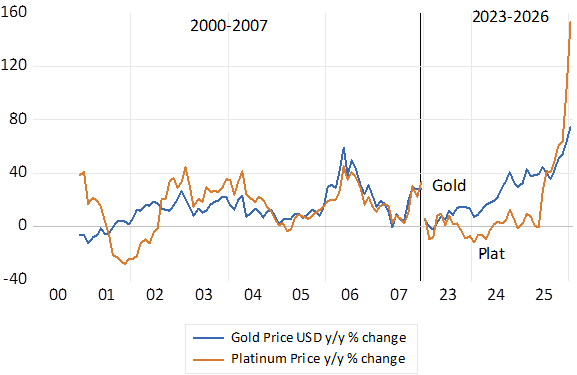

Every time the SA economy picks up momentum it is preceded by a surge in the USD prices of metals and minerals, our major exports where exports account for 30% of all output. We can hope with past performance in mind, that this time, led by much higher precious metal prices, will not prove an exception.

The favourable wind into the sails of the SA economy has continued to blow. That is the price of gold and platinum in USD have held up at what are very high levels, though off their highs of late January 2026. They are now still about 30% more expensive than they were on October 1st 2025.

The ZAR and RSA bonds continue to reflect the improving upside for the SA economy. The ZAR has added strength against all currencies and has been especially strong Vs the EM basket since October. The market in RSA bonds continues to reveal improved ratings – a trend that began in April 2025 with the survival of the GNU. The risk spread between a five-year RSA dollar denominated bond and a US Treasury of the same duration is now about 30 bp lower than the spread of early October and about 1.30%. p.a. Not quite investment grade credit but not far away from it.

These recent increases in the price of SA’s major exports rival those of the early 2000’s- the last time the economy sustained faster growth for an extended period. We can hope that these higher precious metal prices are sustained and that past performance- that was the highly stimulating of demand, credit and money supply responses to higher metal prices of the 2000’s – repeat themselves to some degree.

Growth in the USD Price of Gold and Platinum ; Comparing 2001-2007 and 2023-2026; Monthly Data

Source; Bloomberg and Investec Wealth & Investment.

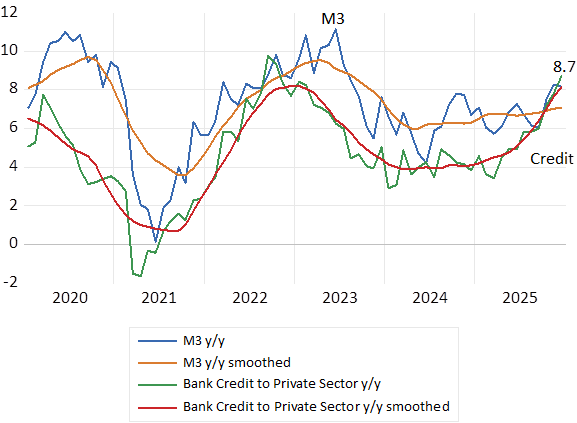

After 2002, in response to a persistently stronger gold and platinum prices, the growth in the supply of money and bank credit grew rapidly as the rand recovered, inflation receded and interest rates fell away. By late 2003 bank credit supplied to the private sector was growing at a very robust 20% p.a. rate and continue to increase by 20% p.a. until all the strong growth was so rudely interrupted by the Global Financial Crisis and one might add the debilitating Zuma presidency.

Inflation having fallen from 12% p.a. in 2002 to close to zero in 2004 in response to a strong recovery in the ZAR and higher interest rates then followed much faster growth in the supply of money and credit. GDP growth averaged about 4.5% p.a. between 2002-2007. It was a welcome combination of credit reinforced demand accompanied by additional imports that added to supply. And inflation was contained by a strong rand- supported by increased flows of foreign capital – willing to fund faster growth.

The responses of the SA economy to the higher metal prices of 2025 and a stronger ZAR are still somewhat muted. Short term interest rates have receded by 1.5% but remain high relative to much lower inflation. Yet to encourage spending, the money supply and credit cycles have clearly turned up. The supply of bank credit to the private sector is now up by over 8% compared to a year ago. And with consumer prices largely unchanged over the past six months, credit and money are now growing strongly in real terms.

The Bank Credit and Money Cycles 2022-2026. Monthly Data

Source; SA Reserve Bank, Investec Wealth & Investment

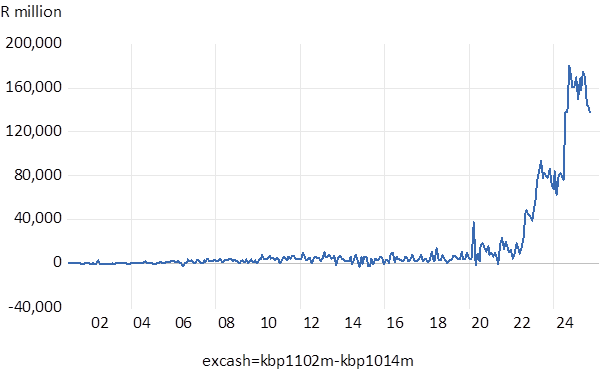

There is a new feature of the economy today that could add impetus to the growth in bank credit and the money supply. SA Banks now hold significant amounts of excess cash reserves, some R140 billion of them. The banks would surely like to convert into loans if only there were credit worthy demands for them. Which there would be if the economy could sustain faster growth. The ability of the Reserve Bank to control the demand for these cash reserves, paying interest on them, to prevent their too rapid conversion into bank lending, might be tested for the first time.

The SA Banks. Excess Cash Reserves

Source; SA Reserve Bank, Investec Wealth & Investment

Should the rand retain its strength allowing inflation to remain at about 3% p.a. the case for lower interest rates will be hard to resist. The negative impact of a strong rand on local manufacturers, is now very apparent, known in the economics literature as the Dutch Disease, might well lead to attempts by the Reserve Bank to inhibit rand strength with lower interest rates. Yet grist to the money supply mill.

Rand stability would contain inflation despite a pick-up in domestic spending. Indeed, should faster growth materialise, it would further improve the fiscal outlook and help further reduce the risk premium attached to capital invested in SA. And attract foreign capital to fund faster growth and further support the ZAR. It is not too much to hope for a sustained virtuous cycle of faster growth and less inflation stimulated as it has in the past, by metal prices sustained at high levels? May the onshore favourable winds continue to blow.