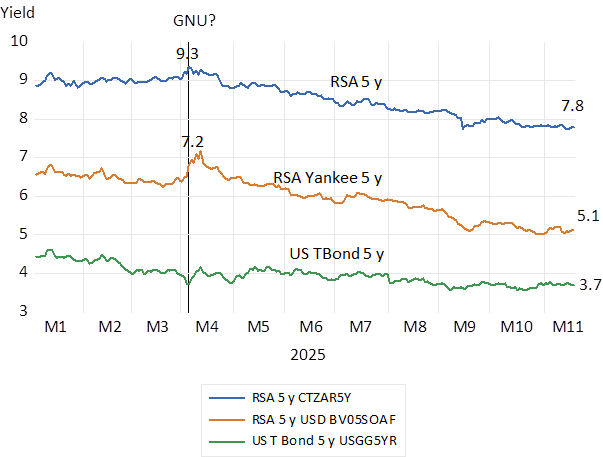

The update on the RSA Budget released on November 12th was well received in the Bond, Currency and Share markets. The yield on the benchmark 10 year RSA Bond gained 12 bp on the day to continue an extended bull run in RSA Bonds that began in April 2025. When doubts about the endurance of the government of national unity (GNU) were most pronounced. The yields on conventional RSA bonds of five year’s duration have fallen consistently from over 9% p.a. to 7.8%. since April. The republics cost of borrowing dollars has fallen even more significantly from 7.2% p.a. in April to the current 5.1% p.a. Representing a sovereign risk spread of 1.4% p.a. and less than half the risk spread of early April.

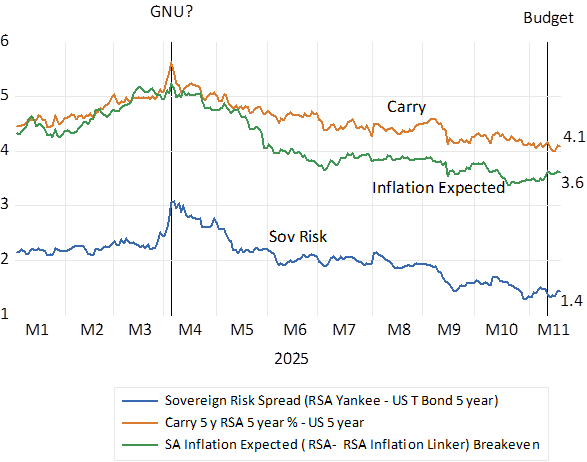

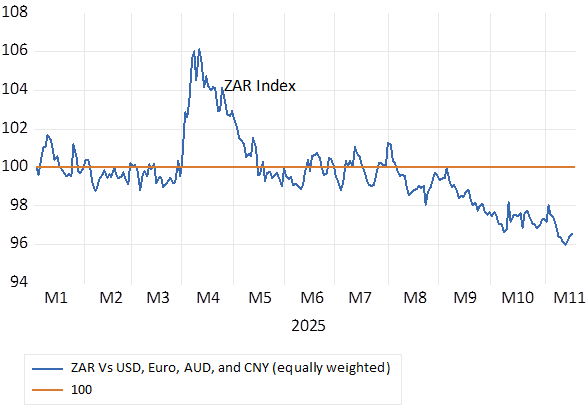

The difference between RSA and USA five-year yields – the carry or the cost of hedging dollars over the next five years, or equivalently the compound rate at which the ZAR is expected to weaken against the USD over the next five years, has fallen in line, from over 5% p.a. to the current 4.1%. The bond market is now factoring in an average rate of inflation of 3.6% p.a. over the next five years. Down impressively from over 5% p.a. inflation expected in April 2025. And the mighty ZAR since April has gained about 10% against an equally weighted Index of the USD, Euro, Aussie, and the Chinese Yuan since April 2025. The GNU has surely produced a kind of very welcome economic magic.

Long term interest rates in 2025. Daily Data.

