The wider the market the less monopoly power any seller can have over it. If households choose, as they will, between all of the many goods or services households offered them, there can be no monopoly power. No one seller can command more than a very small share of the household budget that can easily be reallocated in response to higher prices or inferior service or changes in tastes and fashions. And households account for more than 60% of all final expenditure in SA.

Intense competition for their spend comes not only in the form of price settings. But is also revealed by the ability of suppliers to meet demands anywhere at the prices set with supply chain management- another key area in which suppliers compete. As important, as a source of competition for the household spend, will come through innovations in the form of new products or services introduced to the marketplace.

The all-important competition for revenues and profits is reflected in the updated menus presented to households and individuals. The new offers are disruptive of established interests in the status quo ante. Part of a dynamic evolutionary process that is good for consumers and tough on producers who are given no guarantees of consumer loyalty.

The great majority of business organisations will have a degree of power to set the terms at which they will transact, including the prices they charge and the payment terms acceptable to them. The economy is mostly made up of price makers who must judge what prices their customers will bear and the prices and terms that will be worth supplying them at. Making crucial business decisions to justify the scarce capital and labour and natural resources employed in satisfying their customers.

It therefore would be best to let the many competitors for the household’s spending decision to slug it out without regulatory interference. That is accept that the market economy broadly defined and left alone will work well to satisfy consumers. And that the survival of any business will depend on its ability to compete successfully for scarce capital and labour with which to serve households with the variety of goods and services that are willing to pay for.

Successful businesses have every incentive to increase output and to add to the capital and the labour and natural resources they employ- not to limit them with discouragingly high prices or unattractive terms. While businesses who fail for want of an ability to supply households at a profit should be encouraged to release the resources they are wasting for better use by other firms.

Economic efficiency demands no less. Given this competition by a very large number of firms who supply goods and services for a tiny, but potentially very valuable, share of the household budget. Is there any good reason to worry about what may or could be a temporary and limited degree of monopoly power that might be abused? Worry enough to actively conduct an expensive pro-competition policy to force unknown changes in the evolving structure of an economy? I would suggest not.

An active competition policy can however provide perverse incentives. Competition policy can be utilised to limit competition in the interest of the established firms. The case of Lewis Stores intervening in the proposed amalgamation of the household furniture and appliances divisions of Checkers and Pepkor seems an obvious case of this. On the face of it, any merger that led to fewer competitors, in an artificially and narrowly defined market segment, would be welcomed by the other potential suppliers, from smaller rivals with currently smaller market shares (so defined) hoping to take advantage of any complacency or abuse of market power.

But this presumably is not the Lewis Stores view. I presume they wish to block the merger because they fear the extra competition for the household spend from a now stronger rival. In this dispute the specific market to be affected has been narrowly and arbitrarily defined as the market for household furniture and appliances accompanied with credit provided by the retailer. Yet one where the potential seller also competes with the on-line offers of a Takelot or an Amazon offering goods sourced from all over the world.

