A great business is one that has created enormous wealth for its founding owners and for those who bought and held. Graduating from a start up to a company valued in billions, even trillions of dollars, will bake in two essential ingredients. Firstly, excellent returns on the capital invested initially and subsequently. Returns (true profits) that exceed the opportunity cost of the owners capital invested.

But for true financial success a cost of capital beating return on capital will not be enough to add value for its owners. It must be accompanied by growth in the sales and operating profits of any start-up. The excellent cash returns will be retained and re-invested in the enterprise to fund its growth. It is a combination of consistently profitable operations plus the willingness the opportunity to grow the business organically, or by acquisitions, that opens the path to greatness.

Attempting growth however is always risky and not always worth attempting. The hard-earned savings of the business – cash retained not paid out – can easily be wasted. Not all profitable businesses will have sensible opportunities to grow. Think of a great highly profitable restaurant with an outstanding owner manager chef. There is only one such chef and the opportunity to add further branches and hire expensive additional chefs may not make good sense.

The owner might well be better off not scaling up the business. Continuing to pay out the considerable, perhaps highly predictable profits to herself and partners and be invested in a well-diversified portfolio. And acquire wealth that is capable of withstanding unpredictable shocks to the dining out or indeed any other established business.

But the business without ambition will be valued by potential investors accordingly. Valued essentially as you would an annuity that provided largely guaranteed income – discounted heavily by the risk adjusted cost of capital reflected in the market for fixed interest income.

It takes growth, or more precisely the expectation of profitable growth, that will encourage investors to pay up for a share – that is to value a business as worth much more than its current profits. It should be appreciated that for any closely watched business it is not the expected growth that provides exceptional returns for shareholders. The expected but uncertain growth prospects will be recognised and valued accordingly and be well reflected in the share price. It is the profitable or less profitable growth that surprises investors, in both directions, that leads shareholder returns.

South African economy facing businesses- retailers and banks for example – often deliver highly respectable cost of capital beating returns on the capital invested. But their valuations are heavily deflated by the absence of organic growth opportunities. The economy holds them back and is widely expected to continue to do so.

For an extraordinary demonstration of the value to shareholders of a combination of high returns on capital combined with unexpectedly strong growth in revenues, operating profits and in market value we can look to the performance of the Magnificent Seven (MAG7) companies listed in New York. Nvidia (NVDA) Apple (AAPL) Amazon (AMZN) ( Meta) Alphabet (Google) Tesla (TSLA) and Microsoft (MSFT) They demonstrate the value to their owners of an economic transformation under way and of their making. The future of which is unknown as is the future value of these companies in the vanguard of change. But so far so very good.

The market value of the Mag7 grew by 3.5 times or by about 12 trillion dollars between January 2020 and June 2025. The market value of chipmaker NVDA is up 24 times, the next best performer TSLA is up nearly ten times with the market value of the others up between two and four times their market values of five years ago.

