Brian Kantor

January 13th 2026

These are exciting times for investors in South African assets. They are exciting for the usual reasons. Precious metal prices and the value of the producing mines have been on a tear. And precious metals are still very important for SA incomes, exports, the foreign exchange value of the rand, inflation and interest rates.

We have been here before – notably in the period between 2002 and 2007 when precious metal prices boomed, the rand strengthened and inflation and interest rates came down. And economic (GDP) growth accelerated in response. An episode that was disrupted by the global financial crisis. Though for a long period after 2012 precious metal prices in USD were in decline.

A reprise is very possible as interest rates recede further in response to lower inflation rates. And in response to a genuinely strong rand that the Reserve Bank may well conclude that is too strong for our good. And decide that the attractions of investing in rands should be discouraged to a degree with a lower carry in favour of the ZAR. And additionally buy dollars that would add to the cash reserves and the lending capacity of the banking system.

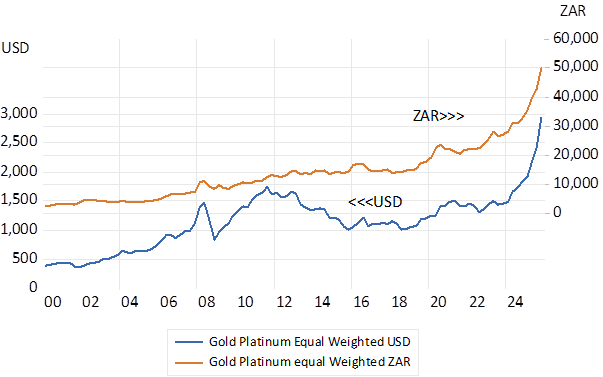

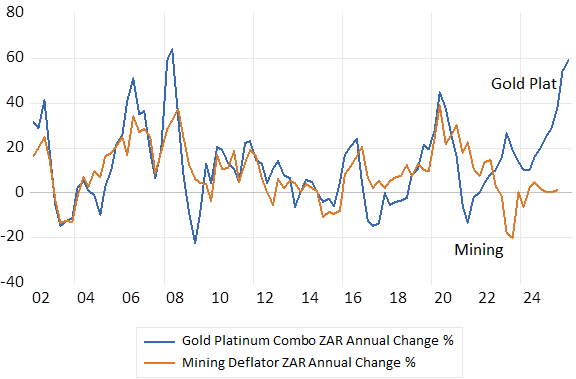

Note below the similarity in metal price trends in USD between 2002 and 2007 and lately. An equal mixture of the gold and platinum prices tells the story – which will be confirmed when the GDP and Balance of Payments statistics are updated later this month. Yet an updated mixture of platinum and gold tells the macro-story in an immediate way. The growth rates in this mixed basket mix are very similar to the growth in mining revenues generally as we show below.

The big metal price picture in USD and ZAR (2000-2026 Daily Data)

Source; Bloomberg and Investec Wealth and Investment

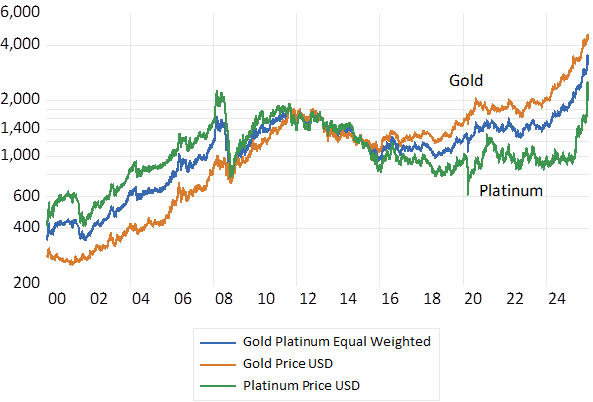

The big picture for gold and platinum in USD

Source; Bloomberg and Investec Wealth and Investment

Gold Platinum and the Mining Price Cycles

Source; Bloomberg and Investec Wealth and Investment

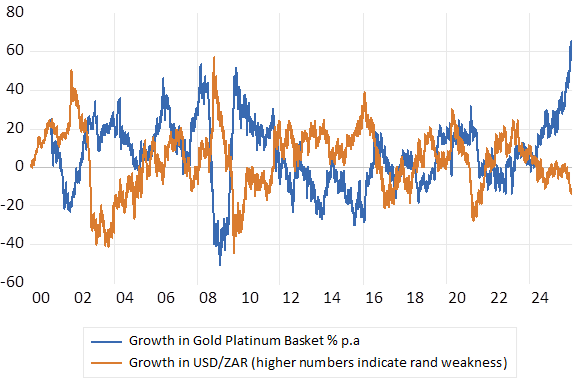

The impact of the surge in gold and platinum prices on the USD/ZAR exchange rate has been predictable – given past behaviour, as we also show below. The simple correlation between these two growth series is -0.54

