25th September 2025.

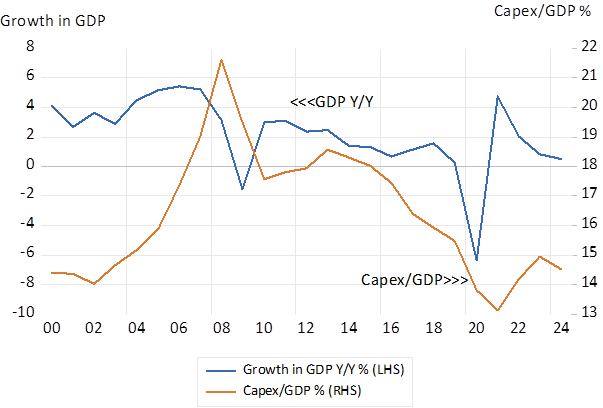

It is common cause that expenditure on capital goods in South Africa is not nearly high enough to sustain faster economic growth. Capex now runs at about 15% of GDP. It was 21% in 2008 after the economy had enjoyed a period of strong growth- averaging close to 5% p.a.

These broad trends – growth and capex rates rising and falling in the same direction – indicate that growth in household spending and incomes, especially in corporate incomes, leads and capex follows. We need faster growth to gain more capex and vice versa.

SA; Growth in GDP and the Capex to GDP Ratio 2000-2024. Annual Data

Source; SA Reserve Bank and Investec Wealth and Investment

Moreover, the most important source of domestic savings with which to fund capex (over 100% of all gross savings given government dissaving on a large scale and household saving largely offset by household borrowing) are made in SA by profitable businesses themselves. Savings in the form of cash retained by them rather than paid out in dividends or shares bought back. For society more capex more growth to come, rather than cash paid out is the preferred outcome.

Raise demand, raise incomes and profits and so business savings and increased capex will follow to sustain faster growth in spending. And should domestic savings be insufficient to fund the capex foreign savings attracted by the same growth in profits and improved returns can fill the gap. And fund the increase in imports that will accompany faster growth and add supplies of goods to help match increased demands for them.

The current account of the balance of payments goes into deficit that net capital inflows automatically match. And help to stabilise the exchange value of the ZAR. This is the virtuous cycle of growth that sustained the economy in the first decade of this century. Faster growth without more inflation.

The Current and Capital accounts of the Balance of Payments

Source; SA Reserve Bank and Investec Wealth and Investment

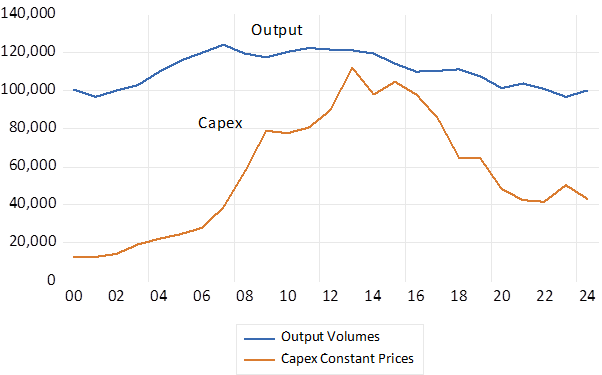

Alas much of the extra capital raised and invested in South Africa over the past 20 years was wasted on a large scale. Returns on capital invested by Eskom and Transnet have returned less than one per cent per annum on average. (See Business Day April 4th 2025) The huge capex programmes undertaken by Eskom in the early 2000’s have been accompanied by declines in the output of electricity –insufficient rather than excess capacity – with demand forced lower by growth destructive increases in the price of electricity.

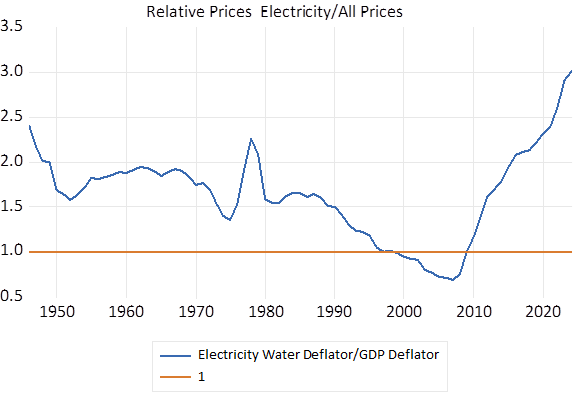

Capex on electricity and water- mostly electricity- Kusile and Medupi- in constant prices- grew by more than five times in real terms while the output of electricity and water in the same constant prices, peaked in 2008 and has been in decline ever since. As has capex. The price of electricity has increased three times faster than prices in general since 2000- to cover the inflated costs of construction and operations – up by over 14% p.a. on average. A growth destroying combination of wasted capital, bloated operating costs and much higher prices, that was a high additional tax on disposable incomes.

Electricity and Water; Output Volumes and Real Capex; 2015 Prices Annual Data. R millions

Source; SA Reserve Bank and Investec Wealth and Investment

The Price of Electricity and Water- Ratio to GDP Price Index (Deflators)

Source; SA Reserve Bank & Investec Wealth and Investment

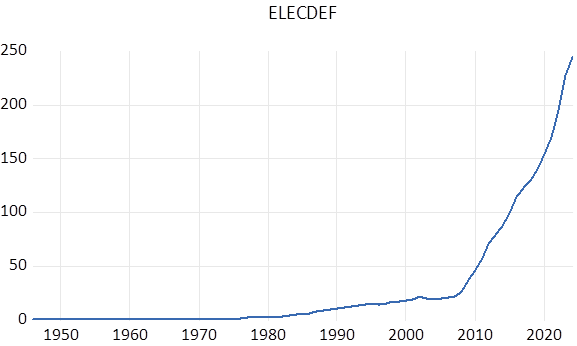

The Electricity and Water Price Index.

Source; SA Reserve Bank & Investec Wealth and Investment

The growth rates achieved between 2003 and 2007 now seem like an impossible dream. Dreams or nightmares to come will depend not on the volume of capex to come but more so on the quality of the capex undertaken. Quality as measured by realised returns on capital.

The waste of capital to date and the outcomes in the public sector more generally has not been accidental. Just follow the money to understand why it is what it is. The actions of the managers of South Africa’s public sector and their governing boards have not been driven by return on capital. As we learn they have seen their income earning potential derived from generous salaries and bonuses and other benefits of employment, armed guards perhaps, and including expensive travel allowances and payments for attending unnecessary meetings. Added to the huge temptation, often exercised, of perverting the very valuable contracts signed with service providers.

KPI’s that emphasise bottom lines or better still on returns on capital realised are essential to the purpose of improving the quality of the capital employed. It is indispensable for any business hoping to survive the threat of competition. Raising additional capital to be employed in SA, absent the discipline of required cost of capital beating returns, is very likely to be wasted.

It may be possible to introduce private sector style incentives to the public sector. But absent the forces of competition constraining the price setting power of public sector monopolies, it remains something of a dream. The alternative to economic stagnation is the firm recognition that only private ownership of capital and private production, imbued with the right incentives, can help improve the performance of the SA economy. Surely the evidence points overwhelmingly to this wake-up call.