annual Data

Source; SA Reserve Bank; Investec Wealth and Investment

Fig.4 Foreign receipts and income from SA assets and liabilities held offshore. Yield per cent per annum. Annual Data

Source; SA Reserve Bank; Investec Wealth and Investment

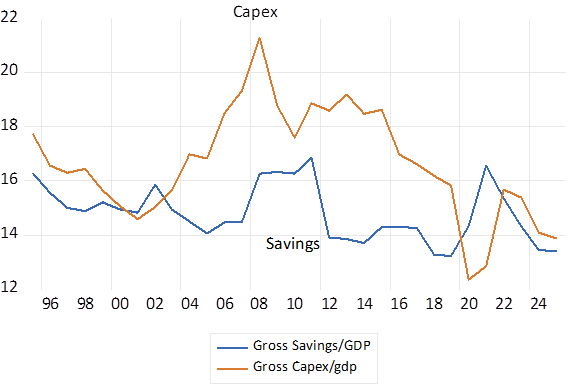

Better perhaps to be a lender with a strong balance sheet rather than a borrower. Yet capital inflows from abroad used to fund capex would be very welcome. Both the savings and capex rate in SA are unsatisfactorily low and a symptom and a cause of slow income growth. Slow growth in incomes and in the demand for additional goods and services discourages scaling up production and capex to do so. Faster growth would stimulate capex improve returns on capital invested and attract the foreign capital to fund that growth. It is striking that the when the economy grew much faster in the mid 2000’s the ratio of capex to GDP rose to 22%- it is now 14%- and the widening gap between Capex and Domestic Savings was closed, as was the deficit of the current account and the deteriorating balance of trade of the balance of payments, by larger net inflows of capital. Faster growth in spending widens the gap between exports and imports and the current account deficit (an unnecessary concern) But will only prove possible when funded by inflows of capital. The capital makes possible the current account deficit. Current account deficits and capital inflows are most helpful when growth is accelerating.

Fig 5; The Ratio of Capex and Gross Domestic Savings to GDP. Annual Data (1996-2025)

Source; SA Reserve Bank and Investec Wealth and Investment

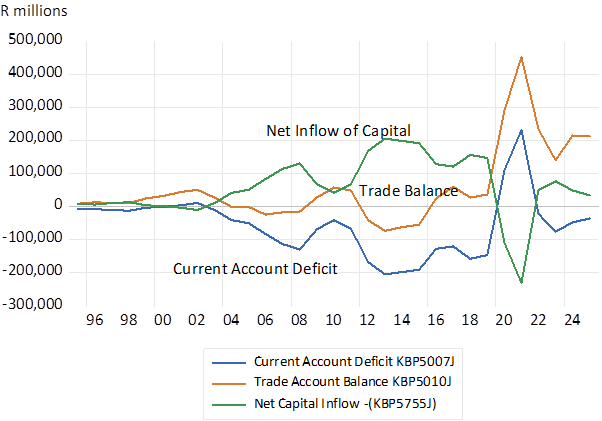

Fig 6; SA Balance of Payments Flows and Identities (96-2025) Annual data

Source; SA Reserve Bank and Investec Wealth and Investment

Faster growth must be accompanied by an increase in the demand for goods and services, imports add to the supply of goods and services. Demand= supply is the National Income Identity. Both sides matter. And faster growth becomes possible without inflation should the exchange value of the ZAR hold up. The prospects of faster growth are very likely to encourage capital inflows to fund any widening of the current account deficit and help to stabilise inflation as it did in the boom years 2002-2007. Faster growth with less inflation is very possible should the global capital market approve of the improved growth prospects and supply the capital that supports the currency.

It is surely apparent that shocks to the USD/ZAR and other exchange rates lead inflation in both directions. As it will again after the oil price shock. And policy determined interest rates are likely (misguidedly) to rise to further inhibit the growth in spending already under pressure from higher prices. Unfortunately, the case for investing in SA has deteriorated, as has the outlook for inflation.

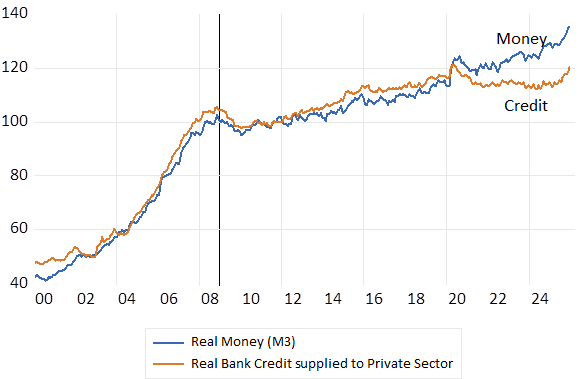

Faster growth over the past ten years has been an economic impossibility because the demand side of the economy has been so severely and consistently depressed by highly restrictive monetary policy. And faster growth- anything above 2% a year – will remain an impossibility, unless interest rate settings become more accommodating of higher levels of spending by households and firms accompanied by faster rates of growth in the money and credit supplies.

The growth in the real supply of bank credit since 2016 has averaged less than 0.5% p.a. and the money supply (M3) as grown at an average annual rate of 1.9% p.a. Much too slow for comfort. Unless these key monetary growth rates are allowed to accelerate faster growth will not happen, indeed cannot happen. And inflation as before will depend mostly on the exchange value of the ZAR. Which will be decided in the Strait of Hormuz, not in Church Street, Tswana. Without lower interest rates the supply of money and credit will continue to grow as slowly as it has over the past ten years and frustrate any growth potential supply side reforms may make. An increase in supply requires an increase in demand.

Fig.7: SA; The supply of money and bank credit- After inflation (2010=100)

Source; SA Reserve Bank; Investec Wealth and Investment

[1] The yield is calculated as Income as per the balance of payments accounts divided by the value of the assets or liabilities.