A Brave New Budget World Beckons

The Minister of Finance and his National Treasury have had a rude awakening. The Treasury set the National Budget and Parliament fell obediently in line to rubber stamp. The Treasury decided how much the government would spend, collect in taxes and how much and how the RSA would have to borrow to make up the difference. Until this year, when Parliament decided the final shape of the Budget. As it will do in any future of government by coalition -as the Minister of Finance, Enoch Godongwana, has clearly acknowledged.

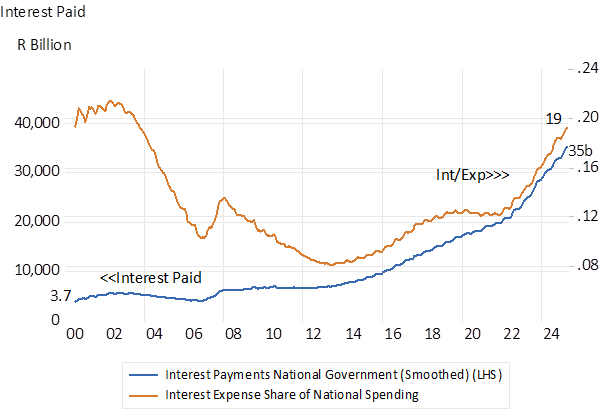

The financial legacy left by the once all powerful Treasury is an un-comfortable one- The Treasury has bequeathed a mountain of close to 6 trillion rand of debt and a huge interest bill now close to R40 billion a year. Equivalent to a suffocating 20% of all national government spending. This interest to spend ratio had fallen to 8% by 2013 but has more than doubled since then.

Interest paid and the Ratio of Interest Paid to all National Spending.

Source; SA Reserve Bank and Investec Wealth & investment

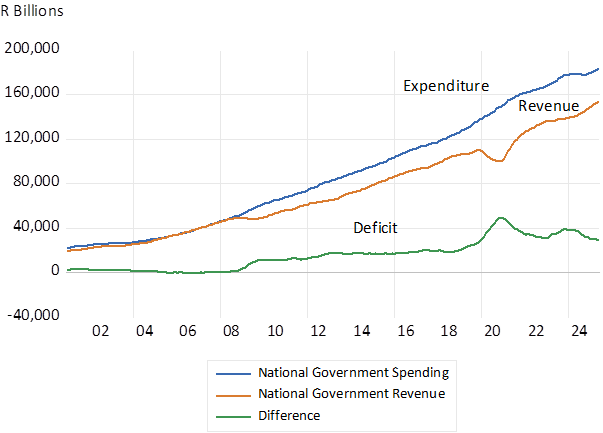

After largely balanced budgets between 2000 and 2008, it went gradually and consistently wrong after the recession of 2009 – linked to the Global Financial Crisis. Tax revenues fell away while government spending remained on its nominal growth path of over 8% p.a. The deficit jaws have not closed since then and widened further during the Covid lockdowns of 2020-2021. Between 2009 and mid 2025 national government expenditure has grown by an average 8.3% p.a. (equivalent to an after inflation growth rate of about 2.8% p.a.) yet more than the slow growing economy could fund. The growth in tax revenues lagged behind growing by an average 7.2% p.a. over this extended period. And so between 2015 and 2025 national debt grew by a debilitating 15.6% a year on average. Smallish Budget deficits became highly leveraged.

The Budget Arithmetic 2000-2025. Monthly data (smoothed)

Source; SA Reserve Bank and Investec Wealth & investment

RSA National Debt and Growth in Debt; 2000-2025

Source; SA Reserve Bank and Investec Wealth & investment

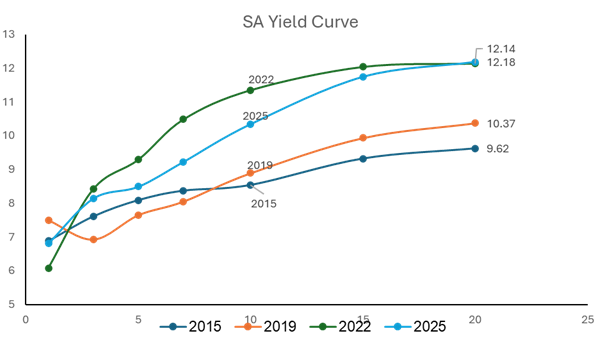

But there was something more than budget deficits that have increased the interest cost of funding the growing debt. The average time to maturity of newly issued national debt was allowed to increase. This significantly increased the cost of funding the national debt. Longer term rates of interest on RSA debt are consistently higher than on shorter term debt. An RSA 20 year bond now offers 12.18% p.a. compared to less than 7% paid on a 3-month Treasury Bill. Between 2010 and 2025 the difference in yield on a 10 RSA bond and a 3-month Treasury Bill has averaged over 2% a year while the difference in yield between a 10 and 5 year bond averaged over 1% p.a. Yet between 2010 and 2019 the time to maturity of the average RSA bond in issue increased consistently from 120 to 190 months. It has since declined to about 140 months. Which is a very large number by international standards.

The RSA Bond Yield Curve. 2015 – 2025. Time to maturity on X axis

Source; Bloomberg and Investec Wealth & Investment

The reason for extending the maturity structure of RSA debt was to avoid roll over risk. That is the apparent danger of having to repay debt, issuing new debt, at a time when the when the market might be highly unsympathetic. But SA debt of all durations is constantly being rolled over – given the amount of debt in issue and maturing regularly. Avoiding roll over risk was a very bad and expensive idea.

Should the market be temporarily closed the Reserve Bank can always be called upon in an emergency to provide cash for the government. It is one of the great advantage of being able to issue debt in your own currency, the quantity of which you control. Unlike foreign debt that you can default upon. The size of the market in rand denominated RSA debt is a large strategic advantage for SA that has been frittered away by paying up unnecessarily for very long-term money.

The risk that SA may be forced later or sooner to monetise its debt to inflate away its debt burden is the reason why RSA long term interest rates are as high as they remain. These high yields compensate lenders for more inflation expected and an accompanying weaker exchange rate. That SA prefers to issue long dated debt at a high fixed rate gives a poor signal about an official belief in the sustainability of fiscal policy and the prospect that inflation may fall rather than rise. As it has done, making previous long-term borrowing at high nominal rates ever more expensive for the tax payer, whose incomes are now rising at a slower rate.

The task for any successful coalition led Budget is to ensure that SA lives within its means. To balance the books by limiting much wasteful spending with authoritative expenditure reviews that have been woefully lacking. And by walking the lower inflation walk – by borrowing significantly more at the short end – rolling over long term debt for shorter varieties. Accepting the risks that inflation could drive borrowing costs higher. A prospect that would help discourage inflation and government spending.