June 3rd, 2025

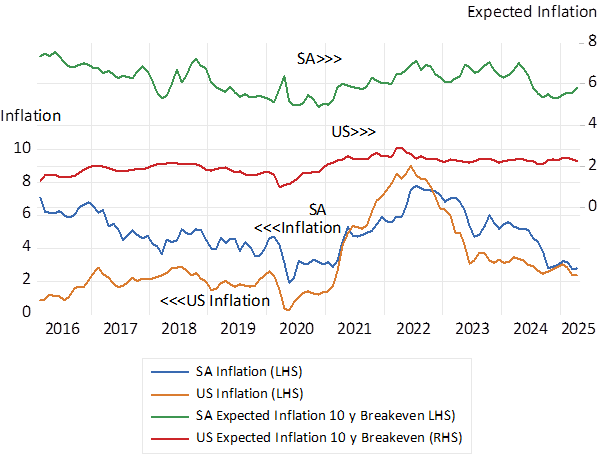

Inflation in SA has declined sharply from a 5% plus rate in early 2024 to 2.8% p.a. in April 2025 – for the usual supply and demand reasons. The demand for goods and services has been growing very slowly, and the supply side of the economy, given rand stability, recently even absolute ZAR strength, has brought moderate increases in the CPI.

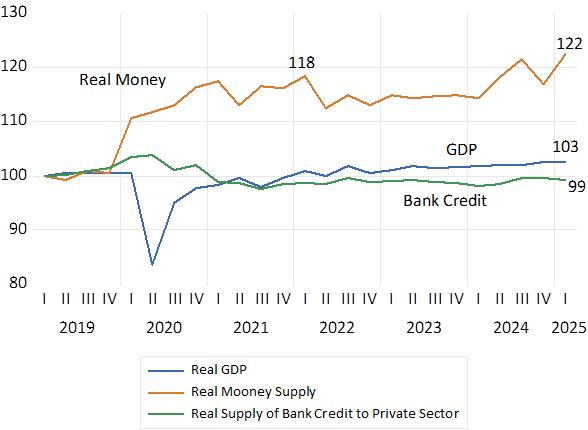

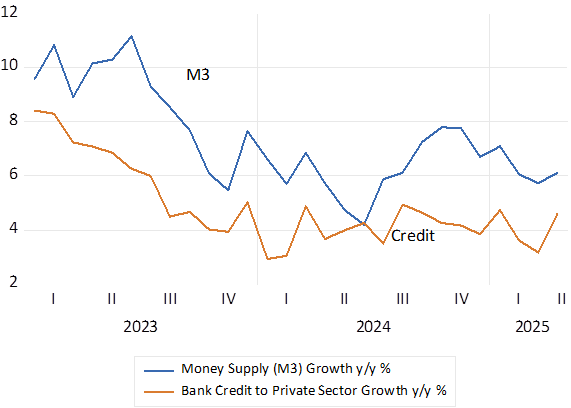

Bank lending to the private sector has been growing very slowly. Adjusted for prices, bank credit was still below pre-Covid levels and the real money supply after a spurt during Covid had grown by only 4.2% between 2021 and the first quarter of 2025. Recent growth rates in money and credit have trended lower. A financial state that can be described as severely repressive. Given the weakness of demand for goods and services it is unsurprising that real incomes and output (GDP) were but 3% higher in q1 2025 than they were in early 2019. When real demand grows as very slowly as it has in South Africa, real output could not have advanced at any faster rate than it has, meaning an expensive waste of a somewhat better growth opportunity.

Real Money Supply (M3) and in Bank Credit supplied to private sector. (2019=100) Monthly data to 2025 q1.

Growth in Money Supply and Bank Credit (January 2023-2025 April) Monthly % p.a.

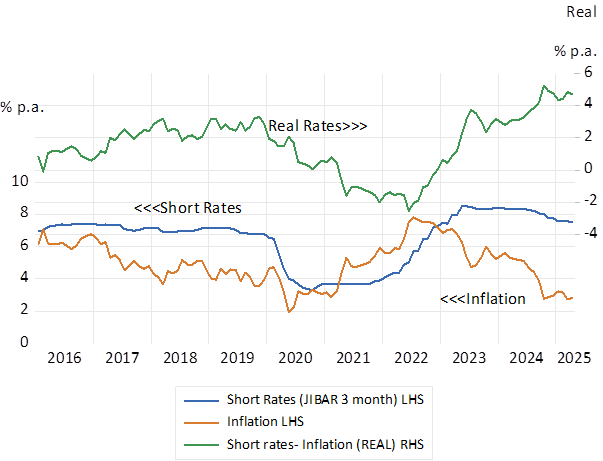

The lack of demand for and supply of credit and money is explained by short term interest rates set by the Reserve Bank. As inflation has come down the real cost of borrowing for overdrafts or mortgages has risen to very high, near record levels. Despite two 25 bp, highly delayed, reductions in the policy determined rate. The money market now predicts but a mere 25 bp further reduction in short rates over the next twelve months.