Source; Bloomberg and Investec Wealth & Investment

Interest rate spreads in 2025 (Daily Data

Source; Bloomberg and Investec Wealth & Investment

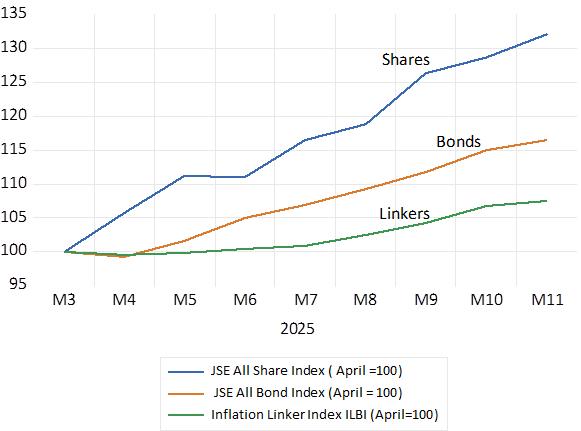

JSE Stocks and Bonds (April 2025=100)

Source; Bloomberg and Investec Wealth & Investment

The mighty rand in 2025 Vs USD, Euro, AUD and CNY. Equally weighted (2025=100) Daily Data

Source; Bloomberg and Investec Wealth & Investment

The Budget update confirmed that South Africa could reverse unfavourable fiscal trends and contain the growth in government spending and so avoid monetising the considerable national debt. And a further favourable force was that the target for inflation of 3% p.a. while accepted by the Treasury, was helpfully qualified by a one per cent band around 3% p.a. and accompanied by a phasing in period. Thereby improving the outlook for lower short-term interest rates and growth. The GNU cannot claim all the credit. The rise in precious metal prices plus the stability in industrial metal prices has helped to add to government revenues and improve the balance of trade – to improve further the fiscal and growth forecasts this year and the case for SA bonds the rand and the JSE.

Faster SA growth would be boosted by lower short- and long-term interest rates. There is growth enhancing scope for declines at both ends of the yield curve should the expected rate of inflation decline further. Which it could but only were the ZAR to continue to hold its own with its low inflation trading partners.

The supply side of the SA economy has been boosted by the strength of the ZAR in a low inflation world. The demand side of the economy has remained depressed by the high cost of bank and other credit. Lower inflation means more expensive credit and less demand for and supply of it from the banking system. Lower short-term interest rates would predictably stimulate spending by SA households and firms and raise growth rates.

Would such welcome trends mean more inflation? Not necessarily – inflation in the future would as in the past depend on the ongoing behaviour of the ZAR. Faster growth would mean increased demands for imported goods and foreign currency. But it would also simultaneously encourage inflows of foreign capital including to the bond market and discourage outflows of SA savings. The larger deficits on the current account of the balance of payments (extra demands for USD) would be matched by larger net inflows of foreign capital willing and to participate in faster SA growth (extra supplies of USD). If so, the rand could be well supported and the inflation rate contained. Faster growth with no more inflation is a virtuous cycle that we can only hope will be put to the test over the next few years. Reserve Bank permitting.

The immediate task for the Treasury is to fulfil its plans for containing government debt. But it should help taxpayers in two further essential ways. Firstly, to show belief in its own inflation targets and to borrow for shorter rather than longer periods and roll over short term debt for longer term debt as inflation and interest rates recede. The Treasury concern with so called roll over risk (a possible inability to borrow short to retire longer term debt) has been a very expensive fear not in fact shared by the rating agencies.

And another task for the Treasury, that it has long been aware of, and has egregiously failed to deal with, are the huge and unaffordable national liabilities of the disgraced Road Accident Fund. Claims on it must become realistic given taxpayers ability to pay and the responsibility for insuring against road accidents devolved, as is all other insurance, to the private sector.

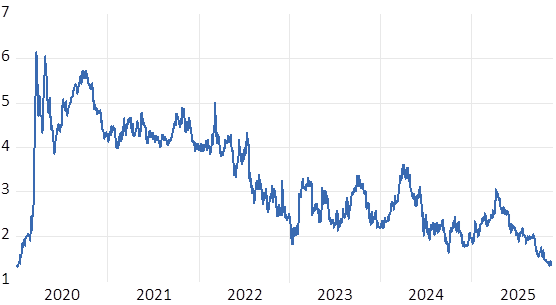

The slope of the RSA yield curve. Ten-year less one year RSA yields 2020-2025 (Daily Data)

Source; Bloomberg and Investec Wealth & Investment