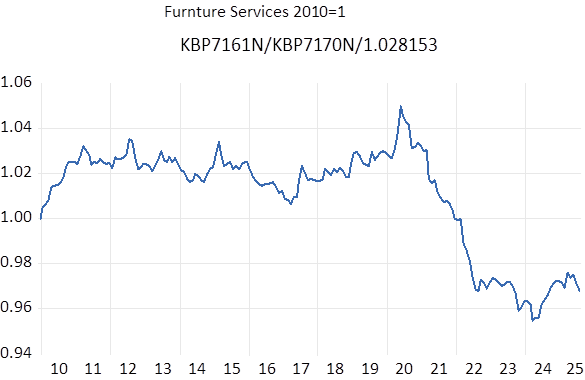

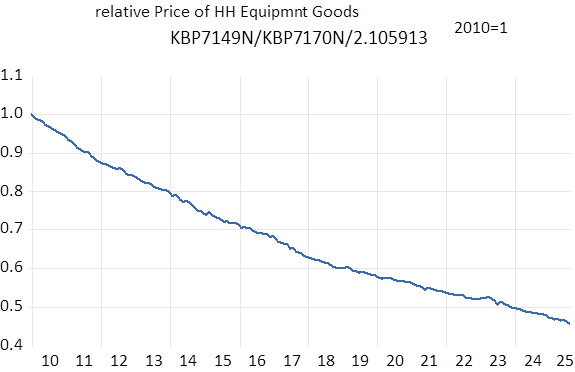

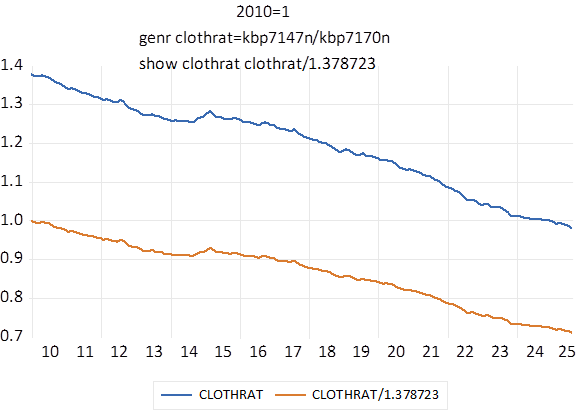

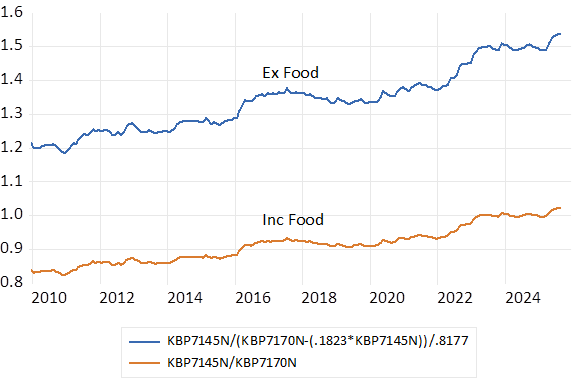

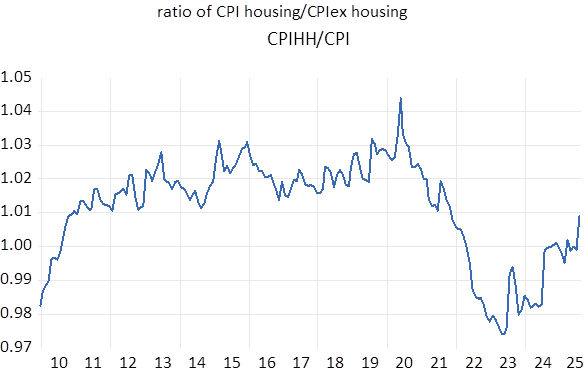

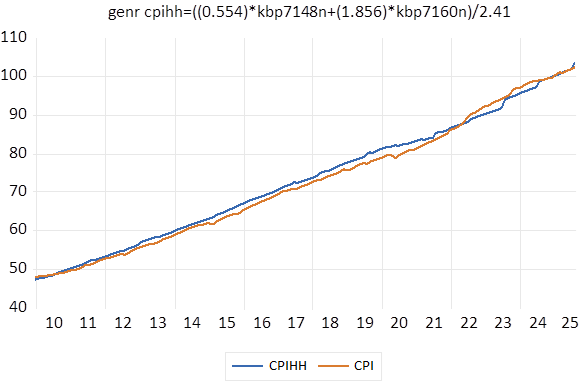

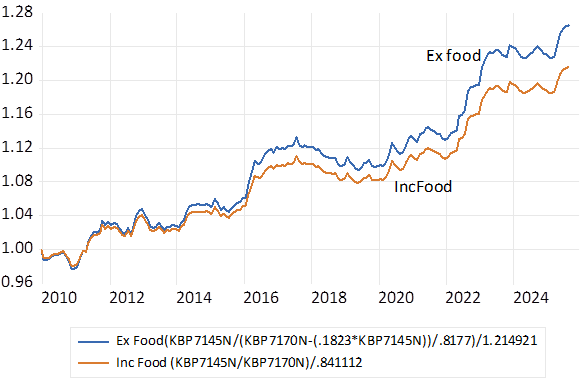

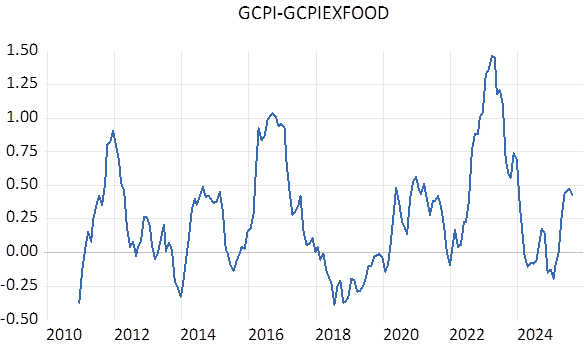

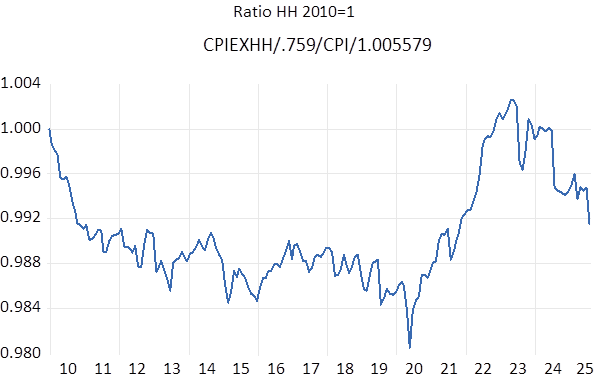

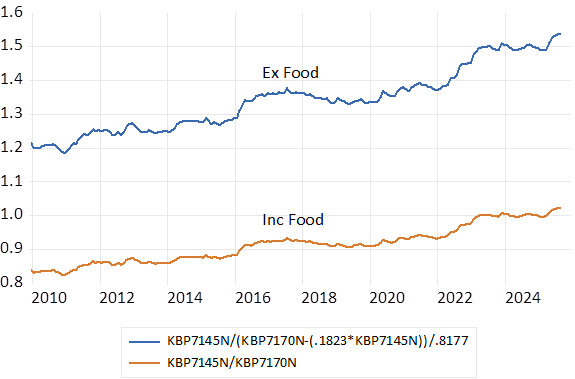

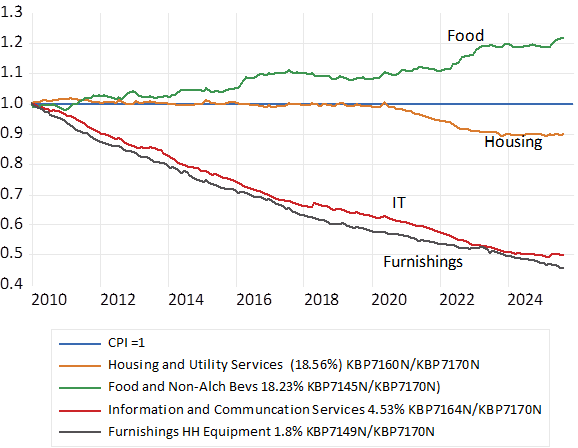

The share of furnishings and household equipment in the CPI- representing the share of the household budget spent on furniture etc in SA, is now of the small order of 1.8%. And the price of furniture has risen by only half the rate of consumer prices in general, in line with cheaper communications. Food and beverage prices with an 18% share have risen by 20% more than the average while housing costs – including the rent attributed to owner occupiers with a weight slightly heavier than food, is now about 10% lower in real terms than it was in 2010. All evidence of a highly dynamic economy with real price competition.

The SA competition authorities, if they approve the Pepkor-Shoprite deal, are very likely to order the new venture not to reduce its workforce. That is not allowed to reduce its costs to become more efficient, more price competitive and hence made less able to compete for a larger share of the household spend. Providing another case of competition policy in SA inhibiting rather than encouraging competition and an efficient economy.

Relative Prices (2010=1) and Share of CPI

Source; SA Reserve Bank and Investec Wealth & Investment.