November 4th 2025

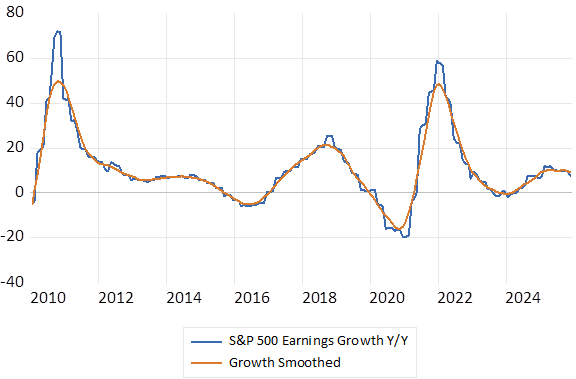

The US economy, judged by the flow of quarterly earnings reports from its leading companies is in very good shape. S&P 500 Index earnings have grown by about 8% over the past year. And the analysts are expecting further growth in earnings over the next twelve months- as much as an additional 14% by this time next year. Sales are growing and profit margins remain at highly elevated ratios. Fears of recession have proved greatly exaggerated.

And the prospect of further reductions in short term interest rates is still widely anticipated. Though several of the major employers, despite their impressive top and bottom lines have publicly revealed a deep reluctance to hire more workers. A wait and see approach to employing more workers and managers seems to be a widely adopted strategy by US business – understandably so. Waiting to see more clearly what the future of adopting AI means for their work forces seems an eminently sensible approach for all businesses everywhere, including South Africa to take.

And so the Fed – the US central bank – has a dilemma. And not only because the government shut- down has denied its policy makers the usual flow of updates on the state of the labour market. There may well be something much more fundamental at work that makes the conventional Fed play book much less useful.

The Fed has a dual mandate- it is instructed to control inflation and to maximise employment with its interest rate and asset purchase settings. And while the prices of goods and services are still presumably subject to the usual somewhat predictable supply and demand forces – the labour market may not be – given the hard to predict pace of adoption of AI. The relationship between the state of the economy and the state of hiring and firing may be changing in a fundamental way- at least for now. As may the link between wage rates, costs of production and prices charged may change. More (or less) demands for goods and services may not translate into coincident demands for workers. And so lowering interest rates to encourage demand for goods and services may be further good news for the revenue and profit lines of US business and lead to higher prices – without doing much to raise employment levels. If so, the case made now in the US for lowering interest rates is weaker.

That access to AI and AI empowered robotics will make workers of all kinds – those behind computers or assembly lines or down mine shafts more productive and safer is indisputable. As has been true of technological advances in the past made with the aid mostly of improved mechanics rather than computing power. Workers clearly produce more when complemented by more and better tools. But for additional profit margins, including covering the cost of the extra capital utilised, to translate into higher rewards for workers requires a relative shortage of workers. And competition for them. It is this competition for relatively scarce labour that has raised the rewards for work, enough for the average worker to consume more leisure – that is to work fewer hours.

Or the adoption of AI might lead to an excess supply of potential workers enough to drive down the rewards of the average, insufficiently skilled worker. While the same forces help promote the exceptional incomes of a highly skilled and productive few. For example, the million dollar a year AI engineers now eing paid ever more handsomely to move from one AI firm to another.

Among the beneficiaries of more profitable, perhaps less labour-intensive technology, would include the owners of the more profitable firms- the employers of the AI and the computing power. Including include among the owners the many members of retirement and pension funds with valuable shares in the AI success stories. Who may then be called upon to shield those unable to find decent jobs- to reduce inequality – as will be argued- with higher taxes.

One however can be optimistic about the impact of increased productivity on economic outcomes. Intense Competition to apply the technology and to scale up production for additional profit will mean more produced, lower prices and improved service. Lower prices and greater convenience greatly encouragers demand and demand for not only robots but also humans to supply a growing market. Think of Uber as an example. The convenience and price of E hailing has grown the market for a taxi service and the number of drivers. Another example might help. If cutting the lawn or your hair took a third of the time and a sixth of the current cost, we would surely trim more frequently and spend more time in the gym. The demand for AI advanced hair or lawn dressers who can share your woes, might well improve rather than decline. Hairdressing for boys does incidentally seem to be a growth story.

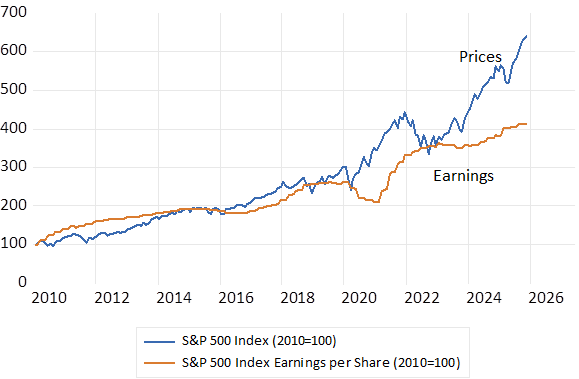

S&P 500 Index and Index Earnings per Share. (2010=100)

Source; Bloomberg and Investec Wealth & Investment

The S&P Earnings Cycle (2010 – October 2025)

Source; Bloomberg and Investec Wealth & Investment