Without significantly lower interest rates to encourage the demand for bank credit and spending by households and firms, frustratingly poor GDP growth rates of less than 2% p.a. should be expected. And the prospect of too little rather than too much spending (relative to potential supplies of goods and services) is likely to continue to weigh heavily on the pricing power of domestic producers. The demand side of the economy is very unlikely to threaten higher prices for the foreseeable future without an unlikely change of mind set at the Reserve Bank.

Short term interest rates before and after inflation. 2016-April 2025. Monthly Data

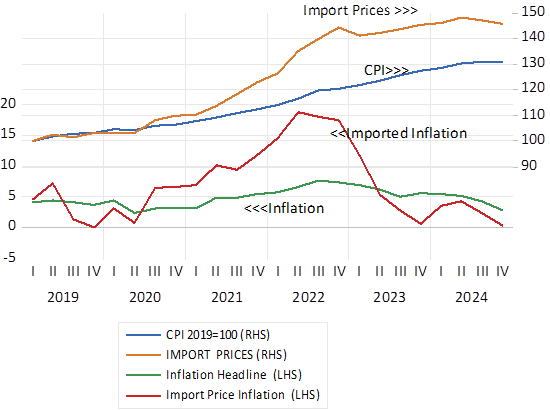

Yet the unpredictable supply side of the SA economy, perhaps accompanied by a sharp reduction in the exchange value of the ZAR could always drive prices higher. And judged by past performance the Reserve Bank would then then drive interest rates higher to further depress demand that would come under pressure from higher prices. Imports and Exports account for a combined 60% of GDP. Their translation into rand prices depends on the exchange rate. That recently has been strong against the USD, the Aussie dollar and the EM basket. The Import Price Index (with a large oil component) was falling in 2024.

Price Indexes; SA CPI and Import Price Deflator (2019=100) and annual % changes in the Indexes. Quarterly Data

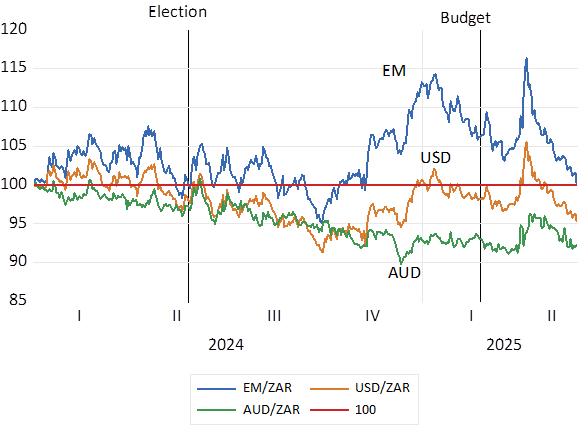

Slow growth aided and abetted by aggressive monetary policy while disinflationary, threatens growth and fiscal sustainability. It discourages domestic capex and capital inflows to fund them that might have improved longer term growth prospects. Slower growth expected frightens capital away and tends to weaken the rand- and raise inflation rates. Doubts that the GNU would survive the arguments over the 2025-26 Budget proposals led to some rand weakness. The agreements on the Budget reached finally in May 2025 have reinforced the GNU and added rand strength (see below) For the ZAR it is the supply side – the outlook for growth that matters most for the rand and in turn inflation.

Political developments and the ZAR in 2024-2025. Daily Data. Lower numbers indicate rand strength.

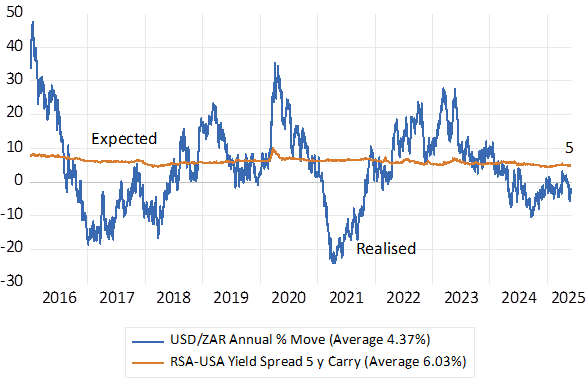

Long term interest rates, their levels and differences with US rates have still to register any marked change in sentiment about the outlook for SA growth or inflation. Forward exchange rates still expect the rand to weaken at about 5% p.a. over the next five years. (see below) And bond market yields- the difference between high vanilla bonds and elevated inflation protected RSA interest rates – indicate that inflation is still expected to average over 6% p.a. over the next ten years. Meaning expensive debt to add to fiscal strain.

Expected inflation and the cost of hedging the ZAR will not narrow, nor borrowing costs decline meaningfully, absent any significant improvement in the SA growth outlook. But nonetheless a welcome 3% p.a. inflation in SA could be sustained absent any exchange rate shocks initiated by politicians, local and foreign. Would setting a 3% inflation target mean more growth sensitive management of the demand side of the economy? Would it secure rand stability? Only possibly. It might however encourage the worst, anti-growth instincts of the Bank to prevail, especially when the supply side of the economy, the exchange rate, does not play ball.

The five-year RSA-USA carry and the realised annual move (% p.a) in the USD/ZAR (Daily Data 2016-2025 June)

SA and the USA; Actual inflation and Expected Inflation over the next 10 years (2016-2025)