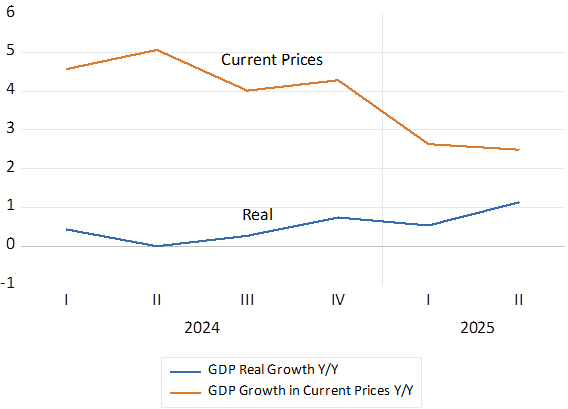

There is a welcome spring in the step of the SA economy. As revealed modestly by the latest National Income accounts released this week. The GDP in Q2 2025 was estimated as 0.8 per cent higher than in Q1. Slightly ahead of consensus and about one per cent up on the same quarter a year before. On a seasonally adjusted annualised basis equivalent to 3.5% p.a. growth, Which, if sustained would be most surprising, and politically consequential, given next year’s municipal elections.

Growth in SA GDP- (Y/Y) in Real and Current Prices. Quarterly Data.

Source; Stats SA and Investec Wealth and Investment

Is faster growth anything like this order sustainable? Supply side reforms work gradually. But to immediately improve the performance of the economy incomes there is a simple remedy easily implemented. That would be to significantly lower the cost and availability of credit for households and firms. The impact of small declines in these costs may in fact already be helping to advance household spending. The stronger growth in household spending to date was one of the GDP positives in Q2 and perhaps beyond.

The seemingly obvious case for lower interest rates, given their current levels relative to sharply declining inflation rates and given the very slow growth in the demand for and supply of bank credit by the private sector, is being strongly resisted by the Reserve Bank, in its efforts to permanently lower inflation to no more than 3% p.a.

Will lowering interest rates be more inflationary should spending and so growth rates improve, that is causing not only increases the demand for but also increases in the supply of goods and services? I would suggest that prices in SA including the CPI it will depend in the future, as inflation always does in South Africa, on the behaviour of the rand. And so on the cost of imports and the prices of exports that together play such an important role in our economy that is so open to trade. In Q2 2025 exports and imports together were equal to 60% of GDP – with exports 6% larger than imports in Q2. Clearly the exchange rate must matter a great deal for the path of prices in general, as it has so conspicuously influenced the direction of prices in SA recently.

The impact on prices facing consumers and firms along the supply chain encouraged by stronger demands would depend on the dollar and rand prices attached to these imports and exports, that is significantly on the exchange rate. Given a stable exchange rate, more growth with more goods and services imported and less exported becomes distinctly possible – without more inflation. And the feed back of faster growth to improved tax flows would also help improve the outlook for fiscal sustainability. The possibility of more growth with no more inflation, given rand stability, is surely a risk well worth taking. It is this vote gaining possibility the Minister of Finance is presumably pursuing with the Reserve Bank.

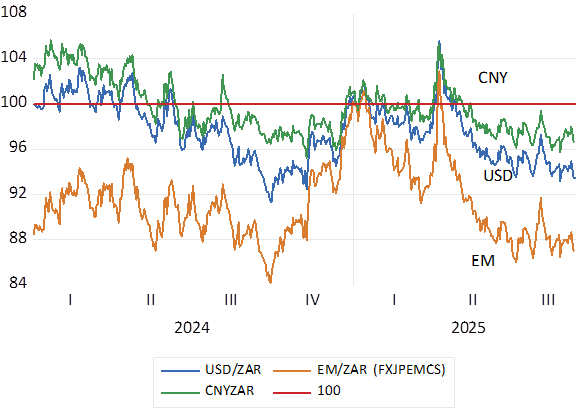

The surprising and most helpful of recent economic developments has been the strength of the ZAR. Strength against the weaker dollar but also against most of our important trading partners, including China.

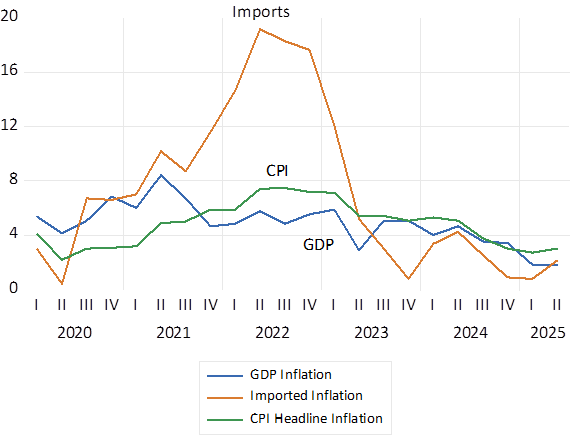

The post covid rand weakness forced import prices much higher to a peak year on year inflation rate of close to 20% in early 2022. The increases in prices charged have rapidly fallen away since with the recovery of the ZAR and have stabilised CPI inflation and the inflation of the prices of goods and services included in GDP- in the GDP deflator. So much so that GDP – measured in current prices rose by only 2.5% in Q2 – a mixed blessing because the much-watched ratio of Debt to GDP has accordingly risen. We are not inflating away our debt problem- rather the opposite – to the apparent approval of the bond market.

Inflation; Year on Year Changes in the Price Index for Imports, GDP and the CPI. Quarter End Data

Source; Stats SA and Investec Wealth and Investment

The ZAR Vs the USD, the EM Basket and the Chinese Yuan (January 2025=100) Daily Data 2025.

Source; Bloomberg and Investec Wealth and Investment

Yet the lower realised rates of inflation have helped to reduce inflation expected and the level of long-term interest rates. The yields on long dated RSA bonds – both rand and dollar dominated – have moved smoothly lower – as they have for other EM borrowers – despite the volatility in the US Treasury Bond market. This has made for highly satisfactory returns on investors in long dated EM, including RSA debt. Yet the SA economy plays on the JSE have had to struggle on, given the interest rate repressed, weakness of demand for their goods and services. A little TLC from the Reserve Bank would make a large difference to their valuations and all dependent on the SA economy. And to SA politics.

Bond Yields; RSA and USA. 5 year % p.a. Daily Data 2025

Source; Bloomberg and Investec Wealth and Investment