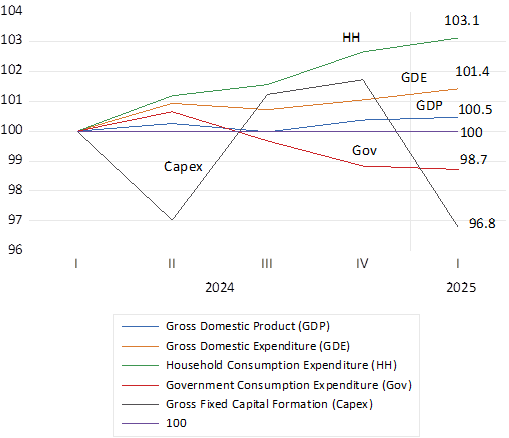

The real economy continues to make little progress, according to the latest National Income estimates for Q1 2025. Output (GDP) has stagnated, higher by a mere half of one per cent since Q1 2024. The expenditure side of the economy (GDE) has consistently fared as poorly, up by 1.5% since then helped to a small degree by a 3.1 per cent increase in household consumption. Government consumption expenditure, that excludes the welfare grants in cash that find their way into household spending, has also been a drag on the economy. Down by 1.3%, while a bigger drag on growth has been capital expenditure by firms and the government that is now 3.2% lower than it was in early 2024. A baleful reality that seems to resonate everywhere except at the Reserve Bank.

South Africa; National Income Flows Quarterly Data 2024-2025 (2024=100)

Source; SA Reserve Bank, Investec Wealth & Investment. (Quarterly seasonally adjusted data at constant prices)

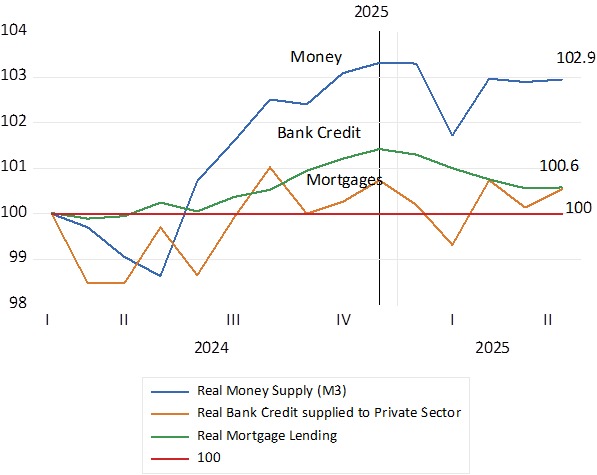

The lack of demand is easily explained by the money supply (bank deposits) and the credit supplied by the banking system. In 2025 the money supply and supplies of bank credit and mortgages, adjusted for inflation, have been in retreat and are barely above levels of early 2024. Clearly the lack of demand for money and credit can be explained by their high real costs.

Money Supply and Bank Credit Adjusted for Inflation; Monthly Data (2024=100)

Source; SA Reserve Bank, Investec Wealth & Investment.

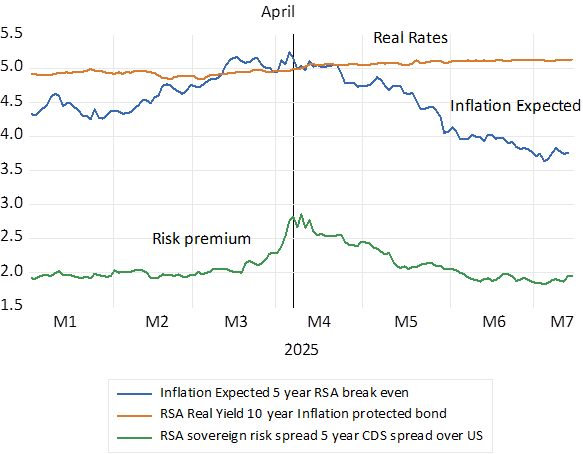

One notable improvement in financial conditions has been the decline in the inflation rate to below 3% p.a. Perhaps even more worthy of notice is the decline in longer term interest rates since April, when the anxieties about the Budget and the survival of the GNU were at their most intense. The 10, 5 and 1 year bond yields are off by 128, 89 and 25 basis points respectively. Truly big moves at the long end. Largely because expectations of inflation in SA have been revised significantly lower.