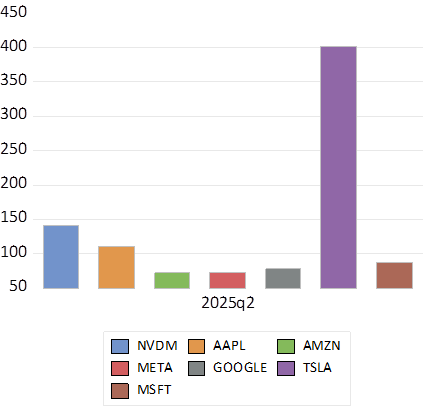

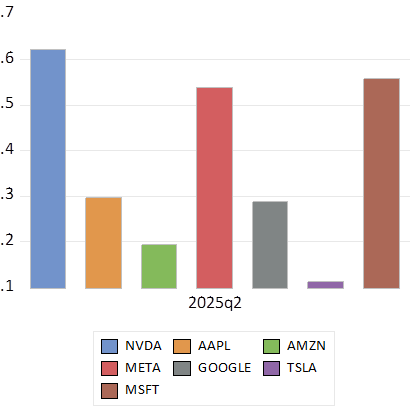

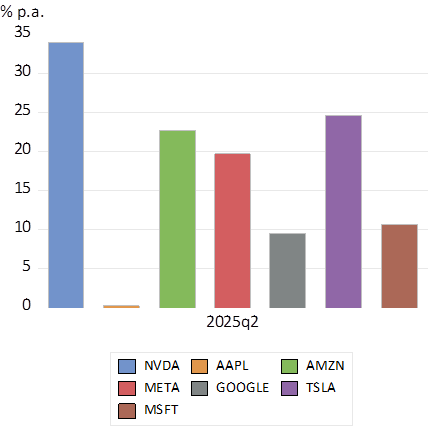

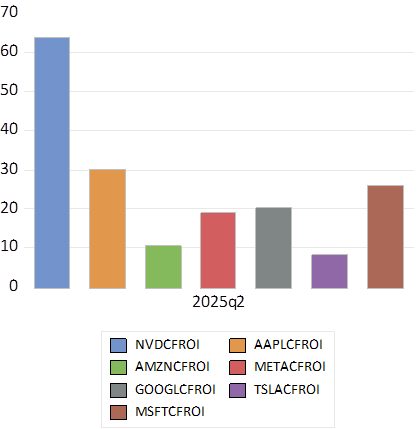

They are all generously valued, the ratio of market value to operating cash flows varying between the 400 multiple attached to TSLA and the 50 plus multiples attached to the others. Their sales and operating cash profits have been growing strongly and the operating profit margins (Sales/Operating Profits) are impressively high ranging from over 60% for NVDA and over 50% for MSFT and Meta. The under performers on this metric are AMZN and TSLA. Return on Capital invested (CFROI) is well above cost of capital except for TSLA and AMZN. It is over 60% p.a. for NVDA – clearly the outstanding performer in the group by all accounts. Its growth in capex is very strong but very well covered by operating cash flows and revenues.

Market Rating – Market Value to Cash Operating Profit Ratios (June 2025)

Source; Bloomberg and Investec Wealth & Investment

Operating Profits to Sales Ratios (June 2025)

Source; Bloomberg and Investec Wealth & Investment

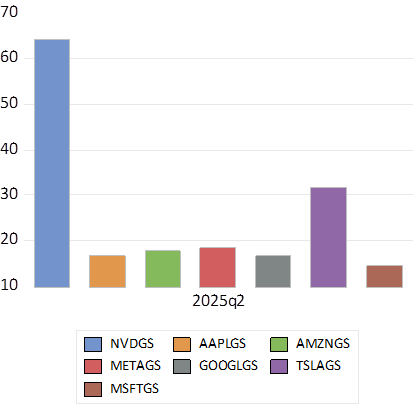

Annual Average Growth In Capital Expenditures (2020-2025)

Source; Holt and Investec Wealth & Investment

Growth In Revenues; 5 year Compound Average 2020-2025

Source; Holt and Investec Wealth & Investment

Cash Flow Return on Investment (CFROI) 2025

Source; Holt and Investec Wealth & Investment

A further very important feature the Mag7 is their huge volume of R&D. They are estimated to have spent $264 billion on R&D in 2024, even more than the $253b of capex undertaken that year. The Mag7 R&D spend is larger than that of the US health care sector. Mag7 capex is also well ahead of the capex of the combined Energy, Industrial and materials sector- some 220b in 2024. The R&D spend is not usually capitalised and is written off as an operating expense. This flow of spending is clearly a very large bet on the future structure of the economy. It represents competition for a share of the future economy in a most intense way. The financial success of the Mag7 has made such bets on the future possible. But they are very large bets indeed.

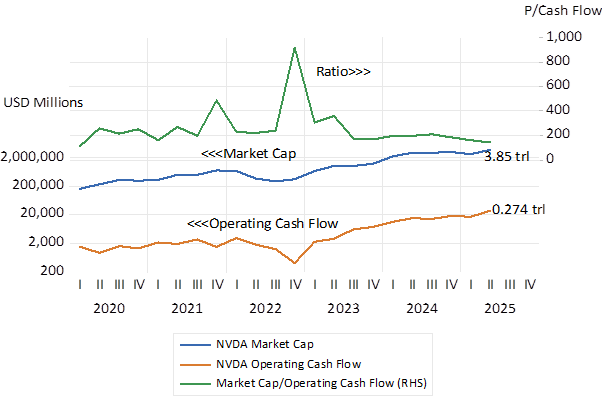

The extraordinary performance of NVDA is summarized below. The rise in its share price and market value has been matched by the growth in operating cash flow. It was expensive five years ago – and it is as expensive now- but much more valuable. Its growth in capex is very strong but very well covered by operating cash flows. A less risky exposure than of some of the other Mag7’s well reflected in its outperformance on the share market.

NVDA; Summary Performance Measures (2020-2025)

Source; Bloomberg and Investec Wealth and Investment

The difficulty for the investor in NVDA and the other Mag7’s is how do we value them with any confidence in our calculations of present value. Their current values depend so heavily on future performance that is impossible to predict with any degree of certainty. Though they are not lacking in past performance. Can performance be maintained or better exceeded to the further satisfaction of investors? Can it meet their expectations of revenue growth and justify the risky exposure to capex and R&D? We will have to wait and see.