Annual % move in the Gold-Platinum Basket and the USD/ZAR. Daily Data 2000-2026

Source; Bloomberg and Investec Wealth and Investment

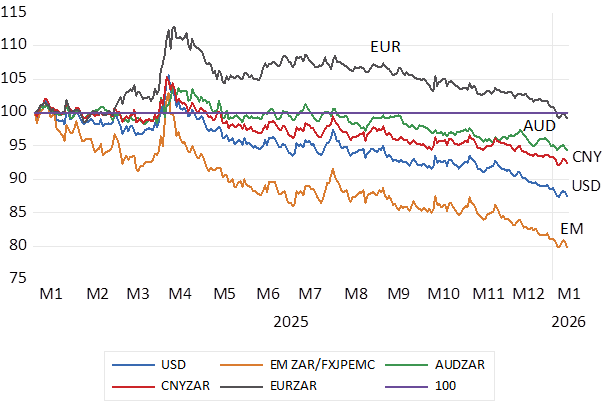

It is therefore not at all surprising that the ZAR continued to strengthen against all currencies and not only the weaker dollar. Including strength against the EM basket and the Aussie dollar, another commodity currency. (see below)

Exchange Rate Moves; Daily Data 2025-2026 (2025=100)

Source; Bloomberg and Investec Wealth and Investment

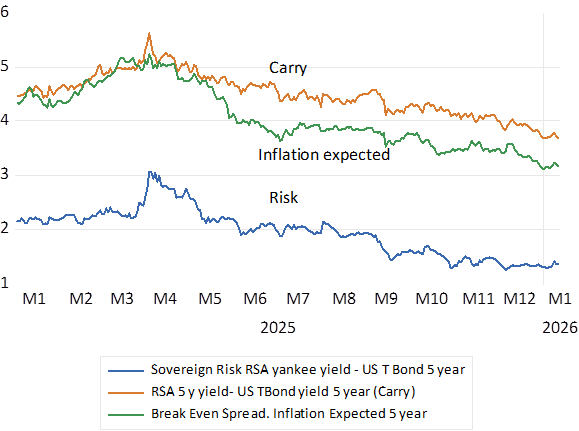

Furthermore, the bond market has responded favourably in a consistent way. Interest rates have receded as has the expected rate of inflation and the expected move in the USD/ZAR as represented by the five-year carry. (see below) The SA sovereign risk premium is now 1.34% p.a. down from the 3.1% registered in early April 2025. The prospect of faster growth improves the outlook for tax revenues and fiscal sustainability. Hence less to be borrowed at lower rates that also incorporate less inflation expected.

Risk Spreads 2025-2026. Daily Data

Source; Bloomberg and Investec Wealth and Investment

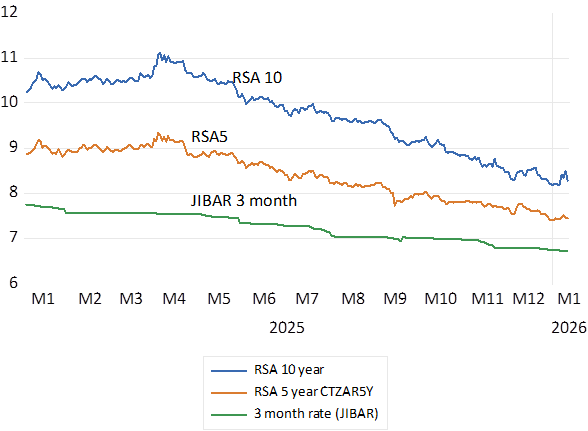

Long term RSA rates are lower by nearly 300 bp compared to early April and short rates are down by 150bp. The slope of the yield curve has flattened. There would be more to come – rand strength combined with the stimulus of lower interest rates, should the impetus from the precious meal prices be maintained. Carry on please Mr.Trump. SA is an unintended beneficiary of policy uncertainty.

SA Interest rate Trends. Daily Data; 2025-2026

Source; Bloomberg and Investec Wealth and Investment