Inflation expectations are implicit in the differences in the yield on an inflation exposed bond and its inflation protected equivalent. These differences in nominal and real yields for five-year RSA’s have declined impressively from 5.14% p.a. in April 2025 to 3.75% this week. Perhaps because the Reserve Bank has committed itself to a 3% inflation target. But more likely because inflation itself has receded so sharply. Inflation leads and inflation expected follows – not the other way round – as the Reserve Bank likes to contend.

However, the SA specific risks explicit in bond yields, while 50 bp lower than they were in April are still highly elevated, now just under 2%. For five year RSA’s. And the fully inflation protected RSA 10 year bond yield remains above a risk infused real 5% p.a. This implies a very high real cost of capital for SA business that suffocates capex spending, especially when demand for the goods and services they produce remains so depressed – and is expected to remain so. And when short term borrowing costs are not expected to decline by more than 25 bp over the next 12 months.

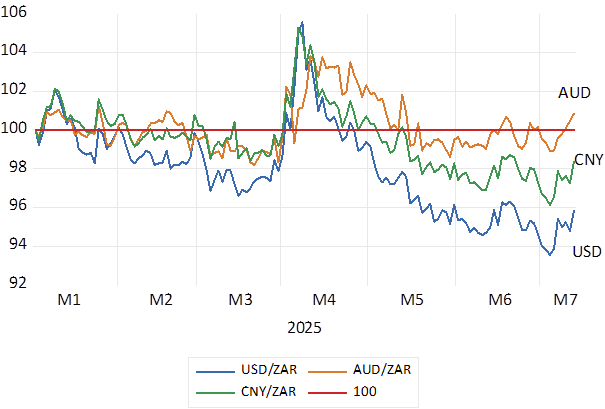

Inflation is down because demand for credit with which to buy is severely repressed. And because the rand has maintained its strength against most currencies. And in line with the bond market the ZAR has strengthened significantly since April 2025 for GNU related reasons. It is noticeable that the rand has weakened against the Chinese Yuan (our largest trading partner) at no more than an average about 1% p.a. rate since January 2021. One reason why Chinese motor cars are as cheap as they are. (despite Tariffs)

The ZAR Vs the USD, the Aussie and the Chines Yuan. (2025=100) Daily Data to 14th July 2025.

Source; Bloomberg, Investec Wealth & Investment

Real Rates, Inflation Expected and the RSA risk premium. Daily Data 2025

Source; Bloomberg, Investec Wealth & Investment

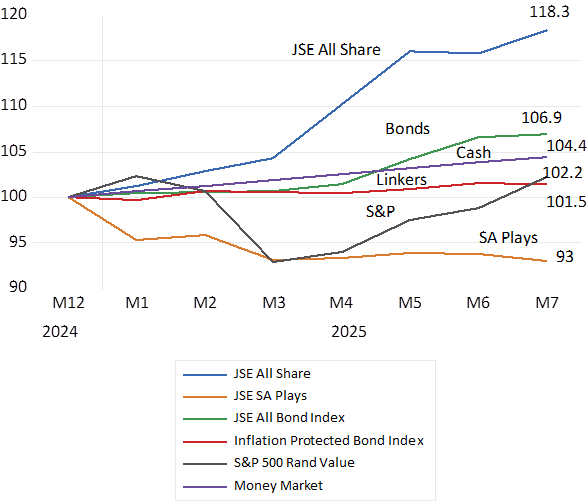

The stock market has nevertheless brought some welcome cheer. The JSE All Share Index has returned a whopping 18% this year. This run has everything to do with precious metals- platinum and gold in that order. Though the performance of the SA Economy Plays on the JSE reveals the dismal reality of a stagnant economy. The return on my constructed Index, market value weighted, of SA plays that includes the slow growth defying Clicks and Capitec, is down by seven per cent this year.

Growth can improve with governance and supply side reforms and less SA risk. Including reforms that can get more gold and other minerals legitimately out of the ground. Common cause surely. But faster growth needs the essential accompaniment of a more sympathetic monetary policy. That would hence reduce SA risk, sustain a stronger rand and lead to less inflation. Three per cent inflation is possible without squeezing further life and growth out of the demand side of the economy.

Total returns from the different SA Asset Classes in 2025. Month end data. (January 2025=100)

Source; Bloomberg, Investec Wealth & Investment